Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- For December 31 20x1 The Balance Sheet of Baxter Corporation Was As FollowsDocumento4 páginasFor December 31 20x1 The Balance Sheet of Baxter Corporation Was As Followslaale dijaanAinda não há avaliações

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Chapter 2 - Taxes, Tax Laws, and Tax AdministrationDocumento7 páginasChapter 2 - Taxes, Tax Laws, and Tax Administrationreymardico100% (2)

- Interim Statement 10-Mar-2023 12-25-49Documento2 páginasInterim Statement 10-Mar-2023 12-25-49zani arslanAinda não há avaliações

- Invoice ZoomDocumento4 páginasInvoice ZoomAsyifaImandaAinda não há avaliações

- DeductionsDocumento10 páginasDeductionsceline marasiganAinda não há avaliações

- ET Explains How The Exemption Against HRA Is Arrived atDocumento10 páginasET Explains How The Exemption Against HRA Is Arrived atbluckyAinda não há avaliações

- Ce Block NCF RC - 815 and RC-642 Haider Saleh Al-HaiderDocumento3 páginasCe Block NCF RC - 815 and RC-642 Haider Saleh Al-Haidersudeep karunAinda não há avaliações

- Purchase OrderDocumento1 páginaPurchase Orderksb sales teamAinda não há avaliações

- Aug2019Documento8 páginasAug2019Mahesh RajuAinda não há avaliações

- AADocumento11 páginasAAJames wiliamAinda não há avaliações

- Travel Claim - Appendix A, B Etc - DotolloDocumento6 páginasTravel Claim - Appendix A, B Etc - DotolloHanzelkris CubianAinda não há avaliações

- 1 Feb InvoiceDocumento2 páginas1 Feb InvoiceritikkuchhalphotoAinda não há avaliações

- Pay Roll SamDocumento2 páginasPay Roll Samsamuel debebeAinda não há avaliações

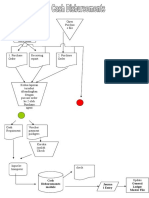

- Flowchart Account Payable & Cash DisbursementsDocumento4 páginasFlowchart Account Payable & Cash DisbursementsAlif Nur IrvanAinda não há avaliações

- Solved in 2002 Florence Purchased 30 Acres of Land She HasDocumento1 páginaSolved in 2002 Florence Purchased 30 Acres of Land She HasAnbu jaromiaAinda não há avaliações

- Canon Printer InvoiceDocumento2 páginasCanon Printer InvoiceTYCS35 SIDDHESH PENDURKARAinda não há avaliações

- Rejected Offline Mts 2014Documento79 páginasRejected Offline Mts 2014Tejas SamelAinda não há avaliações

- Tax Reforms in Pakistan Historic and Critical ViewDocumento299 páginasTax Reforms in Pakistan Historic and Critical ViewJąhąnząib Khąn KąkąrAinda não há avaliações

- BIR Ruling No. 051 2000 PDFDocumento3 páginasBIR Ruling No. 051 2000 PDFVina CeeAinda não há avaliações

- Arthakranti BTT Budget Proposal - Advertorial PDFDocumento1 páginaArthakranti BTT Budget Proposal - Advertorial PDFAryann GuptaAinda não há avaliações

- Monopoly Deed Cards PDFDocumento12 páginasMonopoly Deed Cards PDFErfanAinda não há avaliações

- Form16 W0000000 GS186523X 2021 20211Documento1 páginaForm16 W0000000 GS186523X 2021 20211Raman OjhaAinda não há avaliações

- GST Compensation CessDocumento2 páginasGST Compensation CessPalak JioAinda não há avaliações

- Investor Agreement PDFDocumento2 páginasInvestor Agreement PDFRam Kumar BasakAinda não há avaliações

- Salary-Slip FormatDocumento6 páginasSalary-Slip FormatArjunAtwal100% (1)

- Fee Circular 2023 24Documento1 páginaFee Circular 2023 24Archana SinghAinda não há avaliações

- Topic 14 - Income and Business TaxationDocumento71 páginasTopic 14 - Income and Business TaxationFrancez Anne Guanzon100% (1)

- Encasa BrochureDocumento12 páginasEncasa Brochuremanoj_dalalAinda não há avaliações

- Ninso Global SDN BHD: Official PayslipsDocumento1 páginaNinso Global SDN BHD: Official Payslipsahmad zakwanAinda não há avaliações

- Hotel Amar Residency: Tax InvoiceDocumento1 páginaHotel Amar Residency: Tax InvoiceAnkit SinghAinda não há avaliações