Você também pode gostar

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Feedback Industry Report BicycleDocumento24 páginasFeedback Industry Report BicycleajaxorAinda não há avaliações

- North South University: Final AssignmentDocumento5 páginasNorth South University: Final AssignmentZahid Hridoy100% (1)

- 213010000086page1 PDFDocumento11 páginas213010000086page1 PDFMBM CONSTRUCTIONAinda não há avaliações

- Canadian Importers Lists - Coconut Briquette, CharcoalDocumento6 páginasCanadian Importers Lists - Coconut Briquette, CharcoalIndo Coconut PremiumAinda não há avaliações

- CRM Subway Updated. (2906) .Docx 2Documento13 páginasCRM Subway Updated. (2906) .Docx 2Razi Ul HassanAinda não há avaliações

- Pepsi Vs Coca ColaDocumento24 páginasPepsi Vs Coca ColaWaseem WaqarAinda não há avaliações

- Comparative Analysis Between Tesco and Sainsbury'sDocumento53 páginasComparative Analysis Between Tesco and Sainsbury'sJahid Hasan100% (4)

- Automatic Car Wash 01Documento46 páginasAutomatic Car Wash 01david33% (3)

- SiaHuatCatalogue2017 2018Documento350 páginasSiaHuatCatalogue2017 2018Chin TecsonAinda não há avaliações

- Cadbury ResearchDocumento34 páginasCadbury Researchchinmay parsekarAinda não há avaliações

- Extra Grammar Practice: Reinforcement: Unit 10Documento1 páginaExtra Grammar Practice: Reinforcement: Unit 10toybox 22Ainda não há avaliações

- Individual Written AssignmentDocumento26 páginasIndividual Written Assignmentovina peirisAinda não há avaliações

- Vishal Completes Asset Sale To TPG, Shriram Group - Business LineDocumento1 páginaVishal Completes Asset Sale To TPG, Shriram Group - Business LineDebolin DeyAinda não há avaliações

- StrategicManagementReport PRAVEENDocumento14 páginasStrategicManagementReport PRAVEENPraveen Nair75% (4)

- Food Bazaar - Wholesale Prices: Mega MartDocumento8 páginasFood Bazaar - Wholesale Prices: Mega MartDiwakar SinghAinda não há avaliações

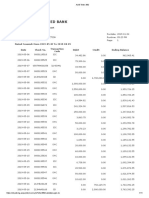

- Account Statement SBI PDFDocumento12 páginasAccount Statement SBI PDFUMESH KUMAR YadavAinda não há avaliações

- A Market Analysis of BritanniaDocumento10 páginasA Market Analysis of Britanniaurmi_patel22Ainda não há avaliações

- PawnshopDocumento25 páginasPawnshopapi-289042707Ainda não há avaliações

- Jameis Winston: Investigation Report and Civil Citation in Crab Leg IncidentDocumento34 páginasJameis Winston: Investigation Report and Civil Citation in Crab Leg IncidentbmortonAinda não há avaliações

- Short Case Layout of Delhaize de Leeuw Supermarket in Ouderghem, BelgiumDocumento2 páginasShort Case Layout of Delhaize de Leeuw Supermarket in Ouderghem, BelgiumSidSinghAinda não há avaliações

- Brochure FT TBR Final 2018Documento13 páginasBrochure FT TBR Final 2018Cico LisadonAinda não há avaliações

- Study The Bar-Chart and Pie-Chart Carefully To Answer The Given QuestionsDocumento28 páginasStudy The Bar-Chart and Pie-Chart Carefully To Answer The Given QuestionsJyoti SukhijaAinda não há avaliações

- Upaya Peningkatkan Melalui Aktivitas: Brand Awareness PT. Go-Jek Indonesia Marketing Public RelationsDocumento13 páginasUpaya Peningkatkan Melalui Aktivitas: Brand Awareness PT. Go-Jek Indonesia Marketing Public RelationsGalih PrimandaAinda não há avaliações

- Value of InformationDocumento19 páginasValue of Informationmishratrilok100% (2)

- StrategyDocumento16 páginasStrategyBeatriz Lança Polidoro100% (1)

- MPM PDF deDocumento16 páginasMPM PDF decyberabad0% (1)

- Market MayhemCase StudyDocumento5 páginasMarket MayhemCase StudyLakshit Garg75% (4)

- Review of Related LiteratureDocumento3 páginasReview of Related LiteratureAya Leah0% (1)

- Travoy Plan BookDocumento29 páginasTravoy Plan Bookadam_8_butlerAinda não há avaliações

- Regulated MarketDocumento12 páginasRegulated Market9406501115100% (2)