Você também pode gostar

- Recall: PP Is Now Introduced: Why "CP" and "PP"?Documento33 páginasRecall: PP Is Now Introduced: Why "CP" and "PP"?salmanshahidkhanAinda não há avaliações

- Session IV Combining FactorDocumento44 páginasSession IV Combining FactorImam MumtazAinda não há avaliações

- Annual Worth Analysis: Graw HillDocumento42 páginasAnnual Worth Analysis: Graw HillJason Gabriel JonathanAinda não há avaliações

- Making Choices: The Method, Marr, and Multiple Attributes: Graw HillDocumento139 páginasMaking Choices: The Method, Marr, and Multiple Attributes: Graw HillFebrianti AyuAinda não há avaliações

- 09 - Mutlistage DDM SolutionsDocumento12 páginas09 - Mutlistage DDM SolutionsDilan MandhaneAinda não há avaliações

- Rate of Return Analysis: Single Alternative: Graw HillDocumento57 páginasRate of Return Analysis: Single Alternative: Graw HillJason Gabriel JonathanAinda não há avaliações

- Capital Markets - 4/11/2008Documento1 páginaCapital Markets - 4/11/2008Russell KlusasAinda não há avaliações

- Calculate the present value of pension obligations as of 12/31/2011 and 12/31/2014. Also, calculate the amount of the annual contribution neededDocumento8 páginasCalculate the present value of pension obligations as of 12/31/2011 and 12/31/2014. Also, calculate the amount of the annual contribution neededHalt DougAinda não há avaliações

- There May Case in Which It Is 0 When Total Revenue Is Not Able To Cover TVC. LOOK at Two Things: 1.total Revenue Exceeds Total Variable Cost. 2. MR Cuts MC From BelowDocumento6 páginasThere May Case in Which It Is 0 When Total Revenue Is Not Able To Cover TVC. LOOK at Two Things: 1.total Revenue Exceeds Total Variable Cost. 2. MR Cuts MC From BelowNaeem Ahmed HattarAinda não há avaliações

- Rate of Return Analysis: Single Alternative: Graw HillDocumento44 páginasRate of Return Analysis: Single Alternative: Graw HillJason Gabriel JonathanAinda não há avaliações

- Value of Bonds and Common Stocks: Principles of Corporate FinanceDocumento30 páginasValue of Bonds and Common Stocks: Principles of Corporate FinanceMr BrownstoneAinda não há avaliações

- IPPTChap 003Documento35 páginasIPPTChap 003Ghita RochdiAinda não há avaliações

- TVM NPVDocumento86 páginasTVM NPVChristine Joy Guinhawa DalisayAinda não há avaliações

- Chap9 HM PDFDocumento82 páginasChap9 HM PDFaboudy noureddineAinda não há avaliações

- Kachi Businesss MathematicsDocumento42 páginasKachi Businesss MathematicsGabriel OnalekeAinda não há avaliações

- Annual Worth Analysis: Gra W HillDocumento42 páginasAnnual Worth Analysis: Gra W HillBagus PrakasaAinda não há avaliações

- 2017 Part 1 Section 4 Salary by Years of Experience in QualityDocumento6 páginas2017 Part 1 Section 4 Salary by Years of Experience in QualityadamAinda não há avaliações

- (2021 2022) ACCA FM 基础 答案册Documento22 páginas(2021 2022) ACCA FM 基础 答案册luoyifei1988Ainda não há avaliações

- Texas Instruments BA II Plus (TI BA II+)Documento14 páginasTexas Instruments BA II Plus (TI BA II+)Hasan Tariqul IslamAinda não há avaliações

- 3 Managing Bond PortfoliosDocumento51 páginas3 Managing Bond PortfoliosShazelAinda não há avaliações

- Illustrating Stocks and BondsDocumento6 páginasIllustrating Stocks and Bondsraymond galagAinda não há avaliações

- Capital Alert - 2/1/2008Documento1 páginaCapital Alert - 2/1/2008Russell KlusasAinda não há avaliações

- 36 Comm 308 Final Exam (Winter 2019) - SolutionDocumento15 páginas36 Comm 308 Final Exam (Winter 2019) - SolutionCarl-Henry FrancoisAinda não há avaliações

