Você também pode gostar

- Summary of IAS 7: Key Principles for Preparing the Statement of Cash FlowsDocumento3 páginasSummary of IAS 7: Key Principles for Preparing the Statement of Cash FlowsHsn IgcseAinda não há avaliações

- IAS 2 SummaryDocumento3 páginasIAS 2 SummaryusmanameerAinda não há avaliações

- Acca FT Om g1 Jul15 v.2Documento2 páginasAcca FT Om g1 Jul15 v.2Hsn IgcseAinda não há avaliações

- Laptop: We Buy and Sell Second Hand and NewDocumento1 páginaLaptop: We Buy and Sell Second Hand and NewHsn IgcseAinda não há avaliações

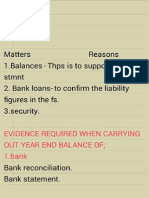

- Audit EvidenceDocumento2 páginasAudit EvidenceHsn IgcseAinda não há avaliações

- Summary of IAS 20 Accounting for Government GrantsDocumento3 páginasSummary of IAS 20 Accounting for Government GrantsHsn IgcseAinda não há avaliações

- CSR Strategy and Strategic CSRDocumento11 páginasCSR Strategy and Strategic CSRHsn Igcse100% (1)

- Bank Amd CashDocumento11 páginasBank Amd CashHsn IgcseAinda não há avaliações

- Using Models in ACCA - P3Documento5 páginasUsing Models in ACCA - P3Hsn IgcseAinda não há avaliações

- Exam Guide Dec 2014 (P2 Corporate Reporting) by Joe FangDocumento2 páginasExam Guide Dec 2014 (P2 Corporate Reporting) by Joe FangHassan Mahmud100% (1)

- Sa August12 1Documento46 páginasSa August12 1accafellowAinda não há avaliações

- Icaew BackgroundDocumento8 páginasIcaew BackgroundHsn IgcseAinda não há avaliações

- Fma Past Paper 3 (F2)Documento24 páginasFma Past Paper 3 (F2)Shereka EllisAinda não há avaliações

- Acca p3 - Professional LevelDocumento31 páginasAcca p3 - Professional Levelmshahza89% (9)

- Acca p3 - Professional LevelDocumento31 páginasAcca p3 - Professional Levelmshahza89% (9)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5784)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)