Você também pode gostar

- Notes On CPWD PDFDocumento70 páginasNotes On CPWD PDFshekarj92% (26)

- A Project Report On Budget and Budgetry ControlDocumento77 páginasA Project Report On Budget and Budgetry ControlNagireddy Kalluri100% (3)

- March 13, 2018 Utility Vs Axon Body-Worn & In-Car Camera PresentationDocumento10 páginasMarch 13, 2018 Utility Vs Axon Body-Worn & In-Car Camera PresentationDillon CollierAinda não há avaliações

- Lisa Rapuano Finding Your Way Along The Many Paths of ValueDocumento29 páginasLisa Rapuano Finding Your Way Along The Many Paths of ValueValueWalk100% (1)

- Hillhouse-Zhang-Value Investing Congress West 2010Documento24 páginasHillhouse-Zhang-Value Investing Congress West 2010jackefellerAinda não há avaliações

- 2009 Annual LetterDocumento5 páginas2009 Annual Letterppate100% (1)

- Bridge With Buffett A Mathematician On Wall StreetDocumento3 páginasBridge With Buffett A Mathematician On Wall StreetgjangAinda não há avaliações

- Eminence CapitalMen's WarehouseDocumento0 páginaEminence CapitalMen's WarehouseCanadianValueAinda não há avaliações

- Investing in Credit Hedge Funds: An In-Depth Guide to Building Your Portfolio and Profiting from the Credit MarketNo EverandInvesting in Credit Hedge Funds: An In-Depth Guide to Building Your Portfolio and Profiting from the Credit MarketAinda não há avaliações

- Distressed Investment Banking - To the Abyss and Back - Second EditionNo EverandDistressed Investment Banking - To the Abyss and Back - Second EditionAinda não há avaliações

- Risk. Reward. Repeat.: How I Succeeded and How You Can TooNo EverandRisk. Reward. Repeat.: How I Succeeded and How You Can TooAinda não há avaliações

- PIPE Investments of Private Equity Funds: The temptation of public equity investments to private equity firmsNo EverandPIPE Investments of Private Equity Funds: The temptation of public equity investments to private equity firmsAinda não há avaliações

- Third Point Q3 2012 Investor Letter TPOIDocumento11 páginasThird Point Q3 2012 Investor Letter TPOIVALUEWALK LLCAinda não há avaliações

- 2012 Third Point Q2 Investor Letter TPOIDocumento7 páginas2012 Third Point Q2 Investor Letter TPOIVALUEWALK LLC100% (1)

- 2012 Third Point Q2 Investor Letter TPOIDocumento7 páginas2012 Third Point Q2 Investor Letter TPOIVALUEWALK LLC100% (1)

- Guidebook On Delegation of AuthorityDocumento32 páginasGuidebook On Delegation of AuthorityMayur JainAinda não há avaliações

- Boyar's Intrinsic Value Research Forgotten FourtyDocumento49 páginasBoyar's Intrinsic Value Research Forgotten FourtyValueWalk100% (1)

- Scott Miller of Greenhaven Road Capital: Long On Zix CorpDocumento0 páginaScott Miller of Greenhaven Road Capital: Long On Zix CorpcurrygoatAinda não há avaliações

- Ubben ValueInvestingCongress 100212Documento27 páginasUbben ValueInvestingCongress 100212VALUEWALK LLC100% (1)

- Clear Thinking About Share RepurchaseDocumento29 páginasClear Thinking About Share RepurchaseVrtpy CiurbanAinda não há avaliações

- H. Kevin Byun's Q4 2013 Denali Investors LetterDocumento4 páginasH. Kevin Byun's Q4 2013 Denali Investors LetterValueInvestingGuy100% (1)

- Murray Stahl - Value - Investor - May - 2013 PDFDocumento10 páginasMurray Stahl - Value - Investor - May - 2013 PDFkdwcapitalAinda não há avaliações

- David Tepper S 2007 Presentation at Carnegie Mellon PDFDocumento7 páginasDavid Tepper S 2007 Presentation at Carnegie Mellon PDFPattyPattersonAinda não há avaliações

- The 400% Man: How A College Dropout at A Tiny Utah Fund Beat Wall Street, and Why Most Managers Are Scared To Copy HimDocumento5 páginasThe 400% Man: How A College Dropout at A Tiny Utah Fund Beat Wall Street, and Why Most Managers Are Scared To Copy Himrakeshmoney99Ainda não há avaliações

- Decision-Making For Investors: Theory, Practice, and PitfallsDocumento20 páginasDecision-Making For Investors: Theory, Practice, and PitfallsGaurav JainAinda não há avaliações

- Bob Robotti - Navigating Deep WatersDocumento35 páginasBob Robotti - Navigating Deep WatersCanadianValue100% (1)