- brealey-pcf-13e-chap003-ppt-vIJ6Documento38 páginasbrealey-pcf-13e-chap003-ppt-vIJ6Khola KhalilAinda não há avaliações

- Capital Markets - 2/29/2008Documento1 páginaCapital Markets - 2/29/2008Russell KlusasAinda não há avaliações

- Engineering Economy Chapter 5Documento102 páginasEngineering Economy Chapter 5Jason Gabriel JonathanAinda não há avaliações

- 350 CH09Documento12 páginas350 CH09KevinAinda não há avaliações

- Full Download Solution Manual For Financial Accounting Tools For Business Decision Making 9th by Kimmel PDF Full ChapterDocumento36 páginasFull Download Solution Manual For Financial Accounting Tools For Business Decision Making 9th by Kimmel PDF Full Chapterdebbiejacobs73fv100% (18)

- Inverse relationship between bond prices and interest ratesDocumento10 páginasInverse relationship between bond prices and interest ratesNidhi AshokAinda não há avaliações

- Introduction To Valuation: The Time Value of Money: Chapter OrganizationDocumento58 páginasIntroduction To Valuation: The Time Value of Money: Chapter OrganizationAshar Ahmad FastNuAinda não há avaliações

- F5 - Mock A - AnswersDocumento13 páginasF5 - Mock A - AnswersmasangaaxAinda não há avaliações

- An Introduction To Risk and Return-History of Financial Market ReturnsDocumento10 páginasAn Introduction To Risk and Return-History of Financial Market ReturnsanisaAinda não há avaliações

- Chapter 4: Bond and Stock Valuation: Answers To End of Chapter QuestionsDocumento10 páginasChapter 4: Bond and Stock Valuation: Answers To End of Chapter QuestionsAn HoàiAinda não há avaliações

- Ca Final SFM Super 100 Class 6 To 10 1Documento32 páginasCa Final SFM Super 100 Class 6 To 10 1Deepsikha maitiAinda não há avaliações

- Contemporary Mathematics For Business and Consumers Brief Edition 7th Edition Brechner Solutions Manual DownloadDocumento20 páginasContemporary Mathematics For Business and Consumers Brief Edition 7th Edition Brechner Solutions Manual DownloadDonna Hopkins100% (31)

- Rs1,000.00 - Rs1,257.30: Bonds and Bonds ValuationDocumento76 páginasRs1,000.00 - Rs1,257.30: Bonds and Bonds ValuationMomna ShahzadAinda não há avaliações

- Micro Fall 2022 - Grand AssignmentDocumento2 páginasMicro Fall 2022 - Grand AssignmentSaad ManzoorAinda não há avaliações

- Final Ils GenmathDocumento15 páginasFinal Ils GenmathSoichi RiveroAinda não há avaliações

- Approaches to Valuation ModelsDocumento18 páginasApproaches to Valuation ModelsSeemaAinda não há avaliações

- Discussion 2 Time Value of Money ApplicationDocumento2 páginasDiscussion 2 Time Value of Money ApplicationAyat fatimaAinda não há avaliações

- Measures of PositionDocumento15 páginasMeasures of PositionSusan Reyes VinoyaAinda não há avaliações

- Financial Institutions Management - Chapter 6 Solutions PDFDocumento13 páginasFinancial Institutions Management - Chapter 6 Solutions PDFJarrod RodriguesAinda não há avaliações

- Simple Interest and Simple Discount-1Documento16 páginasSimple Interest and Simple Discount-1Prince Marc Cabelleza DanielAinda não há avaliações

- Fundamentals of Corporate Finance 3rd Edition Parrino Solutions Manual DownloadDocumento47 páginasFundamentals of Corporate Finance 3rd Edition Parrino Solutions Manual DownloadSamuel Hobart100% (23)

- Corporate Finance2Documento7 páginasCorporate Finance2Daniel Chris0% (1)

- The Term Structure of Interest Rates ExplainedDocumento3 páginasThe Term Structure of Interest Rates ExplainedottieAinda não há avaliações

