Você também pode gostar

- NVRDocumento125 páginasNVRJohn Aldridge Chew100% (1)

- Munger's Analysis To Build A Trillion Dollar Business From ScratchDocumento11 páginasMunger's Analysis To Build A Trillion Dollar Business From ScratchJohn Aldridge Chew100% (4)

- Greenwald 2005 IP Gabelli in LondonDocumento40 páginasGreenwald 2005 IP Gabelli in LondonJohn Aldridge Chew100% (1)

- Cash Return on Capital Invested: Ten Years of Investment Analysis with the CROCI Economic Profit ModelNo EverandCash Return on Capital Invested: Ten Years of Investment Analysis with the CROCI Economic Profit ModelNota: 5 de 5 estrelas5/5 (3)

- Capital Returns: Investing Through the Capital Cycle: A Money Manager’s Reports 2002-15No EverandCapital Returns: Investing Through the Capital Cycle: A Money Manager’s Reports 2002-15Edward ChancellorNota: 4.5 de 5 estrelas4.5/5 (3)

- ATLAS HONDA Internship ReportDocumento83 páginasATLAS HONDA Internship ReportAhmed Aitsam93% (14)

- SGDE Example of A Clear Investment ThesisDocumento10 páginasSGDE Example of A Clear Investment ThesisJohn Aldridge ChewAinda não há avaliações

- Lecture 10 Moody's Corporation ExampleDocumento13 páginasLecture 10 Moody's Corporation ExampleJohn Aldridge ChewAinda não há avaliações

- Greenwald Class Notes 6 - Sealed Air Case StudyDocumento10 páginasGreenwald Class Notes 6 - Sealed Air Case StudyJohn Aldridge Chew100% (1)

- Global Crossing 1999 10-KDocumento199 páginasGlobal Crossing 1999 10-KJohn Aldridge Chew100% (1)

- Case Study 4 Clear Investment Thesis Winmill - Cash BargainDocumento69 páginasCase Study 4 Clear Investment Thesis Winmill - Cash BargainJohn Aldridge Chew100% (1)

- Lecture 6 An Investor Speaks of Investing in A Dying IndustryDocumento28 páginasLecture 6 An Investor Speaks of Investing in A Dying IndustryJohn Aldridge Chew100% (1)

- LPX 10K 2010 - Balance Sheet Case-StudyDocumento116 páginasLPX 10K 2010 - Balance Sheet Case-StudyJohn Aldridge ChewAinda não há avaliações

- Ghazi ValueInvestingCongress 100112Documento70 páginasGhazi ValueInvestingCongress 100112VALUEWALK LLC100% (1)

- Eminence CapitalMen's WarehouseDocumento0 páginaEminence CapitalMen's WarehouseCanadianValueAinda não há avaliações

- Hudsongeneralco10k405 1997Documento149 páginasHudsongeneralco10k405 1997John Aldridge ChewAinda não há avaliações

- Ek VLDocumento1 páginaEk VLJohn Aldridge ChewAinda não há avaliações

- Special Situation Net - Nets and Asset Based Investing by Ben Graham and OthersDocumento28 páginasSpecial Situation Net - Nets and Asset Based Investing by Ben Graham and OthersJohn Aldridge Chew100% (4)

- Distressed Investment Banking - To the Abyss and Back - Second EditionNo EverandDistressed Investment Banking - To the Abyss and Back - Second EditionAinda não há avaliações

- A Thorough Discussion of MCX - Case Study and Capital TheoryDocumento38 páginasA Thorough Discussion of MCX - Case Study and Capital TheoryJohn Aldridge Chew100% (2)

- Economies of Scale StudiesDocumento27 páginasEconomies of Scale StudiesJohn Aldridge Chew100% (4)

- Global Crossing 1999 10-KDocumento199 páginasGlobal Crossing 1999 10-KJohn Aldridge Chew100% (1)

- WMT Case Study #1 AnalysisDocumento8 páginasWMT Case Study #1 AnalysisJohn Aldridge Chew100% (1)

- Special Situation Net - Nets and Asset Based Investing by Ben Graham and OthersDocumento28 páginasSpecial Situation Net - Nets and Asset Based Investing by Ben Graham and OthersJohn Aldridge Chew100% (4)

- Case Study 4 Clear Investment Thesis Winmill - Cash BargainDocumento69 páginasCase Study 4 Clear Investment Thesis Winmill - Cash BargainJohn Aldridge Chew100% (1)

- Greenwald Class Notes 6 - Sealed Air Case StudyDocumento10 páginasGreenwald Class Notes 6 - Sealed Air Case StudyJohn Aldridge Chew100% (1)

- SQL Datetime Conversion - String Date Convert Formats - SQLUSA PDFDocumento13 páginasSQL Datetime Conversion - String Date Convert Formats - SQLUSA PDFRaul E CardozoAinda não há avaliações

