Você também pode gostar

- Executive Summary: Covering The Low-Income, Uninsured in Oklahoma: Recommendations For A Medicaid Demonstration ProposalDocumento5 páginasExecutive Summary: Covering The Low-Income, Uninsured in Oklahoma: Recommendations For A Medicaid Demonstration ProposalOK-SAFE, Inc.Ainda não há avaliações

- Meaningful Use: Implications For Adoption of Health Information Technology (HIT) Tamela D. Yount HAIN 670 10/17/2010Documento10 páginasMeaningful Use: Implications For Adoption of Health Information Technology (HIT) Tamela D. Yount HAIN 670 10/17/2010Tammy Yount Di PoppanteAinda não há avaliações

- Final Report For Colorado Public Option - Includes Appendices I - IVDocumento101 páginasFinal Report For Colorado Public Option - Includes Appendices I - IVapi-491077033Ainda não há avaliações

- Focus: Health ReformDocumento7 páginasFocus: Health ReformBrian ShawAinda não há avaliações

- Transforming The Health Care Marketplace by Promoting Value PDFDocumento7 páginasTransforming The Health Care Marketplace by Promoting Value PDFiggybauAinda não há avaliações

- 1.evolution of Heath PlansDocumento9 páginas1.evolution of Heath PlansUtpal Kumar PalAinda não há avaliações

- AHM 250 Course MaterialDocumento285 páginasAHM 250 Course MaterialAnitha Viji73% (15)

- State Health Exchanges and Qualified Health PlansDocumento49 páginasState Health Exchanges and Qualified Health PlansRajiv GargAinda não há avaliações

- StateProgramsUnderReform BriefDocumento8 páginasStateProgramsUnderReform Briefkirs0069Ainda não há avaliações

- Ensuring Benefits Parity and Gender Identity Nondiscrimination in Essential Health BenefitsDocumento13 páginasEnsuring Benefits Parity and Gender Identity Nondiscrimination in Essential Health BenefitsCenter for American ProgressAinda não há avaliações

- Medicare Policy: The Independent Payment Advisory Board: A New Approach To Controlling Medicare SpendingDocumento24 páginasMedicare Policy: The Independent Payment Advisory Board: A New Approach To Controlling Medicare SpendingCatherine SnowAinda não há avaliações

- AHM 250 Chapter 1Documento9 páginasAHM 250 Chapter 1Paromita MukhopadhyayAinda não há avaliações

- AHA BundledPayment ReportDocumento20 páginasAHA BundledPayment Reportbikram2128100% (1)

- PPP Task Force Report-DraftDocumento41 páginasPPP Task Force Report-DraftSudhir SinghAinda não há avaliações

- APM Companion Paper Formatted FINALDocumento11 páginasAPM Companion Paper Formatted FINALAnonymous 2zbzrvAinda não há avaliações

- C. Mjaset - Value-Based Health Care in Four Different Health Care SystemsDocumento23 páginasC. Mjaset - Value-Based Health Care in Four Different Health Care SystemsRodney RosaliaAinda não há avaliações

- 05 - Main Report HIB FinalDocumento39 páginas05 - Main Report HIB FinalShurendra GhimireAinda não há avaliações

- Managed Care NPRM 09 2015Documento3 páginasManaged Care NPRM 09 2015api-293754603Ainda não há avaliações

- Ramos, Sioco Chapter 25 and 26Documento59 páginasRamos, Sioco Chapter 25 and 26DOROTHY ANN SOMBILUNAAinda não há avaliações

- Oh P Delivery SystemDocumento14 páginasOh P Delivery SystemfrendirachmadAinda não há avaliações

- StateProgramsReform REPORTDocumento59 páginasStateProgramsReform REPORTkirs0069Ainda não há avaliações

- Healthcare Inc. A Better Business ModelDocumento13 páginasHealthcare Inc. A Better Business ModelrangababAinda não há avaliações

- News & Notes: Psychiatric Services 66:7, July 2015Documento2 páginasNews & Notes: Psychiatric Services 66:7, July 2015Re LzAinda não há avaliações

- The Social Life of Health Insurance in Low - To Middle-Income Countries: An Anthropological Research AgendaDocumento22 páginasThe Social Life of Health Insurance in Low - To Middle-Income Countries: An Anthropological Research AgendaDeborah FrommAinda não há avaliações

- Federal Register / Vol. 63, No. 35 / Monday, February 23, 1998 / NoticesDocumento12 páginasFederal Register / Vol. 63, No. 35 / Monday, February 23, 1998 / NoticesGudegna GemechuAinda não há avaliações

- Equality Analysis: Healthy Lives, Healthy People (2:9)Documento49 páginasEquality Analysis: Healthy Lives, Healthy People (2:9)KawaduhokiAinda não há avaliações

- Khyber Pakhtunkhwa Health Sector Review: Hospital CareNo EverandKhyber Pakhtunkhwa Health Sector Review: Hospital CareAinda não há avaliações

- NYS DOB - Health Dept Budget 2018 HightlightsDocumento13 páginasNYS DOB - Health Dept Budget 2018 Hightlightssrikrishna natesanAinda não há avaliações

