Você também pode gostar

- Customer Satisfaction Survey - Internet Banking "Bank of Baroda" by - Amit DubeyDocumento56 páginasCustomer Satisfaction Survey - Internet Banking "Bank of Baroda" by - Amit Dubeyamit_ims351480% (20)

- Technologies in Banking SectorDocumento43 páginasTechnologies in Banking SectorDhaval Majithia100% (3)

- A Study of Customer Perception Towards E-Banking Services Offered in Banking Sector (Accf)Documento56 páginasA Study of Customer Perception Towards E-Banking Services Offered in Banking Sector (Accf)Saurabh Chawla100% (1)

- E Banking ReportDocumento40 páginasE Banking ReportVansh Patel100% (2)

- Online Banking Services Icici BankDocumento10 páginasOnline Banking Services Icici BankMohmmedKhayyumAinda não há avaliações

- Consumer Behaviour Towards E Banking Final ReportDocumento67 páginasConsumer Behaviour Towards E Banking Final ReportTaha Merchant100% (1)

- A Study On Customer Awareness On E-Banking Services at Union Bank of India, MangaloreDocumento74 páginasA Study On Customer Awareness On E-Banking Services at Union Bank of India, MangaloreThasleem Athar95% (40)

- Customer Satisfaction in The Indian Banking SectorDocumento70 páginasCustomer Satisfaction in The Indian Banking SectorAbhishek Singh82% (22)

- Project Report On e BankingDocumento89 páginasProject Report On e BankingSourabh Kumar Das100% (1)

- Financial Services Industry FutureDocumento3 páginasFinancial Services Industry FutureVickySalve0% (1)

- "Satisfaction From E-Banking Services. A Comparative Study of HDFC and ICICI Bank.Documento131 páginas"Satisfaction From E-Banking Services. A Comparative Study of HDFC and ICICI Bank.bairasiarachana84% (37)

- A Study On The Customer Response Towards Mobile BankingDocumento63 páginasA Study On The Customer Response Towards Mobile Bankinganuragmsrcasc57% (7)

- SBI Mobile BankingDocumento46 páginasSBI Mobile BankingAbhishek Tiwari100% (3)

- Online BankingDocumento31 páginasOnline BankingRavi Kashyap506Ainda não há avaliações

- Project On Banking Sector in IndiaDocumento45 páginasProject On Banking Sector in IndiaPunit Rao77% (13)

- A Study On Customer Satisfaction Towards The Net Banking Services of HDFC Bank in Lucknow CityDocumento7 páginasA Study On Customer Satisfaction Towards The Net Banking Services of HDFC Bank in Lucknow CityChandan Srivastava0% (1)

- Project Report On e BankingDocumento88 páginasProject Report On e BankingDhirender Chauhan80% (10)

- Consumer Satisfaction Union BankDocumento23 páginasConsumer Satisfaction Union BankShyam Rout100% (2)

- E-Banking in India: Sandeep ParmarDocumento44 páginasE-Banking in India: Sandeep ParmarVikas SoodAinda não há avaliações

- Consumer Perception of E-banking ServicesDocumento46 páginasConsumer Perception of E-banking ServicesWwe MomentsAinda não há avaliações

- Introduction of E CommerceDocumento2 páginasIntroduction of E CommerceAkanksha KadamAinda não há avaliações

- Project Report On Online BankingDocumento24 páginasProject Report On Online BankingDrSanjeev K Chaudhary100% (3)

- RoleOf It Technology in Banking SectorDocumento69 páginasRoleOf It Technology in Banking SectorPranav Datta100% (1)

- The Impact of Electornic Banking On Service Delivery To Customers of Ghana Commercial Bank LTDDocumento67 páginasThe Impact of Electornic Banking On Service Delivery To Customers of Ghana Commercial Bank LTDmgbemena chika tenyson100% (2)

- A Study of Customer Perception Towards E-Banking Services Offered in Banking Sector (It)Documento73 páginasA Study of Customer Perception Towards E-Banking Services Offered in Banking Sector (It)Kaustubh AgrawalAinda não há avaliações

