Você também pode gostar

- Startups BookDocumento261 páginasStartups BookChris Dixon67% (3)

- 2015.07.04 - The Curious Case of IDBI Call - Put Option Bonds - HongKongDocumento9 páginas2015.07.04 - The Curious Case of IDBI Call - Put Option Bonds - HongKongJoseph SathyanAinda não há avaliações

- Swot Analysis of Asset ClassesDocumento5 páginasSwot Analysis of Asset ClassesRakkuyil Sarath33% (3)

- Mission Statements of NikeDocumento12 páginasMission Statements of Nikemkam212Ainda não há avaliações

- Exempt IncomeDocumento18 páginasExempt IncomeSarvar PathanAinda não há avaliações

- Credit Monitoring and Follow-Up: MeaningDocumento23 páginasCredit Monitoring and Follow-Up: Meaningpuran1234567890100% (2)

- GST Act, 2017-SorDocumento6 páginasGST Act, 2017-SorMohit NagarAinda não há avaliações

- NetFlix Case StudyDocumento24 páginasNetFlix Case Studykaran dattaniAinda não há avaliações

- Target Corporation Marketing PlanDocumento17 páginasTarget Corporation Marketing PlankarinadanielAinda não há avaliações

- Assignment of Management of Working Capital: TopicDocumento13 páginasAssignment of Management of Working Capital: TopicDavinder Singh Banss0% (1)

- Term Loans PPT 2003Documento30 páginasTerm Loans PPT 2003gayathrihari100% (2)

- Share CapitalDocumento21 páginasShare CapitalMehal Ur RahmanAinda não há avaliações

- Benefits of Global Accounting StandardsDocumento16 páginasBenefits of Global Accounting StandardsJones EdombingoAinda não há avaliações

- Key Terminology in Clearing and Sattelment Process NSEDocumento9 páginasKey Terminology in Clearing and Sattelment Process NSETushali TrivediAinda não há avaliações

- Parts Warehouse Company PresentationDocumento12 páginasParts Warehouse Company PresentationIsha UpadhyayAinda não há avaliações

- Lecture 2 Forwards&FuturesPricing NewDocumento48 páginasLecture 2 Forwards&FuturesPricing NewAniruddha DeyAinda não há avaliações

- Cash Flow Statement Analysis Hul FinalDocumento10 páginasCash Flow Statement Analysis Hul FinalGursimran SinghAinda não há avaliações

- Powered by Ninja X SamuraiDocumento2 páginasPowered by Ninja X SamuraiArkadeep TalukderAinda não há avaliações

- Future TerminologyDocumento9 páginasFuture TerminologyavinishAinda não há avaliações

- Impact of Dividend Policy On Value of The Final)Documento40 páginasImpact of Dividend Policy On Value of The Final)finesaqibAinda não há avaliações

- Factoring and ForfaitingDocumento34 páginasFactoring and ForfaitingStone HsuAinda não há avaliações

- Captial Structure Trend in Indian Steel IndustryDocumento76 páginasCaptial Structure Trend in Indian Steel Industryjitendra jaushik50% (2)

- Project Report: Pune UniversityDocumento58 páginasProject Report: Pune UniversityMayur N Malviya100% (1)

- Q. 16 Functions of A Merchant BankerDocumento3 páginasQ. 16 Functions of A Merchant BankerMAHENDRA SHIVAJI DHENAKAinda não há avaliações

- Financial Services NotesDocumento62 páginasFinancial Services NotesHari Haran MAinda não há avaliações

- 5.calculation of EPSDocumento6 páginas5.calculation of EPSVinitgaAinda não há avaliações

- Legal Aspects M & ADocumento15 páginasLegal Aspects M & ATwinkal chakradhari100% (1)

- 6 BondDocumento18 páginas6 Bondßïshñü PhüyãlAinda não há avaliações

- FD 2Documento5 páginasFD 2Nikita Shekhawat100% (1)

- Session 1 - Classification of Export FinanceDocumento28 páginasSession 1 - Classification of Export FinanceJc Duke M Eliyasar100% (1)

- Primary MarketDocumento27 páginasPrimary MarketMrunal Chetan Josih0% (1)

- Regulatory Framework For Financial Services in IndiaDocumento25 páginasRegulatory Framework For Financial Services in IndiaBishnu PhukanAinda não há avaliações

- Unit 2 Structure of of Options MarketsDocumento36 páginasUnit 2 Structure of of Options MarketsTorreus AdhikariAinda não há avaliações

- Mutual Fund Operation Flow ChartDocumento76 páginasMutual Fund Operation Flow ChartjeevanAinda não há avaliações

- Mission and Vision 2020Documento4 páginasMission and Vision 2020paschal makoyeAinda não há avaliações

- Pre ShipmentDocumento8 páginasPre ShipmentRajesh ShahAinda não há avaliações

- Credit Rating ProcessDocumento36 páginasCredit Rating ProcessBhuvi SharmaAinda não há avaliações