- Outperform with Expectations-Based Management: A State-of-the-Art Approach to Creating and Enhancing Shareholder ValueNo EverandOutperform with Expectations-Based Management: A State-of-the-Art Approach to Creating and Enhancing Shareholder ValueAinda não há avaliações

- Sees Candy SchroederDocumento15 páginasSees Candy SchroederJohn Aldridge ChewAinda não há avaliações

- Buffett On ValuationDocumento7 páginasBuffett On ValuationAyush AggarwalAinda não há avaliações

- Sealed Air Case Study - HandoutDocumento17 páginasSealed Air Case Study - HandoutJohn Aldridge ChewAinda não há avaliações

- Students Grilled On Their Presentations and Review of CourseDocumento43 páginasStudents Grilled On Their Presentations and Review of CourseJohn Aldridge ChewAinda não há avaliações

- Nick Train The King of Buy and HoldDocumento13 páginasNick Train The King of Buy and HoldkessbrokerAinda não há avaliações

- Tobacco Stocks Buffett and BeyondDocumento5 páginasTobacco Stocks Buffett and BeyondJohn Aldridge ChewAinda não há avaliações

- Valuing Growth Managing RiskDocumento35 páginasValuing Growth Managing RiskJohn Aldridge Chew67% (3)

- Cornell Students Research Story On Enron 1998Documento4 páginasCornell Students Research Story On Enron 1998John Aldridge Chew100% (1)

- Bob Robotti - Navigating Deep WatersDocumento35 páginasBob Robotti - Navigating Deep WatersCanadianValue100% (1)

- WalMart Competitive Analysis Post 1985 - EOSDocumento3 páginasWalMart Competitive Analysis Post 1985 - EOSJohn Aldridge ChewAinda não há avaliações

- VII332Documento21 páginasVII332currygoatAinda não há avaliações

- Case Study - So What Is It WorthDocumento7 páginasCase Study - So What Is It WorthJohn Aldridge Chew100% (1)

- Warren Buffett and GEICO Case StudyDocumento18 páginasWarren Buffett and GEICO Case StudyReymond Jude PagcoAinda não há avaliações

- SNPK FinancialsDocumento123 páginasSNPK FinancialsJohn Aldridge Chew100% (1)

- Coors Case StudyDocumento3 páginasCoors Case StudyJohn Aldridge Chew0% (1)

- Dividend Policy, Strategy and Analysis - Value VaultDocumento67 páginasDividend Policy, Strategy and Analysis - Value VaultJohn Aldridge ChewAinda não há avaliações

- UPDATED AUG 2010 A Study of Market History Through Graham and Buffett and OthersDocumento83 páginasUPDATED AUG 2010 A Study of Market History Through Graham and Buffett and OthersJohn Aldridge Chew100% (1)

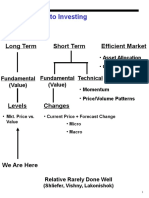

- Approaches To Investing: Long Term Short Term Efficient MarketDocumento71 páginasApproaches To Investing: Long Term Short Term Efficient MarketPeter WarmeAinda não há avaliações

- Murray Stahl - Value - Investor - May - 2013 PDFDocumento10 páginasMurray Stahl - Value - Investor - May - 2013 PDFkdwcapitalAinda não há avaliações

- Boyar's Intrinsic Value Research Forgotten FourtyDocumento49 páginasBoyar's Intrinsic Value Research Forgotten FourtyValueWalk100% (1)

- Office Hours With Warren Buffett May 2013Documento11 páginasOffice Hours With Warren Buffett May 2013jkusnan3341Ainda não há avaliações

- WalMart Competitive Analysis Post 1985 - EOSDocumento3 páginasWalMart Competitive Analysis Post 1985 - EOSJohn Aldridge ChewAinda não há avaliações

- Greenwald 2005 Inv Process Pres GabelliDocumento40 páginasGreenwald 2005 Inv Process Pres GabelliJohn Aldridge ChewAinda não há avaliações

- Wet Seal - VLDocumento1 páginaWet Seal - VLJohn Aldridge ChewAinda não há avaliações

- Class Notes #2 Intro and Duff and Phelps Case StudyDocumento27 páginasClass Notes #2 Intro and Duff and Phelps Case StudyJohn Aldridge Chew100% (1)

- The 400% Man: How A College Dropout at A Tiny Utah Fund Beat Wall Street, and Why Most Managers Are Scared To Copy HimDocumento5 páginasThe 400% Man: How A College Dropout at A Tiny Utah Fund Beat Wall Street, and Why Most Managers Are Scared To Copy Himrakeshmoney99Ainda não há avaliações