- Arlington Value 2016 Annual Letter PDFDocumento6 páginasArlington Value 2016 Annual Letter PDFChrisAinda não há avaliações

- Hayman Bass 20081017Documento3 páginasHayman Bass 20081017dylan555100% (1)

- Allan Mecham Interview PDFDocumento6 páginasAllan Mecham Interview PDFRajeev BahugunaAinda não há avaliações

- Klarman Yield PigDocumento2 páginasKlarman Yield Pigalexg6Ainda não há avaliações

- Aquamarine - 2013Documento84 páginasAquamarine - 2013sb86Ainda não há avaliações

- Amitabh Singhvi L MOI Interview L JUNE-2011Documento6 páginasAmitabh Singhvi L MOI Interview L JUNE-2011Wayne GonsalvesAinda não há avaliações

- Thomas Russo: Global Value Investing - Richard Ivey School of Business, 2013Documento34 páginasThomas Russo: Global Value Investing - Richard Ivey School of Business, 2013Hedge Fund ConversationsAinda não há avaliações

- 8th Annual New York: Value Investing CongressDocumento53 páginas8th Annual New York: Value Investing CongressVALUEWALK LLCAinda não há avaliações

- Brian Spector Leaving Baupost Letter - Business InsiderDocumento4 páginasBrian Spector Leaving Baupost Letter - Business InsiderHedge Fund ConversationsAinda não há avaliações

- Carl Icahn's Letter To Apple's Tim CookDocumento4 páginasCarl Icahn's Letter To Apple's Tim CookCanadianValueAinda não há avaliações

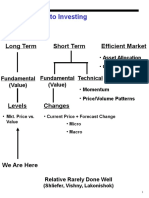

- Approaches To Investing: Long Term Short Term Efficient MarketDocumento71 páginasApproaches To Investing: Long Term Short Term Efficient MarketPeter WarmeAinda não há avaliações

- Graham and Doddsville - Issue 9 - Spring 2010Documento33 páginasGraham and Doddsville - Issue 9 - Spring 2010g4nz0Ainda não há avaliações

- Graham - Doddsville - Issue 40 - v19 PDFDocumento61 páginasGraham - Doddsville - Issue 40 - v19 PDFRofiq 4 NugrohoAinda não há avaliações

- Chuck Akre Value Investing Conference Talk - 'An Investor's Odyssey - The Search For Outstanding Investments' PDFDocumento10 páginasChuck Akre Value Investing Conference Talk - 'An Investor's Odyssey - The Search For Outstanding Investments' PDFSunil ParikhAinda não há avaliações

- Value Investing Congress NY 2010 AshtonDocumento26 páginasValue Investing Congress NY 2010 Ashtonbrian4877Ainda não há avaliações

- Buffett On Valuation PDFDocumento7 páginasBuffett On Valuation PDFvinaymathew100% (1)

- Value Investors Club - AMAZONDocumento11 páginasValue Investors Club - AMAZONMichael Lee100% (1)

- Moi201102 Super Investors PRINTDocumento170 páginasMoi201102 Super Investors PRINTbrl_oakcliffAinda não há avaliações

- Graham Doddsville Issue 33 v23Documento46 páginasGraham Doddsville Issue 33 v23marketfolly.comAinda não há avaliações

- Austrian Economics & InvestingDocumento20 páginasAustrian Economics & InvestingRaj KumarAinda não há avaliações

- J.P. Morgan 2023 OutlookDocumento55 páginasJ.P. Morgan 2023 OutlookHerman TanAinda não há avaliações

- SNPK FinancialsDocumento123 páginasSNPK FinancialsJohn Aldridge Chew100% (1)

- Josh Tarasoff AmazonDocumento7 páginasJosh Tarasoff AmazonDaniel HanasabAinda não há avaliações

- Buffett On ValuationDocumento7 páginasBuffett On ValuationAyush AggarwalAinda não há avaliações

- High Conviction Barrons Talks With RiverParkWedgewood Fund Portfolio Manager David RolfeDocumento3 páginasHigh Conviction Barrons Talks With RiverParkWedgewood Fund Portfolio Manager David RolfebernhardfAinda não há avaliações

- Warren Buffett and GEICO Case StudyDocumento18 páginasWarren Buffett and GEICO Case StudyReymond Jude PagcoAinda não há avaliações

- 10 Years PAt Dorsy PDFDocumento32 páginas10 Years PAt Dorsy PDFGurjeevAinda não há avaliações

- Aquamarine Fund PresentationDocumento25 páginasAquamarine Fund PresentationVijay MalikAinda não há avaliações

- VII332Documento21 páginasVII332currygoatAinda não há avaliações

- Owl Creek Q2 2010 LetterDocumento9 páginasOwl Creek Q2 2010 Letterjackefeller100% (1)