- Fin Statement Analysis - Atlas BatteryDocumento34 páginasFin Statement Analysis - Atlas BatterytabinahassanAinda não há avaliações

- Stock Brokers Role in Nepal Docx - PDF (MAHESH) PDFDocumento6 páginasStock Brokers Role in Nepal Docx - PDF (MAHESH) PDFMahesh JoshiAinda não há avaliações

- Tax PlanningDocumento109 páginasTax PlanningrahulAinda não há avaliações

- Information MemorandumDocumento29 páginasInformation MemorandumAditya Lakhani100% (1)

- Kingfisher Airlines Annual Report 2011 12Documento85 páginasKingfisher Airlines Annual Report 2011 12Neha DhuriAinda não há avaliações

- FM Sheet 4 (JUHI RAJWANI)Documento8 páginasFM Sheet 4 (JUHI RAJWANI)Mukesh SinghAinda não há avaliações

- Various Types of Companies Under Companies Act, 1956-11Documento54 páginasVarious Types of Companies Under Companies Act, 1956-11Upneet Sethi67% (3)

- Model PAPER-Analysis of Financial Statement - MBA-BBADocumento5 páginasModel PAPER-Analysis of Financial Statement - MBA-BBAvelas4100% (1)

- Emerging Trends in Capital MarketDocumento20 páginasEmerging Trends in Capital MarketAvinash Hacholli0% (1)

- 5.1 Receivable ManagementDocumento18 páginas5.1 Receivable ManagementJoshua Cabinas100% (1)

- Equity ResearchDocumento14 páginasEquity ResearchMohit ModiAinda não há avaliações

- FCCBDocumento14 páginasFCCBVanessa DavisAinda não há avaliações

- Ge MatrixDocumento9 páginasGe MatrixAshiq NobitaAinda não há avaliações

- Discount and Finance House of IndiaDocumento25 páginasDiscount and Finance House of Indiavikram_bansal_5Ainda não há avaliações

- Asset and LiabilityDocumento30 páginasAsset and LiabilitymailsubratapaulAinda não há avaliações

- Introduction On Money Market 01Documento41 páginasIntroduction On Money Market 01Hima HaridasAinda não há avaliações

- Questions On LeasingDocumento5 páginasQuestions On Leasingriteshsoni100% (2)

- Bond Valuation: Anita RamanDocumento35 páginasBond Valuation: Anita RamanTanmay MehtaAinda não há avaliações

- Mercantile Bank Working Capital ManagementDocumento20 páginasMercantile Bank Working Capital ManagementMidul Khan100% (1)

- Anti Takeover Amendments - MergersDocumento7 páginasAnti Takeover Amendments - MergersBalajiAinda não há avaliações

- IGNOU MBA MS - 04 Solved Assignment 2011Documento12 páginasIGNOU MBA MS - 04 Solved Assignment 2011Nazif LcAinda não há avaliações

- Term LoanDocumento8 páginasTerm LoanDarshan PatilAinda não há avaliações

- Vce Summer Internship Program 2020 (PROJECT FINANCE-Modelling and Analysis)Documento9 páginasVce Summer Internship Program 2020 (PROJECT FINANCE-Modelling and Analysis)vedantAinda não há avaliações

- Process in Project Finance and The Information MemorandumDocumento3 páginasProcess in Project Finance and The Information Memorandummutale besa100% (1)

- Project MGT Mod 3Documento16 páginasProject MGT Mod 3rahulking219Ainda não há avaliações

- Engineering Graphics 2004Documento3 páginasEngineering Graphics 2004Hardik SharmaAinda não há avaliações

- Engineering Graphics - I 2003Documento4 páginasEngineering Graphics - I 2003Hardik SharmaAinda não há avaliações

- Job Compatibility QuestionnaireDocumento4 páginasJob Compatibility QuestionnaireHardik Sharma0% (1)

- Engineering Graphics 2002Documento2 páginasEngineering Graphics 2002Hardik SharmaAinda não há avaliações

- Engineering Graphics 2002 PDFDocumento2 páginasEngineering Graphics 2002 PDFHardik SharmaAinda não há avaliações

- Mechanics of A-B-C AnalysisDocumento4 páginasMechanics of A-B-C AnalysisHardik SharmaAinda não há avaliações

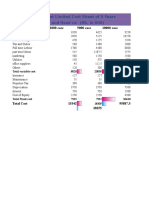

- Ashank Winer Privet Limited Cost Sheet of 5 Years Total Variable Cost and Fixed Cos (RS. in 000)Documento4 páginasAshank Winer Privet Limited Cost Sheet of 5 Years Total Variable Cost and Fixed Cos (RS. in 000)Hardik SharmaAinda não há avaliações

- RegressionDocumento87 páginasRegressionHardik Sharma100% (1)

- French BenifitsDocumento63 páginasFrench BenifitsHardik SharmaAinda não há avaliações

- Financial ManagementDocumento48 páginasFinancial ManagementHardik SharmaAinda não há avaliações

