Você também pode gostar

- Lecture 5 and 6 - Marginal Absorption CostingDocumento23 páginasLecture 5 and 6 - Marginal Absorption CostingPei IngAinda não há avaliações

- Its Fair Value Less Costs To Sell (If Determinable) Its Value in Use (If Determinable) andDocumento2 páginasIts Fair Value Less Costs To Sell (If Determinable) Its Value in Use (If Determinable) andcutieaikoAinda não há avaliações

- 326 Chapter 9 - Fundamentals of Capital BudgetingDocumento20 páginas326 Chapter 9 - Fundamentals of Capital BudgetingAbira Bilal HanifAinda não há avaliações

- Suggested SolutionsDocumento1 páginaSuggested SolutionscutieaikoAinda não há avaliações

- Chapter 26Documento7 páginasChapter 26JaMa Azolman DualAinda não há avaliações

- Interim ReportingDocumento15 páginasInterim ReportingRica RegorisAinda não há avaliações

- Chapter 07 - ManAcc CabreraDocumento7 páginasChapter 07 - ManAcc CabreraNoruie MagabilinAinda não há avaliações

- Final Solution Winter 2017Documento27 páginasFinal Solution Winter 2017sunkenAinda não há avaliações

- Acc For Busi AssignmentDocumento12 páginasAcc For Busi Assignmentpramodh kumarAinda não há avaliações

- Theory of Production and Cost PDFDocumento24 páginasTheory of Production and Cost PDFSaurav Goyal100% (3)

- Cash Flow Estimation and Risk AnalysisDocumento63 páginasCash Flow Estimation and Risk AnalysisAli JumaniAinda não há avaliações

- Variable & Absorption CostingDocumento23 páginasVariable & Absorption CostingRobin DasAinda não há avaliações

- Total Depreciation : (At Any Time During The Year)Documento10 páginasTotal Depreciation : (At Any Time During The Year)prasad_kcpAinda não há avaliações

- CHAPTER-9 Advance Accounting SolmanDocumento26 páginasCHAPTER-9 Advance Accounting SolmanShiela Gumamela100% (1)

- CHAPTER 9 Guerrero Installment SalesDocumento22 páginasCHAPTER 9 Guerrero Installment SalesMacoy Liceralde50% (6)

- Advanced Accounting Chapter 9Documento22 páginasAdvanced Accounting Chapter 9Ya LunAinda não há avaliações

- Multiple Choice Answers and Solutions: Realized Gross Profit, 2008 P 675,000Documento26 páginasMultiple Choice Answers and Solutions: Realized Gross Profit, 2008 P 675,000Kristine Astorga-NgAinda não há avaliações

- 7 Cost of ProductionDocumento29 páginas7 Cost of ProductionEsha ChaudharyAinda não há avaliações

- Chapter 9Documento18 páginasChapter 9Kate RamirezAinda não há avaliações

- Low Cost and Experience CurvesDocumento31 páginasLow Cost and Experience CurvesJuhi ShahAinda não há avaliações

- Management Accounting: Page 1 of 6Documento70 páginasManagement Accounting: Page 1 of 6Ahmed Raza MirAinda não há avaliações

- Chapter 9Documento22 páginasChapter 9Glynes NaboaAinda não há avaliações

- Take Home Quiz 2Documento2 páginasTake Home Quiz 2Ann SCAinda não há avaliações

- Module 5 The Theory of Cost and ProfitDocumento22 páginasModule 5 The Theory of Cost and ProfitCharice Anne VillamarinAinda não há avaliações

- Capital Budgeting ProblemsDocumento9 páginasCapital Budgeting ProblemsSugandhaShaikh0% (1)

- The Costs of ProductionDocumento20 páginasThe Costs of ProductionMurtaza Ali ShahAinda não há avaliações

- Assignment 3 ACT502Documento6 páginasAssignment 3 ACT502Mahdi KhanAinda não há avaliações

- Property, Plant and Equipment Problems 5-1 (Uy Company)Documento14 páginasProperty, Plant and Equipment Problems 5-1 (Uy Company)NaSheeng100% (1)

- Home Assignment 02: Total Sales Value Variable Costs Fixed Costs Annual Savings 1175000 1175000 1175000 1175000 1175000Documento2 páginasHome Assignment 02: Total Sales Value Variable Costs Fixed Costs Annual Savings 1175000 1175000 1175000 1175000 1175000Farzan Yahya HabibAinda não há avaliações

- Chapter 10Documento9 páginasChapter 10teresaypilAinda não há avaliações

- Interim Financial Reporting: Problem 45-1: True or FalseDocumento7 páginasInterim Financial Reporting: Problem 45-1: True or FalseXyverbel Ocampo RegAinda não há avaliações

- Interim Financial Reporting: Problem 45-1: True or FalseDocumento7 páginasInterim Financial Reporting: Problem 45-1: True or FalseMarjorieAinda não há avaliações

- Interim Financial ReportingDocumento7 páginasInterim Financial ReportingRey Joyce AbuelAinda não há avaliações

- Solving ProblemsDocumento1 páginaSolving Problemstryingacc2Ainda não há avaliações

- Answers For EXERCISES On TOPIC 6Documento9 páginasAnswers For EXERCISES On TOPIC 6Alia HazwaniAinda não há avaliações

- Brealey 5CE Ch09 SolutionsDocumento27 páginasBrealey 5CE Ch09 SolutionsToby Tobes TobezAinda não há avaliações

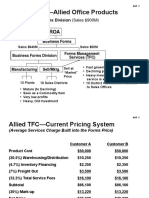

- ABC Costing Allied Office ProductsDocumento13 páginasABC Costing Allied Office ProductsProfessorAsim Kumar Mishra100% (1)