- Cases in Finance 3rd Edition Demello Solutions ManualDocumento8 páginasCases in Finance 3rd Edition Demello Solutions ManualMarkFryegtoi100% (37)

- CH03 - 2021 2022 Sem 1Documento83 páginasCH03 - 2021 2022 Sem 1Mathew Chong Vui KitAinda não há avaliações

- Capital Markets - 3/07/2008Documento1 páginaCapital Markets - 3/07/2008Russell KlusasAinda não há avaliações

- Capital Markets - 3/14/2008Documento2 páginasCapital Markets - 3/14/2008Russell KlusasAinda não há avaliações

- Chap 04 and 05 (Mini Case)Documento18 páginasChap 04 and 05 (Mini Case)ricky setiawan100% (1)

- ACCA FM TuitionExam CBE 2021-2022 As JG21Jan SPi15MarDocumento14 páginasACCA FM TuitionExam CBE 2021-2022 As JG21Jan SPi15MarchimbanguraAinda não há avaliações

- Mock Exam 2023 #4 Second Session Corporate Finance, Equity, FixedDocumento86 páginasMock Exam 2023 #4 Second Session Corporate Finance, Equity, Fixedvedant.diwan26Ainda não há avaliações

- Theoretical Approach to Bond ValuationDocumento11 páginasTheoretical Approach to Bond ValuationSebastian MejiaAinda não há avaliações

- Fixed Income Assignment 2Documento4 páginasFixed Income Assignment 2Rattan Preet SinghAinda não há avaliações

- A Student's Guide to Cost-Benefit Analysis for Natural Resources ProjectsDocumento2 páginasA Student's Guide to Cost-Benefit Analysis for Natural Resources ProjectsAlbyziaAinda não há avaliações

- 1solving Problems Involving Measures of PositionDocumento8 páginas1solving Problems Involving Measures of PositionRyan Cris FranciscoAinda não há avaliações

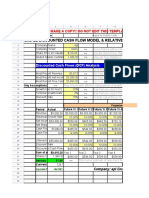

- Simple Discounted Cash Flow Model & Relative ValuationDocumento14 páginasSimple Discounted Cash Flow Model & Relative ValuationlearnAinda não há avaliações

- Spring 2019 Session 9 - Engineering Cost AnalysisDocumento66 páginasSpring 2019 Session 9 - Engineering Cost Analysisnick100% (1)

- Lecture#11Documento20 páginasLecture#11salmanshahidkhanAinda não há avaliações

- ME-102 Engineering GraphicsDocumento23 páginasME-102 Engineering GraphicssalmanshahidkhanAinda não há avaliações

- Lecture#14Documento28 páginasLecture#14salmanshahidkhanAinda não há avaliações

- ME-102 Engineering GraphicsDocumento25 páginasME-102 Engineering GraphicssalmanshahidkhanAinda não há avaliações

- Lecture#1Documento36 páginasLecture#1salmanshahidkhanAinda não há avaliações

- ME-102 Engineering GraphicsDocumento28 páginasME-102 Engineering GraphicssalmanshahidkhanAinda não há avaliações

- ME-102 Engineering GraphicsDocumento19 páginasME-102 Engineering GraphicssalmanshahidkhanAinda não há avaliações

- ME-102 Engineering GraphicsDocumento14 páginasME-102 Engineering GraphicssalmanshahidkhanAinda não há avaliações

- Lecture#11Documento20 páginasLecture#11salmanshahidkhanAinda não há avaliações

- ME-102 Engineering GraphicsDocumento13 páginasME-102 Engineering GraphicssalmanshahidkhanAinda não há avaliações

- ME-102 Engineering GraphicsDocumento20 páginasME-102 Engineering GraphicssalmanshahidkhanAinda não há avaliações

- Lecture#4Documento33 páginasLecture#4salmanshahidkhanAinda não há avaliações

- Circuit Analysis 1: Chapter # 2 Resistive CircuitsDocumento7 páginasCircuit Analysis 1: Chapter # 2 Resistive CircuitssalmanshahidkhanAinda não há avaliações

- Ci Ia Li1 Circuit Analysis 1: Nodal and Loop Analysis TechniquesDocumento12 páginasCi Ia Li1 Circuit Analysis 1: Nodal and Loop Analysis TechniquessalmanshahidkhanAinda não há avaliações