- Mick McGuire Value Investing Congress Presentation Marcato Capital ManagementDocumento70 páginasMick McGuire Value Investing Congress Presentation Marcato Capital Managementmarketfolly.comAinda não há avaliações

- Anon - Housing Thesis 09 12 2011Documento22 páginasAnon - Housing Thesis 09 12 2011cnm3dAinda não há avaliações

- Scion 2006 4q Rmbs Cds Primer and FaqDocumento8 páginasScion 2006 4q Rmbs Cds Primer and FaqsabishiiAinda não há avaliações

- Morgan Stanley - ROICDocumento44 páginasMorgan Stanley - ROICGaurav AhirkarAinda não há avaliações

- Hayman CapitalDocumento26 páginasHayman CapitalZerohedge97% (33)

- The Art of Vulture Investing: Adventures in Distressed Securities ManagementNo EverandThe Art of Vulture Investing: Adventures in Distressed Securities ManagementAinda não há avaliações

- Financial Fine Print: Uncovering a Company's True ValueNo EverandFinancial Fine Print: Uncovering a Company's True ValueNota: 3 de 5 estrelas3/5 (3)

- MicroCap Superstars: The Movers and Shakers in Small Stocks, and Big MoneyNo EverandMicroCap Superstars: The Movers and Shakers in Small Stocks, and Big MoneyNota: 4 de 5 estrelas4/5 (2)

- Peter L. Bernstein Classics Collection: Capital Ideas, Against the Gods, The Power of Gold and Capital Ideas EvolvingNo EverandPeter L. Bernstein Classics Collection: Capital Ideas, Against the Gods, The Power of Gold and Capital Ideas EvolvingAinda não há avaliações

- 8th Annual New York: Value Investing CongressDocumento53 páginas8th Annual New York: Value Investing CongressVALUEWALK LLCAinda não há avaliações

- SHLDDocumento18 páginasSHLDduwe7809100% (1)

- 8th Annual New York: Value Investing CongressDocumento46 páginas8th Annual New York: Value Investing CongressVALUEWALK LLCAinda não há avaliações

- 8th Annual New York: Value Investing CongressDocumento51 páginas8th Annual New York: Value Investing CongressVALUEWALK LLCAinda não há avaliações

- Rockstone Research URS1 EnglishDocumento32 páginasRockstone Research URS1 EnglishVALUEWALK LLC100% (1)

- Green Mountain Coffee Roasters' Q2 and Q3 2011 Net Sales Figures Look Odd and Why It MattersDocumento8 páginasGreen Mountain Coffee Roasters' Q2 and Q3 2011 Net Sales Figures Look Odd and Why It MattersmistervigilanteAinda não há avaliações

- Value Investing Congress Presentation-Tilson-10!1!12Documento93 páginasValue Investing Congress Presentation-Tilson-10!1!12VALUEWALK LLCAinda não há avaliações

- Greenlight Q2 Letter To InvestorsDocumento5 páginasGreenlight Q2 Letter To InvestorsVALUEWALK LLCAinda não há avaliações

- VALUExVail 2012 James ChanosDocumento30 páginasVALUExVail 2012 James ChanosVALUEWALK LLCAinda não há avaliações

- T2 Accredited Fund Letter To Investors June 12Documento10 páginasT2 Accredited Fund Letter To Investors June 12VALUEWALK LLCAinda não há avaliações

- HP PresentationDocumento69 páginasHP Presentationssc320Ainda não há avaliações

- Fairholme: Ignore The CrowdDocumento13 páginasFairholme: Ignore The CrowdVALUEWALK LLCAinda não há avaliações

- Fairholme: Ignore The CrowdDocumento13 páginasFairholme: Ignore The CrowdVALUEWALK LLCAinda não há avaliações

- Pershing Square Q1 12 Investor LetterDocumento14 páginasPershing Square Q1 12 Investor LetterVALUEWALK LLCAinda não há avaliações

- Mauboussinonstrategy - Sharerepurchasefromallangles June 2012Documento15 páginasMauboussinonstrategy - Sharerepurchasefromallangles June 2012zeebugAinda não há avaliações

- Annual Report: March 31, 2011Documento23 páginasAnnual Report: March 31, 2011VALUEWALK LLCAinda não há avaliações

- Why We'Re Long J.C. Penney-T2 PartnersDocumento18 páginasWhy We'Re Long J.C. Penney-T2 PartnersVALUEWALK LLCAinda não há avaliações

- GMO 7 Year Asset Forecast - Jan 2014Documento1 páginaGMO 7 Year Asset Forecast - Jan 2014CanadianValueAinda não há avaliações