- Joe Koster's 2007 and 2009 Interviews With Peter BevelinDocumento12 páginasJoe Koster's 2007 and 2009 Interviews With Peter Bevelinjberkshire01Ainda não há avaliações

- Great Investor 2006 Lecture On Investment Philosophy and ProcessDocumento25 páginasGreat Investor 2006 Lecture On Investment Philosophy and ProcessJohn Aldridge Chew100% (1)

- Value Investing With Legends (Santos, Greenwald, Eveillard) SP2015Documento6 páginasValue Investing With Legends (Santos, Greenwald, Eveillard) SP2015ascentcommerce100% (1)

- Class 1 Introduction To Value InvestingDocumento36 páginasClass 1 Introduction To Value Investingoo2011Ainda não há avaliações

- Greenwald Class Notes 5 - Liz Claiborne & Valuing GrowthDocumento17 páginasGreenwald Class Notes 5 - Liz Claiborne & Valuing GrowthJohn Aldridge Chew100% (2)

- Anf VLDocumento1 páginaAnf VLJohn Aldridge ChewAinda não há avaliações

- Dangers of DCF MortierDocumento12 páginasDangers of DCF MortierKitti WongtuntakornAinda não há avaliações

- Death, Taxes and Reversion To The Mean - ROIC StudyDocumento20 páginasDeath, Taxes and Reversion To The Mean - ROIC Studypjs15Ainda não há avaliações

- Leon Cooperman Value Investing Congress Henry Singleton PDFDocumento37 páginasLeon Cooperman Value Investing Congress Henry Singleton PDFYashAinda não há avaliações

- David Tepper S 2007 Presentation at Carnegie Mellon PDFDocumento7 páginasDavid Tepper S 2007 Presentation at Carnegie Mellon PDFPattyPattersonAinda não há avaliações

- The Art of Vulture Investing: Adventures in Distressed Securities ManagementNo EverandThe Art of Vulture Investing: Adventures in Distressed Securities ManagementAinda não há avaliações

- Behind the Curve: An Analysis of the Investment Behavior of Private Equity FundsNo EverandBehind the Curve: An Analysis of the Investment Behavior of Private Equity FundsAinda não há avaliações

- Tech Stock Valuation: Investor Psychology and Economic AnalysisNo EverandTech Stock Valuation: Investor Psychology and Economic AnalysisNota: 4 de 5 estrelas4/5 (1)

- Financial Fine Print: Uncovering a Company's True ValueNo EverandFinancial Fine Print: Uncovering a Company's True ValueNota: 3 de 5 estrelas3/5 (3)

- Asian Financial Statement Analysis: Detecting Financial IrregularitiesNo EverandAsian Financial Statement Analysis: Detecting Financial IrregularitiesAinda não há avaliações

- SNPK FinancialsDocumento123 páginasSNPK FinancialsJohn Aldridge Chew100% (1)

- Tow Times Miller IndustriesDocumento32 páginasTow Times Miller IndustriesJohn Aldridge ChewAinda não há avaliações

- Chapter 20 - Margin of Safety Concept and More NotesDocumento53 páginasChapter 20 - Margin of Safety Concept and More NotesJohn Aldridge Chew100% (1)

- Assessing Performance Records - A Case Study 02-15-12Documento8 páginasAssessing Performance Records - A Case Study 02-15-12John Aldridge Chew0% (1)

- Niederhoffer Discusses Being WrongDocumento7 páginasNiederhoffer Discusses Being WrongJohn Aldridge Chew100% (1)

- CA Network Economics MauboussinDocumento16 páginasCA Network Economics MauboussinJohn Aldridge ChewAinda não há avaliações

- Coors Case StudyDocumento3 páginasCoors Case StudyJohn Aldridge Chew0% (1)

- Economies of Scale StudiesDocumento27 páginasEconomies of Scale StudiesJohn Aldridge ChewAinda não há avaliações

- WalMart Competitive Analysis Post 1985 - EOSDocumento3 páginasWalMart Competitive Analysis Post 1985 - EOSJohn Aldridge ChewAinda não há avaliações

- WalMart Competitive Analysis Post 1985 - EOSDocumento3 páginasWalMart Competitive Analysis Post 1985 - EOSJohn Aldridge ChewAinda não há avaliações

- Prof. Greenwald On StrategyDocumento6 páginasProf. Greenwald On StrategyMarc F. DemshockAinda não há avaliações

- GLBC 20000317 10K 19991231Documento333 páginasGLBC 20000317 10K 19991231John Aldridge ChewAinda não há avaliações

- Five Forces Industry AnalysisDocumento23 páginasFive Forces Industry AnalysisJohn Aldridge ChewAinda não há avaliações

- Quinsa Example of A Clear Investment Thesis - Case Study 3Documento18 páginasQuinsa Example of A Clear Investment Thesis - Case Study 3John Aldridge ChewAinda não há avaliações