- Customer Awareness and Preference Towards E-Banking Services of Banks (A Study of SBI)Documento10 páginasCustomer Awareness and Preference Towards E-Banking Services of Banks (A Study of SBI)aurorashiva1Ainda não há avaliações

- E BankingDocumento74 páginasE BankingKritika Shiva100% (1)

- Project Report On Mobile BankingDocumento45 páginasProject Report On Mobile BankingTulika Agrawal Rawool57% (7)

- Mobile Banking Project 2010-2011Documento74 páginasMobile Banking Project 2010-2011Nitesh Salunke67% (3)

- A Study of Customer Perception Towards E-Banking Services Offered in Banking Sector - Doc11111111111Documento73 páginasA Study of Customer Perception Towards E-Banking Services Offered in Banking Sector - Doc11111111111Sami Zama0% (1)

- Online BankingDocumento30 páginasOnline BankingNikunjBhuwalka67% (3)

- Objective of The StudyDocumento13 páginasObjective of The StudyYogendra Kumar Jain100% (1)

- Jishnu - Effectiveness of Yono App of SbiDocumento69 páginasJishnu - Effectiveness of Yono App of Sbinoufeer p nazar p.n0% (1)

- QUESTIONAIREDocumento3 páginasQUESTIONAIREsunny12101986Ainda não há avaliações

- Summer Internship SbiDocumento64 páginasSummer Internship SbiPriya GuptaAinda não há avaliações

- A Study of Netbanking Provided by HDFC BankDocumento73 páginasA Study of Netbanking Provided by HDFC Banknk_khanna89% (36)

- Project of Internet Banking of SbiDocumento41 páginasProject of Internet Banking of Sbiprakash100% (1)

- SBI Internet BankingDocumento21 páginasSBI Internet BankingHiteshwar Singh Andotra60% (5)

- A Comparative Study of E-Banking in Public andDocumento10 páginasA Comparative Study of E-Banking in Public andanisha mathuriaAinda não há avaliações

- Internet Banking of SbiDocumento73 páginasInternet Banking of Sbijiya_ahuja57883% (12)

- Literature ReviewDocumento4 páginasLiterature Reviewdivya100% (1)

- Sip Report HDFC Bank (Digitization)Documento65 páginasSip Report HDFC Bank (Digitization)Ashish Chandra100% (1)

- Karan Khanna - B.com Hons - Online BankingDocumento81 páginasKaran Khanna - B.com Hons - Online BankingMd SaquibAinda não há avaliações

- Innovation in Banking SectorDocumento66 páginasInnovation in Banking Sectorpappu_jaiswal43767% (3)

- Customer Satisfaction With Ebanking in Uco BankDocumento77 páginasCustomer Satisfaction With Ebanking in Uco BankRamanand100% (3)

- Online Banking Services Icici BankDocumento51 páginasOnline Banking Services Icici BankMubeenAinda não há avaliações

- A Study On Consumer Perception Towards Mobile Banking Services of State Bank of IndiaDocumento45 páginasA Study On Consumer Perception Towards Mobile Banking Services of State Bank of IndiaVijaya Anandhan100% (1)

- Internet Banking and Mobile Banking - Safe and Secure BankingDocumento99 páginasInternet Banking and Mobile Banking - Safe and Secure BankingRehanCoolestBoy0% (1)

- Identifying Prospective SME Customers for CRMDocumento93 páginasIdentifying Prospective SME Customers for CRMDilip BalachandranAinda não há avaliações

- E-Banking Study on Syndicate BankDocumento80 páginasE-Banking Study on Syndicate BankMaa Maa100% (1)

- Digital Banking – The New Way to BankDocumento50 páginasDigital Banking – The New Way to BankAYUSHI GABAAinda não há avaliações

- Retail Banking With Yes BankDocumento67 páginasRetail Banking With Yes BankJuyee JainAinda não há avaliações

