Você também pode gostar

- Solutions-Debraj-Ray-1 Dev EcoDocumento62 páginasSolutions-Debraj-Ray-1 Dev EcoDiksha89% (9)

- Final Practical NAVTTCDocumento8 páginasFinal Practical NAVTTCParwaiz Ali JiskaniAinda não há avaliações

- Technical IndicatorsDocumento54 páginasTechnical IndicatorsRavee MishraAinda não há avaliações

- Assignment: Statistics For ManagementDocumento17 páginasAssignment: Statistics For ManagementShravanti Bhowmik SenAinda não há avaliações

- MB0041Documento8 páginasMB0041Gaurang VyasAinda não há avaliações

- MB0041-Fin & MGMT AccountingDocumento12 páginasMB0041-Fin & MGMT AccountingRamesh SoniAinda não há avaliações

- MB0041 Financial and Management AccountingDocumento12 páginasMB0041 Financial and Management AccountingDivyang Panchasara0% (2)

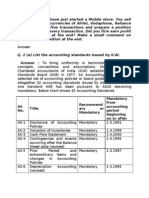

- Recommend Ary or Mandatory Mandatory From Accounting Period Beginning On or AfterDocumento7 páginasRecommend Ary or Mandatory Mandatory From Accounting Period Beginning On or AfterdnbiswasAinda não há avaliações

- Q.1 Assure You Have Just Started A Mobile Store. You Sell MobileDocumento16 páginasQ.1 Assure You Have Just Started A Mobile Store. You Sell MobileUttam SinghAinda não há avaliações

- Documents - CAAH2013 - MBA 2 Acc Dec Making Workbook Jan 2013 PDFDocumento96 páginasDocuments - CAAH2013 - MBA 2 Acc Dec Making Workbook Jan 2013 PDFSatyabrataNayak100% (1)

- NBP Internship Report by Umer RashidDocumento75 páginasNBP Internship Report by Umer RashidKT LHR 2Ainda não há avaliações

- 3-5 MCQ - DikshaDocumento2 páginas3-5 MCQ - DikshabenAinda não há avaliações

- Chapter Zakat Acc For Ibis-1 - 42051Documento20 páginasChapter Zakat Acc For Ibis-1 - 42051Aisyah AnuarAinda não há avaliações

- IMT-61 (Corporate Finance) Need Solution - Ur Call Away - 9582940966Documento5 páginasIMT-61 (Corporate Finance) Need Solution - Ur Call Away - 9582940966Ambrish (gYpr.in)Ainda não há avaliações

- Sample PaperDocumento28 páginasSample PaperSantanu KararAinda não há avaliações

- Capinew Account June13Documento7 páginasCapinew Account June13ashwinAinda não há avaliações

- Mba025 Set1 Set2 520929319Documento16 páginasMba025 Set1 Set2 520929319tejas2111Ainda não há avaliações

- MBA Semester 1 Spring 2015 Solved Assignments - MB0041Documento3 páginasMBA Semester 1 Spring 2015 Solved Assignments - MB0041SolvedSmuAssignmentsAinda não há avaliações

- Accounting For Managers MB003 QuestionDocumento34 páginasAccounting For Managers MB003 QuestionAiDLo0% (1)

- LeonsDocumento34 páginasLeonsFeilix BennyAinda não há avaliações

- Ratio Analysis Numerical QuestionsDocumento9 páginasRatio Analysis Numerical Questionsnsrivastav1Ainda não há avaliações

- MBA 8 Year 2 Accounting For Decision Making Workbook January 2020Documento94 páginasMBA 8 Year 2 Accounting For Decision Making Workbook January 2020weedforlifeAinda não há avaliações

- Master of Business Administration - Semister - 1 Mb0041 - Fianncial Management Accounting SET - 2Documento10 páginasMaster of Business Administration - Semister - 1 Mb0041 - Fianncial Management Accounting SET - 2Asha JyothiAinda não há avaliações

- Accounts Question BankDocumento12 páginasAccounts Question BankSRMBALAAAinda não há avaliações

- Cherat-Cement-Company Final Report 2Documento21 páginasCherat-Cement-Company Final Report 2UbaidAinda não há avaliações

- Swagat 2010 2011 Training BookletDocumento108 páginasSwagat 2010 2011 Training Bookletbitus92Ainda não há avaliações