- Delta Project and Repco AnalysisDocumento9 páginasDelta Project and Repco AnalysisvarunjajooAinda não há avaliações

- AnswersDocumento10 páginasAnswersE-Shop TaobaoAinda não há avaliações

- 1.1 Decentralization and Segment ReportingDocumento4 páginas1.1 Decentralization and Segment ReportingJason CabreraAinda não há avaliações

- CHAPTER 11 Answer KeyDocumento8 páginasCHAPTER 11 Answer KeyEnsot Soriano33% (3)

- CPA Review Notes 2019 - BEC (Business Environment Concepts)No EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Nota: 4 de 5 estrelas4/5 (9)

- Agile Procurement: Volume II: Designing and Implementing a Digital TransformationNo EverandAgile Procurement: Volume II: Designing and Implementing a Digital TransformationAinda não há avaliações

- Wiley CMAexcel Learning System Exam Review 2017: Part 1, Financial Reporting, Planning, Performance, and Control (1-year access)No EverandWiley CMAexcel Learning System Exam Review 2017: Part 1, Financial Reporting, Planning, Performance, and Control (1-year access)Ainda não há avaliações

- Business Metrics and Tools; Reference for Professionals and StudentsNo EverandBusiness Metrics and Tools; Reference for Professionals and StudentsAinda não há avaliações

- Entrepreneurial Marketing: Beyond Professionalism to Creativity, Leadership, and SustainabilityNo EverandEntrepreneurial Marketing: Beyond Professionalism to Creativity, Leadership, and SustainabilityAinda não há avaliações

- Automotive Glass Replacement Shop Revenues World Summary: Market Values & Financials by CountryNo EverandAutomotive Glass Replacement Shop Revenues World Summary: Market Values & Financials by CountryAinda não há avaliações

- Business Management for Scientists and Engineers: How I Overcame My Moment of Inertia and Embraced the Dark SideNo EverandBusiness Management for Scientists and Engineers: How I Overcame My Moment of Inertia and Embraced the Dark SideAinda não há avaliações

- Practical M&A Execution and Integration: A Step by Step Guide To Successful Strategy, Risk and Integration ManagementNo EverandPractical M&A Execution and Integration: A Step by Step Guide To Successful Strategy, Risk and Integration ManagementAinda não há avaliações

- Digital Transformation Payday: Navigate the Hype, Lower the Risks, Increase Return on InvestmentsNo EverandDigital Transformation Payday: Navigate the Hype, Lower the Risks, Increase Return on InvestmentsAinda não há avaliações

- Securities Brokerage Revenues World Summary: Market Values & Financials by CountryNo EverandSecurities Brokerage Revenues World Summary: Market Values & Financials by CountryAinda não há avaliações

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryAinda não há avaliações

- Wiley CMAexcel Learning System Exam Review 2017: Part 2, Financial Decision Making (1-year access)No EverandWiley CMAexcel Learning System Exam Review 2017: Part 2, Financial Decision Making (1-year access)Ainda não há avaliações

- HOB SolutionsDocumento5 páginasHOB SolutionscutieaikoAinda não há avaliações

- Suggested Solutions Share Based Payment Compensation 5745 1Documento1 páginaSuggested Solutions Share Based Payment Compensation 5745 1cutieaikoAinda não há avaliações

- Installment SalesDocumento3 páginasInstallment SalesEpal Ako67% (3)

- HobDocumento5 páginasHobcutieaikoAinda não há avaliações

- Tax 2Documento11 páginasTax 2cutieaikoAinda não há avaliações

- HobDocumento5 páginasHobcutieaikoAinda não há avaliações

- HOB SolutionsDocumento5 páginasHOB SolutionscutieaikoAinda não há avaliações

- Not Collectible Within The Normal Operating Cycle Hence Amount To Be Collected Beyond 12 Months Shall Be Classified As A Noncurrent ReceivableDocumento1 páginaNot Collectible Within The Normal Operating Cycle Hence Amount To Be Collected Beyond 12 Months Shall Be Classified As A Noncurrent ReceivablecutieaikoAinda não há avaliações

- Formation & OperationDocumento4 páginasFormation & OperationcutieaikoAinda não há avaliações

- Suggested Solutions Receivable Financing 1. A: "Weighted Average Time To Maturity"Documento2 páginasSuggested Solutions Receivable Financing 1. A: "Weighted Average Time To Maturity"cutieaikoAinda não há avaliações

- SqueezedDocumento1 páginaSqueezedcutieaikoAinda não há avaliações

- Suggested SolutionsDocumento1 páginaSuggested SolutionscutieaikoAinda não há avaliações

- Suggested Solutions 5740 Deferred Income Tax 1Documento1 páginaSuggested Solutions 5740 Deferred Income Tax 1cutieaikoAinda não há avaliações

- AttDocumento8 páginasAttcutieaikoAinda não há avaliações

- Business Combination and Date of AcquisitionDocumento3 páginasBusiness Combination and Date of AcquisitioncutieaikoAinda não há avaliações

- Audit Evidence and Audit ProgramsDocumento9 páginasAudit Evidence and Audit ProgramscutieaikoAinda não há avaliações

- Auditing Theory Quiz Final PrintDocumento6 páginasAuditing Theory Quiz Final Printnda0403Ainda não há avaliações

- Avocado Production in The PhilippinesDocumento20 páginasAvocado Production in The Philippinescutieaiko100% (1)

- 2005 - ACCTG 14-02 - Auditing ProblemsDocumento5 páginas2005 - ACCTG 14-02 - Auditing ProblemscutieaikoAinda não há avaliações