Você também pode gostar

- Yellow King - Black Star MagicDocumento186 páginasYellow King - Black Star Magicwijeesf797100% (1)

- Return To The Source Selected Speeches of Amilcar CabralDocumento112 páginasReturn To The Source Selected Speeches of Amilcar Cabraldjazzy456Ainda não há avaliações

- Excels For Solution ManualDocumento116 páginasExcels For Solution ManualDimple PandeyAinda não há avaliações

- U.S. Strategy For Pakistan and AfghanistanDocumento112 páginasU.S. Strategy For Pakistan and AfghanistanCouncil on Foreign Relations100% (2)

- Allison Serie 9800Documento2 páginasAllison Serie 9800Anonymous TEbcqw5RbT100% (1)

- Regression Analysis ProjectDocumento4 páginasRegression Analysis ProjectAsif. MahamudAinda não há avaliações

- How Charts Can Make You Money: An Investor’s Guide to Technical AnalysisNo EverandHow Charts Can Make You Money: An Investor’s Guide to Technical AnalysisAinda não há avaliações

- Agile Data Warehouse Design For Big Data Presentation (720p - 30fps - H264-192kbit - AAC) PDFDocumento90 páginasAgile Data Warehouse Design For Big Data Presentation (720p - 30fps - H264-192kbit - AAC) PDFMatian Dal100% (2)

- QUAMA000Documento41 páginasQUAMA000Abd ZouhierAinda não há avaliações

- Open Data Driving Growth Ingenuity and InnovationDocumento36 páginasOpen Data Driving Growth Ingenuity and InnovationAnonymous EBlYNQbiMyAinda não há avaliações

- Phrasal Verbs and IdiomaticDocumento9 páginasPhrasal Verbs and IdiomaticAbidah Sarajul Haq100% (1)

- MKTG 376 Assignment 2Documento5 páginasMKTG 376 Assignment 2api-506531415Ainda não há avaliações

- Second Assessment - Unknown - LakesDocumento448 páginasSecond Assessment - Unknown - LakesCarlos Sánchez LópezAinda não há avaliações

- Risk and Return: An Overview of Capital Market TheoryDocumento11 páginasRisk and Return: An Overview of Capital Market Theorytarunsoni88Ainda não há avaliações

- Multiplier ModelDocumento20 páginasMultiplier ModelANJULI AGARWALAinda não há avaliações

- Iapm SolutionsDocumento81 páginasIapm Solutionsjayaram_polarisAinda não há avaliações

- National Account Statistics: Hersch SahayDocumento37 páginasNational Account Statistics: Hersch SahayShivam ChatterjeeAinda não há avaliações

- Solutions ChandraDocumento80 páginasSolutions ChandraKunle OketoboAinda não há avaliações

- Lecture 4 Agriculture SectorDocumento27 páginasLecture 4 Agriculture SectorShiwani BalaniAinda não há avaliações

- Equivalent Concrete Strength - Advance-B1-COLUMNDocumento7 páginasEquivalent Concrete Strength - Advance-B1-COLUMNWahid wrbelAinda não há avaliações

- Lecture 4 Agriculture SectorDocumento25 páginasLecture 4 Agriculture SectorYumna HasnainAinda não há avaliações

- Petro NCR 2022-Jul-28Documento2 páginasPetro NCR 2022-Jul-28Nida SaingAinda não há avaliações

- Petro Nluz 2023-Jun-30Documento7 páginasPetro Nluz 2023-Jun-30johnis19dcAinda não há avaliações

- Year Nominal GDP at Market Price With Base Year of 2004-05 Real GDP at Market Price With Base Year 2004-05Documento10 páginasYear Nominal GDP at Market Price With Base Year of 2004-05 Real GDP at Market Price With Base Year 2004-05Rajat RanjanAinda não há avaliações

- M. Khafid - 74 A - 18reg74079 - Tugas SBD 1Documento5 páginasM. Khafid - 74 A - 18reg74079 - Tugas SBD 1KhafidAnkaAinda não há avaliações

- Exam 2 ReviewDocumento53 páginasExam 2 ReviewNkeih FidelisAinda não há avaliações

- Sample Paper 1Documento8 páginasSample Paper 1MohanAinda não há avaliações

- Tax and Investment Planning Seminar HighlightsDocumento31 páginasTax and Investment Planning Seminar Highlightsgunduanil17Ainda não há avaliações

- Petro NCR 2022 Nov 10Documento2 páginasPetro NCR 2022 Nov 10Justine CastilloAinda não há avaliações