- Tobacco Stocks Buffett and BeyondDocumento5 páginasTobacco Stocks Buffett and BeyondJohn Aldridge ChewAinda não há avaliações

- Burry WriteupsDocumento15 páginasBurry WriteupseclecticvalueAinda não há avaliações

- Capital Structure and Stock Repurchases - Value VaultDocumento58 páginasCapital Structure and Stock Repurchases - Value VaultJohn Aldridge ChewAinda não há avaliações

- Charlie Munger - Art of Stock PickingDocumento18 páginasCharlie Munger - Art of Stock PickingsuniltmAinda não há avaliações

- Dividend Policy, Strategy and Analysis - Value VaultDocumento67 páginasDividend Policy, Strategy and Analysis - Value VaultJohn Aldridge ChewAinda não há avaliações

- Revit 2019 Collaboration ToolsDocumento80 páginasRevit 2019 Collaboration ToolsNoureddineAinda não há avaliações

- C Sharp Logical TestDocumento6 páginasC Sharp Logical TestBogor0251Ainda não há avaliações

- Small Signal Analysis Section 5 6Documento104 páginasSmall Signal Analysis Section 5 6fayazAinda não há avaliações

- Ticket Udupi To MumbaiDocumento2 páginasTicket Udupi To MumbaikittushuklaAinda não há avaliações

- Lec # 26 NustDocumento18 páginasLec # 26 NustFor CheggAinda não há avaliações

- Palm Manual EngDocumento151 páginasPalm Manual EngwaterloveAinda não há avaliações

- AutoCAD Dinamicki Blokovi Tutorijal PDFDocumento18 páginasAutoCAD Dinamicki Blokovi Tutorijal PDFMilan JovicicAinda não há avaliações

- Milestone 9 For WebsiteDocumento17 páginasMilestone 9 For Websiteapi-238992918Ainda não há avaliações

- ABB Price Book 524Documento1 páginaABB Price Book 524EliasAinda não há avaliações

- Beam Deflection by Double Integration MethodDocumento21 páginasBeam Deflection by Double Integration MethodDanielle Ruthie GalitAinda não há avaliações

- Principles of SOADocumento36 páginasPrinciples of SOANgoc LeAinda não há avaliações

- Practical GAD (1-32) Roll No.20IF227Documento97 páginasPractical GAD (1-32) Roll No.20IF22720IF135 Anant PatilAinda não há avaliações

- Ethercombing Independent Security EvaluatorsDocumento12 páginasEthercombing Independent Security EvaluatorsangelAinda não há avaliações

- Paul Milgran - A Taxonomy of Mixed Reality Visual DisplaysDocumento11 páginasPaul Milgran - A Taxonomy of Mixed Reality Visual DisplaysPresencaVirtual100% (1)

- A Comparison of Pharmaceutical Promotional Tactics Between HK & ChinaDocumento10 páginasA Comparison of Pharmaceutical Promotional Tactics Between HK & ChinaAlfred LeungAinda não há avaliações

- Gravity Based Foundations For Offshore Wind FarmsDocumento121 páginasGravity Based Foundations For Offshore Wind FarmsBent1988Ainda não há avaliações

- ReviewerDocumento2 páginasReviewerAra Mae Pandez HugoAinda não há avaliações

- MCS Valve: Minimizes Body Washout Problems and Provides Reliable Low-Pressure SealingDocumento4 páginasMCS Valve: Minimizes Body Washout Problems and Provides Reliable Low-Pressure SealingTerry SmithAinda não há avaliações

- KrauseDocumento3 páginasKrauseVasile CuprianAinda não há avaliações

- Product Manual: Panel Mounted ControllerDocumento271 páginasProduct Manual: Panel Mounted ControllerLEONARDO FREITAS COSTAAinda não há avaliações

- Preventing OOS DeficienciesDocumento65 páginasPreventing OOS Deficienciesnsk79in@gmail.comAinda não há avaliações

- The "Solid Mount": Installation InstructionsDocumento1 páginaThe "Solid Mount": Installation InstructionsCraig MathenyAinda não há avaliações

- CEA 4.0 2022 - Current Draft AgendaDocumento10 páginasCEA 4.0 2022 - Current Draft AgendaThi TranAinda não há avaliações

- Health Informatics SDocumento4 páginasHealth Informatics SnourhanAinda não há avaliações

- AkDocumento7 páginasAkDavid BakcyumAinda não há avaliações

- Concrete For Water StructureDocumento22 páginasConcrete For Water StructureIntan MadiaaAinda não há avaliações

- IOSA Information BrochureDocumento14 páginasIOSA Information BrochureHavva SahınAinda não há avaliações

- Pro Tools ShortcutsDocumento5 páginasPro Tools ShortcutsSteveJones100% (1)