- References BitCoinDocumento27 páginasReferences BitCoinVeerAinda não há avaliações

- Financial Accounting (Unsolved Papers of ICMAP)Documento48 páginasFinancial Accounting (Unsolved Papers of ICMAP)Platonic0% (1)

- Individual Assignment: Analysis of Audit Reports of Premier Bank LimitedDocumento7 páginasIndividual Assignment: Analysis of Audit Reports of Premier Bank LimitedSohel MahmudAinda não há avaliações

- Assignment Front Sheet: BusinessDocumento13 páginasAssignment Front Sheet: BusinessHassan AsgharAinda não há avaliações

- Consumer LoansDocumento28 páginasConsumer LoansSyed AliAinda não há avaliações

- Bba Banking Fin1Documento10 páginasBba Banking Fin1kotit35Ainda não há avaliações

- MB41Documento5 páginasMB41Prajeesh Kumar KmAinda não há avaliações

- Financial Accounting I SemesterDocumento25 páginasFinancial Accounting I SemesterBhaskar KrishnappaAinda não há avaliações

- Project of MCBDocumento55 páginasProject of MCBSana JavaidAinda não há avaliações

- PPTDocumento35 páginasPPTShivam ChauhanAinda não há avaliações

- Account Project OrginalDocumento41 páginasAccount Project OrginalshankarinadarAinda não há avaliações

- UBL ReportDocumento65 páginasUBL ReportNoman Iqbal100% (1)

- Allied Bank PresentationDocumento74 páginasAllied Bank Presentationtyrose88100% (3)

- Get Answers of Following Questions Here: MB0041 - Financial and Management AccountingDocumento3 páginasGet Answers of Following Questions Here: MB0041 - Financial and Management AccountingRajesh SinghAinda não há avaliações

- Insurance & BankingDocumento33 páginasInsurance & BankingbobbyhandsomeAinda não há avaliações

- Annual Report 2011Documento233 páginasAnnual Report 2011Khalid FirozAinda não há avaliações

- Topic 5 CFDocumento18 páginasTopic 5 CFAmalMdIsaAinda não há avaliações

- NBFC-L&T Finance: Group MembersDocumento29 páginasNBFC-L&T Finance: Group Membershayden28Ainda não há avaliações

- Balance Sheet Analysis Quick BookletDocumento16 páginasBalance Sheet Analysis Quick BookletSwatiRanjanAinda não há avaliações

- IMT 57 Financial Accounting M1Documento4 páginasIMT 57 Financial Accounting M1solvedcareAinda não há avaliações

- FA - Excercises & Answers PDFDocumento17 páginasFA - Excercises & Answers PDFRasanjaliGunasekeraAinda não há avaliações

- Advanced Auditing and Assurance - Revision KitDocumento244 páginasAdvanced Auditing and Assurance - Revision Kitmulika99Ainda não há avaliações

- Isc Accounts 5 MB: (Three HoursDocumento7 páginasIsc Accounts 5 MB: (Three HoursShivam SinghAinda não há avaliações

- Cash BudgetDocumento6 páginasCash BudgetSalahuddin ShahAinda não há avaliações

- Advanced AccountingDocumento13 páginasAdvanced AccountingprateekfreezerAinda não há avaliações

- Kotak Mahindra Bank Limited Swot Analysis BacDocumento8 páginasKotak Mahindra Bank Limited Swot Analysis BacAsh DesaiAinda não há avaliações

- Soneri Annual Report 2010Documento57 páginasSoneri Annual Report 2010Muqaddas IsrarAinda não há avaliações

- 11 CaipccaccountsDocumento19 páginas11 Caipccaccountsapi-206947225Ainda não há avaliações

- Capii Advaccount June13Documento14 páginasCapii Advaccount June13casarokarAinda não há avaliações

- Financial Results 201920Documento26 páginasFinancial Results 201920Ankush AgrawalAinda não há avaliações

- Financial Reporting and Auditing in Sovereign Operations: Technical Guidance NoteNo EverandFinancial Reporting and Auditing in Sovereign Operations: Technical Guidance NoteAinda não há avaliações

- Statement of Cash Flows: Preparation, Presentation, and UseNo EverandStatement of Cash Flows: Preparation, Presentation, and UseAinda não há avaliações

- Fast-Track Tax Reform: Lessons from the MaldivesNo EverandFast-Track Tax Reform: Lessons from the MaldivesAinda não há avaliações