- 2D Ms Excel Intermediate and Advance 2021 Perodua 10112021Documento164 páginas2D Ms Excel Intermediate and Advance 2021 Perodua 10112021Syahrum ShukriAinda não há avaliações

- Financial Analysis of Textile Companies FraDocumento2 páginasFinancial Analysis of Textile Companies FraN SethAinda não há avaliações

- Pertemuan 6 Portfolio Risk and Return IDocumento35 páginasPertemuan 6 Portfolio Risk and Return IFani HuangAinda não há avaliações

- Contoh Part ConsumableDocumento4 páginasContoh Part ConsumableJ EquipAinda não há avaliações

- Franklin 2018 SIP-PresentationDocumento24 páginasFranklin 2018 SIP-PresentationRajat GuptaAinda não há avaliações

- CH 04 RevisedDocumento20 páginasCH 04 RevisedPrakash PandeyAinda não há avaliações

- Pemrograman DasarDocumento24 páginasPemrograman DasarYoga AndriyantoAinda não há avaliações

- CH 04 RevisedDocumento20 páginasCH 04 RevisedAnkit GuptaAinda não há avaliações

- Statistics For Managerial Decision: Project Report On Regression AnalysisDocumento4 páginasStatistics For Managerial Decision: Project Report On Regression AnalysisAsif. MahamudAinda não há avaliações

- Exercise Mining FinanceDocumento3 páginasExercise Mining FinanceJhon Jairo CiezaAinda não há avaliações

- Project cash flow analysis and investment metricsDocumento2 páginasProject cash flow analysis and investment metricscatharina arnitaAinda não há avaliações

- Capital FormationDocumento20 páginasCapital FormationAdeel AhmadAinda não há avaliações

- Portfolio Risk and Return: Part I: Presenter Venue DateDocumento35 páginasPortfolio Risk and Return: Part I: Presenter Venue DateahmedAinda não há avaliações

- PGP 1920 IE Lec 2 Agg SCRDocumento26 páginasPGP 1920 IE Lec 2 Agg SCRDevendra MahajanAinda não há avaliações

- Erc - Mac-III Cost of ProdDocumento11 páginasErc - Mac-III Cost of ProdMallikarjun GAinda não há avaliações

- Risk and Return Risk and ReturnDocumento64 páginasRisk and Return Risk and ReturnRaman SharmaAinda não há avaliações

- Trinidad and Tobago diversification-KBenjamin - DSinanan - CORM - 2012Documento20 páginasTrinidad and Tobago diversification-KBenjamin - DSinanan - CORM - 2012jefferyleclercAinda não há avaliações

- SMA NEGERI 1 JEUMPA PUTEH BANDA ACEH FISIKA DAFTAR NILAI 2018-2019Documento9 páginasSMA NEGERI 1 JEUMPA PUTEH BANDA ACEH FISIKA DAFTAR NILAI 2018-2019Tgk lina rahmaliaAinda não há avaliações

- EFM - MSESPM - Lec 5 - Risk and Return - Chapt4 - 2020Documento21 páginasEFM - MSESPM - Lec 5 - Risk and Return - Chapt4 - 2020RabinAinda não há avaliações

- Fiscal Policy GuideDocumento19 páginasFiscal Policy Guidevikas rathoreAinda não há avaliações

- Months Demand Moving Average - A-F - Weighte D Moving Average - A-F - JAN FEB MAR APR MAY June TotalDocumento2 páginasMonths Demand Moving Average - A-F - Weighte D Moving Average - A-F - JAN FEB MAR APR MAY June TotalIkhmal AlifAinda não há avaliações

- Rincian Biaya Perjalanan DinasDocumento11 páginasRincian Biaya Perjalanan Dinasheppy prastyo nugrohoAinda não há avaliações

- Petro Sluz 2022 Dec 27 Batangas Rizal QuezonDocumento2 páginasPetro Sluz 2022 Dec 27 Batangas Rizal QuezonFloyd PantiAinda não há avaliações

- Capital Budgeting Spreadsheet Tools - Summer 2020Documento14 páginasCapital Budgeting Spreadsheet Tools - Summer 2020Reshma mansinghaniAinda não há avaliações

- UK - Relative Humidity ChartsDocumento11 páginasUK - Relative Humidity ChartsShamaAinda não há avaliações

- National Quickstat September2021 - 27Documento6 páginasNational Quickstat September2021 - 27Jibreen TaugAinda não há avaliações

- Chapter 18 PowerPointDocumento20 páginasChapter 18 PowerPointfitriawasilatulastifahAinda não há avaliações