- Clinical Audit Manual July, 2016Documento21 páginasClinical Audit Manual July, 2016Addishiwot seifuAinda não há avaliações

- SHADAC Brief30 OnlineDocumento10 páginasSHADAC Brief30 Onlinekirs0069Ainda não há avaliações

- Issue Brief 23Documento12 páginasIssue Brief 23SHADACAinda não há avaliações

- ACA Health Reform and Mental Health Care 2012Documento3 páginasACA Health Reform and Mental Health Care 2012Mike F MartelliAinda não há avaliações

- The Affordable Care ActDocumento7 páginasThe Affordable Care ActalexAinda não há avaliações

- A Critical Insight, Analysis and Comparative of Health Care Provision in The United Kingdom and United States of America.Documento19 páginasA Critical Insight, Analysis and Comparative of Health Care Provision in The United Kingdom and United States of America.Abiola AbrahamAinda não há avaliações

- UK AND US HEALTHCARE COMPARISON - EditedDocumento19 páginasUK AND US HEALTHCARE COMPARISON - EditedAbiola Abraham100% (1)

- 201720180SB562 - Senate HealthDocumento20 páginas201720180SB562 - Senate HealthMaggie DeSistoAinda não há avaliações

- EHIADocumento6 páginasEHIAmuhammedseid2946Ainda não há avaliações

- (MOHW) The Eighth Public Engagement RoundtableDocumento4 páginas(MOHW) The Eighth Public Engagement Roundtableinkorea202425Ainda não há avaliações

- Jost - Timothy Jost, State-Run Programs Are Not A Viable Option For Creating A Public PlanDocumento7 páginasJost - Timothy Jost, State-Run Programs Are Not A Viable Option For Creating A Public PlanjoshblackmanAinda não há avaliações

- OIG Compliance Program For Third-Party Medical Billing CompaniesDocumento15 páginasOIG Compliance Program For Third-Party Medical Billing CompaniesaaronborosAinda não há avaliações

- Public Private Partnerships Booket-2018Documento44 páginasPublic Private Partnerships Booket-2018Prabir Kumar ChatterjeeAinda não há avaliações

- PPP Task Force Report DraftDocumento48 páginasPPP Task Force Report DraftSavita HanamsagarAinda não há avaliações

- CPRNYDE Response To The 2012 DOH Report - April 5 2013Documento31 páginasCPRNYDE Response To The 2012 DOH Report - April 5 2013EdmondsonAinda não há avaliações

- Availability and Use of Enrollment Data From The ACA Health Insurance MarketplaceDocumento23 páginasAvailability and Use of Enrollment Data From The ACA Health Insurance Marketplacekirs0069Ainda não há avaliações

- Policy Issues and Access Cost and QualityDocumento6 páginasPolicy Issues and Access Cost and Qualityapi-240946281Ainda não há avaliações

- The HMO Act of 1973 Health Maintenance Organization Act of 1973Documento3 páginasThe HMO Act of 1973 Health Maintenance Organization Act of 1973Sai PrabhuAinda não há avaliações

- My Two Cents: Taking the Care Out of Health CareNo EverandMy Two Cents: Taking the Care Out of Health CareAinda não há avaliações

- ACO Final ReportDocumento24 páginasACO Final ReportSowmya ParthasarathyAinda não há avaliações

- Paper 6Documento3 páginasPaper 6api-301357653Ainda não há avaliações

- Dear Governor Feb 24Documento3 páginasDear Governor Feb 24KFFHealthNewsAinda não há avaliações

- Legal and Policy Requirements of Basic Health Insurance Package To Achieve Universal Health Coverage in A Developing CountryDocumento7 páginasLegal and Policy Requirements of Basic Health Insurance Package To Achieve Universal Health Coverage in A Developing CountryBahtiar AfandiAinda não há avaliações

- Questions & Answers - Updated April 12, 2011Documento5 páginasQuestions & Answers - Updated April 12, 2011Denilson Oliveira MeloAinda não há avaliações

- Solution Manual For Health Care Management and The Law Principles and Applications 1st EditionDocumento37 páginasSolution Manual For Health Care Management and The Law Principles and Applications 1st Editioneozoicjaggern2ni4100% (13)

- A Sustainable Health System IIDocumento73 páginasA Sustainable Health System IICírculo de EmpresariosAinda não há avaliações

- A New Definition' For Health Care Reform: James C. Capretta Tom MillerDocumento57 páginasA New Definition' For Health Care Reform: James C. Capretta Tom MillerFirhiwot DemisseAinda não há avaliações

- StateDataSpotlight ME May2011Documento3 páginasStateDataSpotlight ME May2011SHADACAinda não há avaliações

- SHARE Grantee Newsletter October 2009Documento4 páginasSHARE Grantee Newsletter October 2009butle180Ainda não há avaliações

- Policy Memo 1 1Documento6 páginasPolicy Memo 1 1api-488942224Ainda não há avaliações

- Mining for Gold In a Barren Land: Pioneer Accountable Care Organization Potential to Redesign the Healthcare Business Model in a Post-Acute SettingNo EverandMining for Gold In a Barren Land: Pioneer Accountable Care Organization Potential to Redesign the Healthcare Business Model in a Post-Acute SettingAinda não há avaliações