- Impact of Digitalization For Customers of HDFC Bank: Post Graduate Diploma in ManagementDocumento42 páginasImpact of Digitalization For Customers of HDFC Bank: Post Graduate Diploma in ManagementJASMEET SINGHAinda não há avaliações

- E-Banking MBA Marketing VTU Project - 167969731Documento99 páginasE-Banking MBA Marketing VTU Project - 167969731Deepak SinghalAinda não há avaliações

- DIGITALIZATION IN BANK HDFC BANk Final AditiDocumento90 páginasDIGITALIZATION IN BANK HDFC BANk Final AditiMaster PrintersAinda não há avaliações

- Customer Satisfaction Survey Internet Banking Bank of Baroda by Amit DubeyDocumento56 páginasCustomer Satisfaction Survey Internet Banking Bank of Baroda by Amit DubeyNeha jainAinda não há avaliações

- Risks and Security of Digital BankingDocumento12 páginasRisks and Security of Digital BankingAniruddha BorkarAinda não há avaliações

- Declaration: "Customer Satisfaction On Internet Banking Service Quality"Documento37 páginasDeclaration: "Customer Satisfaction On Internet Banking Service Quality"Alok NayakAinda não há avaliações

- Department of Management Studies: (Jai Narain Vyas University, Jodhpur)Documento50 páginasDepartment of Management Studies: (Jai Narain Vyas University, Jodhpur)Utkarsh PatelAinda não há avaliações

- Internet Banking: Submitted By: Under The Guidance Of: Industry Guide Faculty GuideDocumento23 páginasInternet Banking: Submitted By: Under The Guidance Of: Industry Guide Faculty Guideਅਮਨਦੀਪ ਸਿੰਘ ਰੋਗਲਾAinda não há avaliações

- Pizza Joint Service FinalDocumento28 páginasPizza Joint Service Finalmajiclover50% (2)

- Mutual Fund Promotion in NCRDocumento58 páginasMutual Fund Promotion in NCRmajiclover100% (3)

- Internal Marketing in Foreign Bank G-2Documento29 páginasInternal Marketing in Foreign Bank G-2majiclover100% (2)

- Consumer Preferences For Coca ColaDocumento45 páginasConsumer Preferences For Coca Colamajiclover90% (20)

- Final Mis Report - AccDocumento34 páginasFinal Mis Report - Accmajiclover85% (13)

- Launchof New Product (Shoes)Documento50 páginasLaunchof New Product (Shoes)majiclover75% (16)

- To Launch Bata BiscutDocumento33 páginasTo Launch Bata BiscutmajicloverAinda não há avaliações

- Advertising ResearchDocumento29 páginasAdvertising ResearchmajicloverAinda não há avaliações

- BBuzzDocumento14 páginasBBuzzmajiclover100% (2)

- A Project ReportDocumento58 páginasA Project Reportmajiclover100% (9)

- A Project Report of MisDocumento25 páginasA Project Report of Mismajiclover75% (16)

- Brand Positioning of Slice in SaharanpurDocumento103 páginasBrand Positioning of Slice in SaharanpurmajicloverAinda não há avaliações

- Post Graduate Diploma in Business Management: On The Partial Fulfillment of 3 Tri-Semester ofDocumento42 páginasPost Graduate Diploma in Business Management: On The Partial Fulfillment of 3 Tri-Semester ofmajiclover75% (12)

- 2019 - 2020 Vinhomes - Corporate - PresentationDocumento40 páginas2019 - 2020 Vinhomes - Corporate - PresentationHIeu DoAinda não há avaliações

- ListDocumento6 páginasListRoshelleAinda não há avaliações

- How financial promotions influence young people's decisionsDocumento16 páginasHow financial promotions influence young people's decisionsbudhaditya.choudhury2583Ainda não há avaliações

- Constitution of Mutungo Community AssociationDocumento9 páginasConstitution of Mutungo Community AssociationRobert Baguma MwesigwaAinda não há avaliações