- Portfolio Risk and Return: Part I: Presenter Venue DateDocumento35 páginasPortfolio Risk and Return: Part I: Presenter Venue DateahmedAinda não há avaliações

- Session-8 Capital BudgetingDocumento11 páginasSession-8 Capital BudgetingKishan TCAinda não há avaliações

- Tugas Return and RiskDocumento6 páginasTugas Return and RiskFebry AnggaAinda não há avaliações

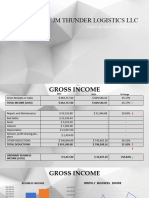

- JM Thunder LogisticsDocumento5 páginasJM Thunder LogisticsJan Ray Oviedo EscotoAinda não há avaliações

- The Body Shop Plc 2001: Historical Financial AnalysisDocumento13 páginasThe Body Shop Plc 2001: Historical Financial AnalysisNaman Nepal100% (1)

- Quantitative Forecasting Methods in 40 CharactersDocumento18 páginasQuantitative Forecasting Methods in 40 CharactersUmar IsmailAinda não há avaliações

- Tugas II Ekonometri I: Analisis Hubungan Harga Emas, Indeks Saham, dan InflasiDocumento11 páginasTugas II Ekonometri I: Analisis Hubungan Harga Emas, Indeks Saham, dan InflasiMuhammad Faisal LathiefAinda não há avaliações

- Random Motor SheetDocumento31 páginasRandom Motor SheetAndy KumarAinda não há avaliações

- Chapter 12 Bond Portfolio MGMTDocumento32 páginasChapter 12 Bond Portfolio MGMTAanchalAinda não há avaliações

- National Parks Percentage of Visitors Current YearDocumento4 páginasNational Parks Percentage of Visitors Current YearSarahMae bumagatAinda não há avaliações

- Current Affairs NotesDocumento9 páginasCurrent Affairs NotesAkash saxena100% (1)

- CH 35Documento26 páginasCH 35Pankaj KumarAinda não há avaliações

- Tajmahal WonderofworlddineshvoraDocumento23 páginasTajmahal WonderofworlddineshvoraAkash saxenaAinda não há avaliações

- CH 034Documento19 páginasCH 034Akash saxenaAinda não há avaliações

- Chapter - 33: Derivatives For Managing Financial RiskDocumento21 páginasChapter - 33: Derivatives For Managing Financial RiskAkash saxenaAinda não há avaliações

- ICC CWC 2011 Official Ticket GuideDocumento28 páginasICC CWC 2011 Official Ticket GuideDinesh KumarAinda não há avaliações

- CH 36Documento34 páginasCH 36rameshmbaAinda não há avaliações

- Chapter - 30: Cash ManagementDocumento20 páginasChapter - 30: Cash ManagementAkash saxenaAinda não há avaliações

- CH 022Documento23 páginasCH 022Akash saxenaAinda não há avaliações

- Chapter - 28: Receivables Management and FactoringDocumento11 páginasChapter - 28: Receivables Management and FactoringAkash saxenaAinda não há avaliações

- Chapter - 31: Working Capital FinanceDocumento13 páginasChapter - 31: Working Capital FinanceAkash saxenaAinda não há avaliações

- Chapter - 23: Venture Capital FinancingDocumento11 páginasChapter - 23: Venture Capital FinancingAkash saxenaAinda não há avaliações

- Chapter - 27: Principles of Working Capital ManagementDocumento17 páginasChapter - 27: Principles of Working Capital ManagementAkash saxenaAinda não há avaliações

- Chapter - 29: Inventory ManagementDocumento10 páginasChapter - 29: Inventory ManagementAkash saxenaAinda não há avaliações

- Chapter - 25: Financial Statement AnalysisDocumento21 páginasChapter - 25: Financial Statement AnalysisAkash saxenaAinda não há avaliações

- Chapter - 17: Dividend TheoryDocumento18 páginasChapter - 17: Dividend TheoryAkash saxenaAinda não há avaliações

- Chapter - 24: Financial Statements and Cash Flow AnalysisDocumento39 páginasChapter - 24: Financial Statements and Cash Flow AnalysisAkash saxenaAinda não há avaliações

- CH 21Documento9 páginasCH 21rameshmbaAinda não há avaliações

- Chapter - 12: Risk Analysis in Capital BudgetingDocumento28 páginasChapter - 12: Risk Analysis in Capital BudgetingAkash saxenaAinda não há avaliações

- Chapter - 19: Capital Market Efficiency and Capital Markets in IndiaDocumento6 páginasChapter - 19: Capital Market Efficiency and Capital Markets in IndiaAkash saxenaAinda não há avaliações