- Medicare Revolution: Profiting from Quality, Not QuantityNo EverandMedicare Revolution: Profiting from Quality, Not QuantityAinda não há avaliações

- Customer Relationship Management Project ReportDocumento102 páginasCustomer Relationship Management Project ReportJAI SINGHAinda não há avaliações

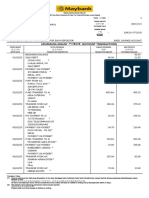

- Statements 5013Documento6 páginasStatements 5013ytprem agu100% (1)

- HSBC Personal Internet Banking Inter-Bank Fund Transfer (BEFTN) Frequently Asked QuestionDocumento6 páginasHSBC Personal Internet Banking Inter-Bank Fund Transfer (BEFTN) Frequently Asked Questionrokib0116Ainda não há avaliações

- Gift Cards Method - JUNE 2023Documento9 páginasGift Cards Method - JUNE 2023Neel KakkadAinda não há avaliações

- Flight Ticket - Bangalore To Lucknow: Passenger's Name Status Seat No. 1. Miss Juhi Awasthi ConfirmedDocumento3 páginasFlight Ticket - Bangalore To Lucknow: Passenger's Name Status Seat No. 1. Miss Juhi Awasthi ConfirmedJuhi AwasthiAinda não há avaliações

- Statements: Sources of The Medical Myths and Quack PracticesDocumento6 páginasStatements: Sources of The Medical Myths and Quack PracticesLoreta De GuzmanAinda não há avaliações

- Mand CHODocumento7 páginasMand CHOMichael BaguyoAinda não há avaliações

- Dangila Branch CustomerDocumento2 páginasDangila Branch CustomerdagnayeAinda não há avaliações

- Amadeus PDFDocumento32 páginasAmadeus PDFsaurabhwmAinda não há avaliações

- Air Cap2702i C k9 DatasheetDocumento3 páginasAir Cap2702i C k9 DatasheettotAinda não há avaliações

- Benefit IllustrationDocumento3 páginasBenefit Illustrationanon_315406837Ainda não há avaliações

- 30000/30000I PC Terminal Gonsin Software Manual of Scan Environment FrequencyDocumento2 páginas30000/30000I PC Terminal Gonsin Software Manual of Scan Environment Frequencyemanuel romeroAinda não há avaliações

- Non Performing AssetsDocumento15 páginasNon Performing AssetsChetanModiAinda não há avaliações

- BORANG AMLA - Lampiran II - Borang Transaksi Mencurigakan Detail AML CFT - RMSDocumento8 páginasBORANG AMLA - Lampiran II - Borang Transaksi Mencurigakan Detail AML CFT - RMSAr-Rahnu X'change Sri ManjaAinda não há avaliações

- Problem SolutionDocumento3 páginasProblem SolutionMohammad Mnirul Islam sajibAinda não há avaliações

- Form No 03102014 ALIB Life Insurance BenefitsDocumento2 páginasForm No 03102014 ALIB Life Insurance BenefitsAndres Kalikasan SaraAinda não há avaliações

- Proforma InvoiceDocumento2 páginasProforma InvoicehrdbelibisgroupAinda não há avaliações

- Mbs Mice BrochureDocumento14 páginasMbs Mice BrochureTrần KhươngAinda não há avaliações

- A Study On Customer SatisfactionDocumento14 páginasA Study On Customer Satisfactionakash ManwarAinda não há avaliações

- Questionnaire On Labour Welfare MeasuresDocumento3 páginasQuestionnaire On Labour Welfare MeasuresAfra Sayed100% (1)

- Ipoh Main 1 28/02/23Documento6 páginasIpoh Main 1 28/02/23Remy YamahaAinda não há avaliações

- Importance of Types of Networks - LAN, MAN, and WAN - SimplilearnDocumento9 páginasImportance of Types of Networks - LAN, MAN, and WAN - SimplilearnMike MikkelsenAinda não há avaliações

- JAIIB AFM Practice MCQs Part 1Documento17 páginasJAIIB AFM Practice MCQs Part 1preetmehtaAinda não há avaliações

- Bhuvanteza Happy Homes Hmda Fee ReceiptsDocumento6 páginasBhuvanteza Happy Homes Hmda Fee ReceiptsMahesh KanthiAinda não há avaliações

- p58 Inland v3Documento2 páginasp58 Inland v3andrewmmwilmot0% (1)

- Raj Tour & Travels Reciept FormatDocumento2 páginasRaj Tour & Travels Reciept Formatnamanagrawal259053% (160)

- Business Data - Ma. Angela Bravo - New JerseyDocumento16 páginasBusiness Data - Ma. Angela Bravo - New JerseyAngela BravoAinda não há avaliações

- CLP Audit2Documento4 páginasCLP Audit2hannaniAinda não há avaliações

- Teori AkuntansiDocumento18 páginasTeori AkuntansiTria UlfaAinda não há avaliações

- 6-Data Link LayerDocumento6 páginas6-Data Link Layerbadri.mohammed55Ainda não há avaliações