- Bruce Berkowitz - Fairholme 2011 Stat Sheet (Morning Star)Documento2 páginasBruce Berkowitz - Fairholme 2011 Stat Sheet (Morning Star)Luochang YuAinda não há avaliações

- To Longleaf Shareholders: Cumulative Returns at December 31, 2011Documento6 páginasTo Longleaf Shareholders: Cumulative Returns at December 31, 2011VALUEWALK LLCAinda não há avaliações

- Nokia Results2011Q4eDocumento60 páginasNokia Results2011Q4ejunaid112Ainda não há avaliações

- ASFL - Quarterly Accounts - September 30, 2011Documento17 páginasASFL - Quarterly Accounts - September 30, 2011VALUEWALK LLCAinda não há avaliações

- The New Accounting ModelDocumento38 páginasThe New Accounting Modeldiqyst33251Ainda não há avaliações

- Project in Business FinanceDocumento10 páginasProject in Business FinanceKOUJI N. MARQUEZAinda não há avaliações

- Retail Management Mini ProjectDocumento9 páginasRetail Management Mini ProjectNagarjuna ReddyAinda não há avaliações

- May 2017 Advanced Financial Accounting & Reporting Final Pre-BoardDocumento20 páginasMay 2017 Advanced Financial Accounting & Reporting Final Pre-BoardPatrick ArazoAinda não há avaliações

- How To Budget Your Money - The 50-20-30 GuidelineDocumento7 páginasHow To Budget Your Money - The 50-20-30 GuidelineAndrew Peter100% (1)

- FTG Irs Form 990-Ez 2008Documento12 páginasFTG Irs Form 990-Ez 2008L. A. PatersonAinda não há avaliações

- This Document Contains Confidential Company Information. Do Not Disclose It To Third Parties Without Permission From The CompanyDocumento11 páginasThis Document Contains Confidential Company Information. Do Not Disclose It To Third Parties Without Permission From The CompanyGowtham SunderajanAinda não há avaliações

- Capital Structure - RanbaxyDocumento40 páginasCapital Structure - RanbaxyNooral Alfa100% (1)

- Assessment of Government Budgetary Control Procedures and Utilization (In Case of Hawassa University)Documento22 páginasAssessment of Government Budgetary Control Procedures and Utilization (In Case of Hawassa University)samuel debebe100% (1)

- DHHL Acquisition of Mō Ili Ili PropertiesDocumento6 páginasDHHL Acquisition of Mō Ili Ili PropertiesHPR NewsAinda não há avaliações

- ACT23 - 12 - Standard Costs and Variance AnalysisDocumento4 páginasACT23 - 12 - Standard Costs and Variance AnalysisLim JugyeongAinda não há avaliações

- Principles of MicroeconomicDocumento9 páginasPrinciples of MicroeconomicMohd Fadzly100% (1)

- TRN FI001 Finance Overview v1 3Documento96 páginasTRN FI001 Finance Overview v1 3Shyam JaganathAinda não há avaliações

- Hangar PlanningDocumento39 páginasHangar Planningmonocrome fajar tjahyonoAinda não há avaliações

- Budgetary ControlDocumento11 páginasBudgetary ControlDurga Prasad NallaAinda não há avaliações

- Belgica v. Ochoa DigestDocumento7 páginasBelgica v. Ochoa DigestClara Mae ReyesAinda não há avaliações

- 2020 CMA Content Specification OutlinesDocumento12 páginas2020 CMA Content Specification OutlinesDivyam SahniAinda não há avaliações

- Case StudyDocumento11 páginasCase Studyapi-269859076Ainda não há avaliações

- Arkansas Bill HB1149Documento7 páginasArkansas Bill HB1149capsearchAinda não há avaliações

- Chapter 1 SolutionsDocumento5 páginasChapter 1 SolutionsChan ZacharyAinda não há avaliações

- St. Louis, Missouri Comprehensive Revenue Study 2009, by The PFM GroupDocumento349 páginasSt. Louis, Missouri Comprehensive Revenue Study 2009, by The PFM GroupstlbeaconAinda não há avaliações

- Network Strategic Evaluation: Rodrigo Archondo-Callao Senior Highway Engineer, ETWTRDocumento24 páginasNetwork Strategic Evaluation: Rodrigo Archondo-Callao Senior Highway Engineer, ETWTRJared MakoriAinda não há avaliações

- Raghuram Rajan On World EconomyDocumento2 páginasRaghuram Rajan On World EconomyAbhinav RajAinda não há avaliações

- Work Sheet # 2Documento4 páginasWork Sheet # 2Sashina GrantAinda não há avaliações

- Unicef SlideshowDocumento13 páginasUnicef SlideshowDhrubajyoti MaitraAinda não há avaliações

- Economics & Management DecisionsDocumento29 páginasEconomics & Management DecisionsRaj KumarAinda não há avaliações