- Chapter - 20: Long Term Finance: Shares, Debentures and Term LoansDocumento12 páginasChapter - 20: Long Term Finance: Shares, Debentures and Term LoansAkash saxenaAinda não há avaliações

- Chapter - 10: Determining Cash Flows For Investment AnalysisDocumento15 páginasChapter - 10: Determining Cash Flows For Investment AnalysisAkash saxenaAinda não há avaliações

- CH 014Documento17 páginasCH 014Akash saxenaAinda não há avaliações

- CH - 18visit Us at Management - Umakant.infoDocumento6 páginasCH - 18visit Us at Management - Umakant.infowelcome2jungleAinda não há avaliações

- CH - 16visit Us at Management - Umakant.infoDocumento28 páginasCH - 16visit Us at Management - Umakant.infowelcome2jungleAinda não há avaliações

- Chapter - 15: Capital Structure Theory and PolicyDocumento32 páginasChapter - 15: Capital Structure Theory and PolicyAkash saxenaAinda não há avaliações

- CH 013Documento17 páginasCH 013Akash saxenaAinda não há avaliações

- CH 008Documento45 páginasCH 008Akash saxenaAinda não há avaliações

- Chapter - 11: Complex Investment DecisionsDocumento15 páginasChapter - 11: Complex Investment DecisionsAkash saxenaAinda não há avaliações

- Chapter - 7: Options and Their ValuationDocumento29 páginasChapter - 7: Options and Their ValuationAkash saxenaAinda não há avaliações

- Kythera S-1 Ex. 99.1Documento471 páginasKythera S-1 Ex. 99.1darwinbondgrahamAinda não há avaliações

- Bibliography of the Butterworth TrialDocumento3 páginasBibliography of the Butterworth TrialmercurymomAinda não há avaliações

- Paper 3 IBIMA Brand Loyalty Page 2727-2738Documento82 páginasPaper 3 IBIMA Brand Loyalty Page 2727-2738Sri Rahayu Hijrah HatiAinda não há avaliações

- 19 Preposition of PersonalityDocumento47 páginas19 Preposition of Personalityshoaibmirza1Ainda não há avaliações

- Financial Reporting Quality and Investment Efficiency - Evidence F PDFDocumento12 páginasFinancial Reporting Quality and Investment Efficiency - Evidence F PDFRenjani Lulu SafitriAinda não há avaliações

- Specific Gravity of FluidDocumento17 páginasSpecific Gravity of FluidPriyanathan ThayalanAinda não há avaliações

- What's New: Activity 1.2 ModelDocumento3 páginasWhat's New: Activity 1.2 ModelJonrheym RemegiaAinda não há avaliações

- Astm d4921Documento2 páginasAstm d4921CeciliagorraAinda não há avaliações

- Shot List Farm To FridgeDocumento3 páginasShot List Farm To Fridgeapi-704594167Ainda não há avaliações

- First CaseDocumento2 páginasFirst Caseaby marieAinda não há avaliações

- HCB 0207 Insurance Ad Risk ManagementDocumento2 páginasHCB 0207 Insurance Ad Risk Managementcollostero6Ainda não há avaliações

- GonorrhoeaDocumento24 páginasGonorrhoeaAtreyo ChakrabortyAinda não há avaliações

- University Student Council: University of The Philippines Los BañosDocumento10 páginasUniversity Student Council: University of The Philippines Los BañosSherwin CambaAinda não há avaliações

- ACC8278 Annual Report 2021Documento186 páginasACC8278 Annual Report 2021mikeAinda não há avaliações

- In - Gov.uidai ADHARDocumento1 páginaIn - Gov.uidai ADHARvamsiAinda não há avaliações

- Marketing MetricsDocumento29 páginasMarketing Metricscameron.king1202Ainda não há avaliações

- Taste of IndiaDocumento8 páginasTaste of IndiaDiki RasaptaAinda não há avaliações

- The Night Artist ComprehensionDocumento6 páginasThe Night Artist ComprehensionDana TanAinda não há avaliações

- Axis Priority SalaryDocumento5 páginasAxis Priority SalarymanojAinda não há avaliações

- Lec 2Documento10 páginasLec 2amitava deyAinda não há avaliações

- MPRC - OGSE100 FY2020 Report - 0Documento48 páginasMPRC - OGSE100 FY2020 Report - 0adamAinda não há avaliações

- Recruitment On The InternetDocumento8 páginasRecruitment On The InternetbgbhattacharyaAinda não há avaliações