- Office of The Auditor Construction Industry Authority of The PhilippinesDocumento3 páginasOffice of The Auditor Construction Industry Authority of The PhilippinesHoven MacasinagAinda não há avaliações

- HSBC Feb STTMNTDocumento2 páginasHSBC Feb STTMNTShelvya ReeseAinda não há avaliações

- Insurance Recit Questions (Atty. Bathan)Documento6 páginasInsurance Recit Questions (Atty. Bathan)Aaron ViloriaAinda não há avaliações

- A Brief History of Money PDFDocumento52 páginasA Brief History of Money PDFCristian CambiazoAinda não há avaliações

- Annex A-RMC 26-2018Documento2 páginasAnnex A-RMC 26-2018Anonymous LC5kFdtc100% (1)

- Sol. Man. - Chapter 3 - Bank Reconciliation - Ia PartDocumento15 páginasSol. Man. - Chapter 3 - Bank Reconciliation - Ia PartMike Joseph E. Moran100% (3)

- Gramin BankDocumento8 páginasGramin BankSayan SahaAinda não há avaliações

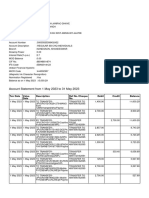

- Account Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento10 páginasAccount Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceavinashdeshmukh7027Ainda não há avaliações

- Set 5 2.3 American Home V TantucoDocumento2 páginasSet 5 2.3 American Home V TantucoJose MasarateAinda não há avaliações

- Chapter 3Documento3 páginasChapter 3Lukman Kresno OktaviantoAinda não há avaliações

- Reading Comprehension ExerciseDocumento23 páginasReading Comprehension Exercisestephen vaiAinda não há avaliações

- Travel and Expense PolicyDocumento6 páginasTravel and Expense PolicyLee Cogburn100% (1)

- Cases on Persons and Family RelationsDocumento9 páginasCases on Persons and Family RelationsJoseph SereñoAinda não há avaliações

- Toll Free Numbers (India) - Customer Care Service ListDocumento13 páginasToll Free Numbers (India) - Customer Care Service Listvkrm140% (1)

- The Role of The Custodian BankDocumento10 páginasThe Role of The Custodian BankMarius AngaraAinda não há avaliações

- A Research Study of Plastic Money Among HousewivesDocumento34 páginasA Research Study of Plastic Money Among HousewivesNainaAinda não há avaliações

- Credit Midterm Reviewer - Loan and DepositDocumento12 páginasCredit Midterm Reviewer - Loan and Depositviva_33Ainda não há avaliações

- Financial Times Europe - 28 03 2020 - 29 03 2020 PDFDocumento52 páginasFinancial Times Europe - 28 03 2020 - 29 03 2020 PDFNikhil NainAinda não há avaliações

- Us 7 MDocumento291 páginasUs 7 MPrasad NayakAinda não há avaliações

- NIBC 2019 2020 Competition Overview2Documento31 páginasNIBC 2019 2020 Competition Overview2HarshAinda não há avaliações

- BDO Equity FundDocumento4 páginasBDO Equity FundKurt YuAinda não há avaliações

- Chapter 4 Accounts ReceivableDocumento12 páginasChapter 4 Accounts Receivableweddiemae villariza50% (2)

- IIFL - Rollover Action - Feb-21 T Expiry DayDocumento6 páginasIIFL - Rollover Action - Feb-21 T Expiry DayRomelu MartialAinda não há avaliações

- Apply for UNILAG Transcripts and RecordsDocumento7 páginasApply for UNILAG Transcripts and RecordsUdoh Mopolo-Ultra Emmanuel100% (1)

- Khannan Finance & InvestmentDocumento4 páginasKhannan Finance & InvestmentJordan JohnsonAinda não há avaliações

- MGMT E-2030 - Syllabus - Fall 2014 - 8 - 1 - 14Documento20 páginasMGMT E-2030 - Syllabus - Fall 2014 - 8 - 1 - 14smey0% (1)