- Business Financial Information Secrets: How a Business Produces and Utilizes Critical Financial InformationNo EverandBusiness Financial Information Secrets: How a Business Produces and Utilizes Critical Financial InformationAinda não há avaliações

- Chapter 05 Questions and ProblemsDocumento4 páginasChapter 05 Questions and Problemsglobinho111Ainda não há avaliações

- Ring Type JointsDocumento12 páginasRing Type JointsdamicesterAinda não há avaliações

- THREE Bonds and Stock Valuation.. STOCKDocumento19 páginasTHREE Bonds and Stock Valuation.. STOCKRaasu KuttyAinda não há avaliações

- Air Thread Case FinalDocumento49 páginasAir Thread Case FinalJonathan GranowitzAinda não há avaliações

- Bond PricingDocumento4 páginasBond PricingKyrbe Krystel AbalaAinda não há avaliações

- HDFC Life Insurance ProjectDocumento18 páginasHDFC Life Insurance Projectshubham moonAinda não há avaliações

- UGRD-ITE6301 Technopreneurship Midterm Quiz 2Documento15 páginasUGRD-ITE6301 Technopreneurship Midterm Quiz 2DanicaAinda não há avaliações

- Bernie Madoff - Overview, History, and The Ponzi SchemeDocumento7 páginasBernie Madoff - Overview, History, and The Ponzi SchemeElleAinda não há avaliações

- Drills Dissolution Admission of A PartnerDocumento4 páginasDrills Dissolution Admission of A PartnerSSGAinda não há avaliações

- Clinton Foundation Before NY StateDocumento99 páginasClinton Foundation Before NY StateDaily Caller News FoundationAinda não há avaliações

- Asian Paints Limited Dividend Distribution PolicyDocumento3 páginasAsian Paints Limited Dividend Distribution PolicyJaiAinda não há avaliações

- A STUDY ON DEPOSITORY SYSTEM - Docx NewDocumento19 páginasA STUDY ON DEPOSITORY SYSTEM - Docx NewRajni WaswaniAinda não há avaliações

- Fin405 Assignment 2 Group 7Documento18 páginasFin405 Assignment 2 Group 7Esraah AhmedAinda não há avaliações

- WEEK 2 - Chapter 2-An Overview of Financial SystemDocumento26 páginasWEEK 2 - Chapter 2-An Overview of Financial SystemSipanAinda não há avaliações

- DebentureDocumento34 páginasDebentureSOHEL BANGIAinda não há avaliações

- Asset Management ISO55Documento50 páginasAsset Management ISO55helix2010Ainda não há avaliações

- Study The Effect of Economic Growth On The Real Estate Industry in Major Cities of IndiaDocumento46 páginasStudy The Effect of Economic Growth On The Real Estate Industry in Major Cities of IndiamtamilvAinda não há avaliações

- Chater Two Leacture NoteDocumento26 páginasChater Two Leacture NoteMelaku WalelgneAinda não há avaliações

- Business GKDocumento21 páginasBusiness GKapi-19620791Ainda não há avaliações

- Hul PPT (CTP)Documento31 páginasHul PPT (CTP)vedantAinda não há avaliações

- Max's GroupDocumento29 páginasMax's GroupEnzy Crema100% (1)

- Ac557 W3 HW HBDocumento2 páginasAc557 W3 HW HBHasan Barakat100% (2)

- Economic Impact of Libraries in New York CityDocumento14 páginasEconomic Impact of Libraries in New York CityCity Limits (New York)Ainda não há avaliações

- Impact of Inflation On Economic Growth: A Survey of Literature ReviewDocumento13 páginasImpact of Inflation On Economic Growth: A Survey of Literature ReviewgayleAinda não há avaliações

- Capital BudgetingDocumento53 páginasCapital BudgetingSaahil LedwaniAinda não há avaliações

- Executive Summary: Human Resource Practices in Reliance InsuranceDocumento54 páginasExecutive Summary: Human Resource Practices in Reliance Insurancevenkata siva kumarAinda não há avaliações

- Risk Management ProposalDocumento13 páginasRisk Management ProposalromanAinda não há avaliações

- Accounting CONCEPTS Multiple Choice QuestionsDocumento7 páginasAccounting CONCEPTS Multiple Choice Questionspatsjit50% (2)