- ME-102 Engineering GraphicsDocumento44 páginasME-102 Engineering GraphicssalmanshahidkhanAinda não há avaliações

- Lecture17 18Documento18 páginasLecture17 18salmanshahidkhanAinda não há avaliações

- Ci Ia Li1 Circuit Analysis 1: Nodal and Loop Analysis TechniquesDocumento12 páginasCi Ia Li1 Circuit Analysis 1: Nodal and Loop Analysis TechniquessalmanshahidkhanAinda não há avaliações

- Ci Ia Li1 Circuit Analysis 1: Nodal and Loop Analysis TechniquesDocumento13 páginasCi Ia Li1 Circuit Analysis 1: Nodal and Loop Analysis TechniquessalmanshahidkhanAinda não há avaliações

- Ci Ita L I1 Circuit Analysis 1: Chapter # 1 Basic ConceptsDocumento17 páginasCi Ita L I1 Circuit Analysis 1: Chapter # 1 Basic ConceptssalmanshahidkhanAinda não há avaliações

- Ci Ita L I1 Circuit Analysis 1: Chapter # 2 Resistive CircuitsDocumento6 páginasCi Ita L I1 Circuit Analysis 1: Chapter # 2 Resistive CircuitssalmanshahidkhanAinda não há avaliações

- Ci Ia Li1 Circuit Analysis 1: Chapter # 2 Resistive CircuitsDocumento11 páginasCi Ia Li1 Circuit Analysis 1: Chapter # 2 Resistive CircuitssalmanshahidkhanAinda não há avaliações

- Ci Ita L I1 Circuit Analysis 1: Chapter # 2 Resistive CircuitsDocumento13 páginasCi Ita L I1 Circuit Analysis 1: Chapter # 2 Resistive CircuitssalmanshahidkhanAinda não há avaliações

- Ci Ia Li1 Circuit Analysis 1: Chapter # 2 Resistive CircuitsDocumento12 páginasCi Ia Li1 Circuit Analysis 1: Chapter # 2 Resistive CircuitssalmanshahidkhanAinda não há avaliações

- Ci Ita L I1 Circuit Analysis 1: Chapter # 1 Basic ConceptsDocumento16 páginasCi Ita L I1 Circuit Analysis 1: Chapter # 1 Basic ConceptssalmanshahidkhanAinda não há avaliações

- Lec 06Documento12 páginasLec 06salmanshahidkhanAinda não há avaliações

- ME 291 Engineering Economy: Simple and Compound InterestDocumento15 páginasME 291 Engineering Economy: Simple and Compound InterestsalmanshahidkhanAinda não há avaliações

- Ci Ita L I1 Circuit Analysis 1: Chapter # 1 Basic ConceptsDocumento14 páginasCi Ita L I1 Circuit Analysis 1: Chapter # 1 Basic ConceptssalmanshahidkhanAinda não há avaliações

- Graw Hill: 17.3 Effect On Taxes of Different Depreciation Methods and Recovery PeriodsDocumento38 páginasGraw Hill: 17.3 Effect On Taxes of Different Depreciation Methods and Recovery PeriodssalmanshahidkhanAinda não há avaliações

- Section 5.7 Life Cycle Costs: Authored by Don Smith, Texas A&M University 2004Documento29 páginasSection 5.7 Life Cycle Costs: Authored by Don Smith, Texas A&M University 2004salmanshahidkhanAinda não há avaliações

- Graw Hill: 17.1 Income Tax Terminology and Relations For Corporations and IndividualsDocumento33 páginasGraw Hill: 17.1 Income Tax Terminology and Relations For Corporations and IndividualssalmanshahidkhanAinda não há avaliações

- JAVIER - RLA - CWTS103 - A72 - Project Financial ReportDocumento2 páginasJAVIER - RLA - CWTS103 - A72 - Project Financial ReportRome Lauren JavierAinda não há avaliações

- Authority To Sell FORMDocumento2 páginasAuthority To Sell FORMSuzi Garcia-RufinoAinda não há avaliações