- Prototypin G: Gattani Neha Brijmohan ROLL NO.14081 MBA-1Documento11 páginasPrototypin G: Gattani Neha Brijmohan ROLL NO.14081 MBA-1Hardik SharmaAinda não há avaliações

- Inventory Software: Application Software On Inventory of Textile Trading CompanyDocumento9 páginasInventory Software: Application Software On Inventory of Textile Trading CompanyHardik SharmaAinda não há avaliações

- 16793theory of CostDocumento54 páginas16793theory of CostHardik SharmaAinda não há avaliações

- Data vs. InformationDocumento72 páginasData vs. InformationHardik SharmaAinda não há avaliações

- 104-Me 1443017742071Documento82 páginas104-Me 1443017742071Hardik SharmaAinda não há avaliações

- Law 1Documento73 páginasLaw 1Hardik SharmaAinda não há avaliações

- B-Sale of GoodsDocumento21 páginasB-Sale of GoodsHardik SharmaAinda não há avaliações

- Interest RatesDocumento54 páginasInterest RatesAmeen ShaikhAinda não há avaliações

- Ea 1Documento20 páginasEa 1Ella LawanAinda não há avaliações

- FIM Question Practice 2Documento15 páginasFIM Question Practice 2Bao Khanh HaAinda não há avaliações

- Chapter 2Documento50 páginasChapter 2junrexAinda não há avaliações

- Test Prog3Documento7 páginasTest Prog3Kimberly HunterAinda não há avaliações

- Cost & Management Accounting: Riya Gupta - 21PGDM012Documento11 páginasCost & Management Accounting: Riya Gupta - 21PGDM012RIYA GUPTAAinda não há avaliações

- Applied Economics (MIDTERM EXAM) SENIORDocumento2 páginasApplied Economics (MIDTERM EXAM) SENIORJoan Mae Angot - VillegasAinda não há avaliações

- Cost Accounting Mastery - 1Documento4 páginasCost Accounting Mastery - 1Mark RevarezAinda não há avaliações

- IIFA Country Reports 2010Documento271 páginasIIFA Country Reports 2010alper55kAinda não há avaliações

- Soal Akuntansi ManajemenDocumento7 páginasSoal Akuntansi ManajemenInten RosmalinaAinda não há avaliações

- Lesson Two-3Documento10 páginasLesson Two-3Ruth NyawiraAinda não há avaliações

- SCMPE Important Theory Topics For ExamDocumento44 páginasSCMPE Important Theory Topics For ExamGopikumar ChintalaAinda não há avaliações

- Electrifying City Logistics in The European Union: Optimising Charging Saves CostDocumento3 páginasElectrifying City Logistics in The European Union: Optimising Charging Saves CostThe International Council on Clean TransportationAinda não há avaliações

- Transposition of Formulae and National Income DeterminationDocumento3 páginasTransposition of Formulae and National Income DeterminationH EvelynAinda não há avaliações

- Feasib Feasibility Study 2Documento79 páginasFeasib Feasibility Study 2Irish Keith SanchezAinda não há avaliações

- RII (Renewal Rewrite), Effective Date 20221128, Transaction 00280Documento16 páginasRII (Renewal Rewrite), Effective Date 20221128, Transaction 00280Pete PoliAinda não há avaliações

- Chemical Engineering Economics: Dr. Ir. Ahmad Rifandi, MSC., Cert IvDocumento88 páginasChemical Engineering Economics: Dr. Ir. Ahmad Rifandi, MSC., Cert Iviqbal m farizAinda não há avaliações

- Far PreweekDocumento18 páginasFar PreweekHarvey OchoaAinda não há avaliações

- Personal Assignment Inventory (Materi 5)Documento2 páginasPersonal Assignment Inventory (Materi 5)Cita Setia RahmiAinda não há avaliações

- Libya Since 1969 - Qadhafis Revolution Revisited - Dirk Vandewalle 2008 PDFDocumento268 páginasLibya Since 1969 - Qadhafis Revolution Revisited - Dirk Vandewalle 2008 PDFAbid ChaudhryAinda não há avaliações

- Test Your Knowledge: Theoretical QuestionsDocumento30 páginasTest Your Knowledge: Theoretical QuestionsRITZ BROWN50% (2)

- Ch. 2 Directed Reading GuideDocumento9 páginasCh. 2 Directed Reading GuideOtabek KhamidovAinda não há avaliações

- Chart of Accounts: Account Type Income Tax LineDocumento4 páginasChart of Accounts: Account Type Income Tax LineNak VanAinda não há avaliações

- Dr. Filemon C. Aguilar Memorial College of Las Piñas: Aced 4 - Managerial EconomicsDocumento7 páginasDr. Filemon C. Aguilar Memorial College of Las Piñas: Aced 4 - Managerial Economicsmaelyn calindongAinda não há avaliações

- Name of Work: Town Municipal CouncilDocumento38 páginasName of Work: Town Municipal CouncilmaniannanAinda não há avaliações

- Cosmetics and Toiletries To Hong KongDocumento5 páginasCosmetics and Toiletries To Hong KongTzinNui ChongAinda não há avaliações