- 2 Financial Reporting Theory UpdatedDocumento52 páginas2 Financial Reporting Theory UpdatedSiham OsmanAinda não há avaliações

- MCQ For Practise (Pre-Mids Topics) PDFDocumento6 páginasMCQ For Practise (Pre-Mids Topics) PDFAliAinda não há avaliações

- ComplaintDocumento32 páginasComplaintmikelintonAinda não há avaliações

- Pertemuan 6 - Financial AnalysisDocumento35 páginasPertemuan 6 - Financial Analysisdyah ayu kusuma wardhaniAinda não há avaliações

- Cost Assignment IDocumento5 páginasCost Assignment Ifitsum100% (1)

- NORTHERN TRUST CORPORATION OWNS IRSDocumento3 páginasNORTHERN TRUST CORPORATION OWNS IRStravis smithAinda não há avaliações

- ICAI professionals competency mappingDocumento3 páginasICAI professionals competency mappingसिद्धार्थ शुक्लाAinda não há avaliações

- Principal and Agent: Joseph E. StiglitzDocumento13 páginasPrincipal and Agent: Joseph E. StiglitzRamiro EnriquezAinda não há avaliações

- What Is Microfinance and What Does It PromiseDocumento16 páginasWhat Is Microfinance and What Does It PromiseZahid BhatAinda não há avaliações

- GIC Report 2019 20 1Documento84 páginasGIC Report 2019 20 1a aaaAinda não há avaliações

- Credit Ratings in Insurance Regulation: The Missing Piece of Financial ReformDocumento32 páginasCredit Ratings in Insurance Regulation: The Missing Piece of Financial ReformRishi KumarAinda não há avaliações

- Charge (Short Note)Documento3 páginasCharge (Short Note)Srishti GoelAinda não há avaliações

- Accounting ConceptsDocumento32 páginasAccounting ConceptsSarika KeswaniAinda não há avaliações

- BRM v3-1 Taxonomy 20130615Documento52 páginasBRM v3-1 Taxonomy 20130615kevinzhang2022Ainda não há avaliações

- Beck Fed IncomeTax OutlineDocumento106 páginasBeck Fed IncomeTax OutlineEvan Joseph100% (1)

- Praktek Akuntansi PD UD Buana (Kevin Jonathan)Documento67 páginasPraktek Akuntansi PD UD Buana (Kevin Jonathan)kevin jonathanAinda não há avaliações

- C VDocumento8 páginasC VAnonymous K8uhur100% (1)

- Smartphone Melsie C. TudtudDocumento10 páginasSmartphone Melsie C. TudtudEdmon FuentesAinda não há avaliações

- Statement of AccountDocumento2 páginasStatement of Accountmdyakubhnk85Ainda não há avaliações

- Calculating partnership profits and capital balancesDocumento1 páginaCalculating partnership profits and capital balancesDe Nev Oel0% (1)

- Internship Report on Consumer Banking at United Bank LimitedDocumento48 páginasInternship Report on Consumer Banking at United Bank LimitedGul ZareenAinda não há avaliações

- Caltex v COA: No offsetting of taxes against claimsDocumento1 páginaCaltex v COA: No offsetting of taxes against claimsHarvey Leo RomanoAinda não há avaliações

- Republic Planters Bank Vs CADocumento2 páginasRepublic Planters Bank Vs CAMohammad Yusof Mauna MacalandapAinda não há avaliações

- EFU Life Insurance Group ReportDocumento20 páginasEFU Life Insurance Group ReportZawar Afzal Khan0% (1)

- Leibowitz - Franchise Value PDFDocumento512 páginasLeibowitz - Franchise Value PDFDavidAinda não há avaliações

- Valuation Report DCF Power CompanyDocumento34 páginasValuation Report DCF Power CompanySid EliAinda não há avaliações

- Unit I Introduction To Marketing FinanceDocumento3 páginasUnit I Introduction To Marketing Financerajesh laddhaAinda não há avaliações

- Sample Solved Question Papers For IRDA 50 Hours Agents Training ExamDocumento15 páginasSample Solved Question Papers For IRDA 50 Hours Agents Training ExamPurnendu Sarkar100% (3)