Você também pode gostar

- Financial Policy and PlanningDocumento16 páginasFinancial Policy and Planninggunaseelan_pnb7566Ainda não há avaliações

- Essential Capital Budgeting Techniques in 40 CharactersDocumento11 páginasEssential Capital Budgeting Techniques in 40 CharactersGaurav GurjarAinda não há avaliações

- Capital Budgeting Methods SummaryDocumento3 páginasCapital Budgeting Methods Summarykyra inarsolinAinda não há avaliações

- Techniques of Investment AnalysisDocumento32 páginasTechniques of Investment AnalysisPranjal Verma0% (1)

- Evaluation of Capital Budgeting TechniquesDocumento36 páginasEvaluation of Capital Budgeting TechniquesAshish GoelAinda não há avaliações

- Capital Bud ..Updated FinalDocumento36 páginasCapital Bud ..Updated FinalKeyur JoshiAinda não há avaliações

- Capital Budgeting TechniquesDocumento26 páginasCapital Budgeting TechniquesMahima GirdharAinda não há avaliações

- Capital BudgetingDocumento31 páginasCapital BudgetingJanu JinniAinda não há avaliações

- What Is Capital BudgetingDocumento24 páginasWhat Is Capital BudgetingZohaib Zohaib Khurshid AhmadAinda não há avaliações

- Dr. Sandeep Malu Associate Professor SVIM, IndoreDocumento14 páginasDr. Sandeep Malu Associate Professor SVIM, Indorechaterji_aAinda não há avaliações

- Dr. Sandeep Malu Associate Professor SVIM, IndoreDocumento14 páginasDr. Sandeep Malu Associate Professor SVIM, Indorechaterji_aAinda não há avaliações

- Capital Budgeting at Birla CementDocumento61 páginasCapital Budgeting at Birla Cementrpsinghsikarwar0% (1)

- Capital Budgeting Can Be Defined Finance EssayDocumento4 páginasCapital Budgeting Can Be Defined Finance EssayHND Assignment HelpAinda não há avaliações

- Capital Budgeting 1Documento19 páginasCapital Budgeting 1Lisie SonyAinda não há avaliações

- Capital Budgeting - NPV AnalysisDocumento17 páginasCapital Budgeting - NPV AnalysisFernandes RudolfAinda não há avaliações

- Capital Budgeting Techniques ExplainedDocumento28 páginasCapital Budgeting Techniques Explainedhashmi4a4Ainda não há avaliações

- Nature of Investment Decisions: Capital Budgeting, or Capital Expenditure DecisionsDocumento49 páginasNature of Investment Decisions: Capital Budgeting, or Capital Expenditure DecisionsRam Krishna Krish100% (2)

- Capital Budgeting 55Documento54 páginasCapital Budgeting 55Hitesh Jain0% (1)

- Capital Budgeting: Exclusive ProjectsDocumento6 páginasCapital Budgeting: Exclusive ProjectsMethon BaskAinda não há avaliações

- Why Capital Budgeting is Important for Long-Term Investment DecisionsDocumento17 páginasWhy Capital Budgeting is Important for Long-Term Investment DecisionsAditya SinghAinda não há avaliações

- Ch20 InvestmentAppraisalDocumento32 páginasCh20 InvestmentAppraisalsohail merchantAinda não há avaliações

- Discounting or Modern Methods of Capital BudgetingDocumento18 páginasDiscounting or Modern Methods of Capital BudgetingRiyas Parakkattil100% (1)

- Capitalbudgeting 1227282768304644 8Documento27 páginasCapitalbudgeting 1227282768304644 8Sumi LatheefAinda não há avaliações

- Investment Appraisal TechniquesDocumento6 páginasInvestment Appraisal TechniquesERICK MLINGWAAinda não há avaliações

- Capital Budgeting Methods ComparedDocumento95 páginasCapital Budgeting Methods ComparedMohammad Salim HossainAinda não há avaliações

- Year, Financial Management: Capital BudgetingDocumento9 páginasYear, Financial Management: Capital BudgetingPooja KansalAinda não há avaliações

- Capital Budgeing ReviewDocumento20 páginasCapital Budgeing ReviewBalakrishna ChakaliAinda não há avaliações

- DR - Naushad Alam: Capital BudgetingDocumento38 páginasDR - Naushad Alam: Capital BudgetingUrvashi SinghAinda não há avaliações

- Time Value of MoneyDocumento4 páginasTime Value of MoneyShradha KapseAinda não há avaliações

- Definition of Capital BudgetingDocumento6 páginasDefinition of Capital Budgetingkaram deenAinda não há avaliações

- Capital Budgeting Methods and Techniques GuideDocumento3 páginasCapital Budgeting Methods and Techniques Guidepratibha2031Ainda não há avaliações

- Capital Budgeting (Or Investment Appraisal) Is The Planning Process Used To Determine Whether A Firm'sDocumento4 páginasCapital Budgeting (Or Investment Appraisal) Is The Planning Process Used To Determine Whether A Firm'spavanbhatAinda não há avaliações

- Guide to Capital Budgeting DecisionsDocumento8 páginasGuide to Capital Budgeting DecisionsDawn CaldeiraAinda não há avaliações

- Captai Budgeting AssignmentDocumento2 páginasCaptai Budgeting AssignmentPravanjan AumcapAinda não há avaliações

- (Lecture 1 & 2) - Introduction To Investment Appraisal Methods 2Documento21 páginas(Lecture 1 & 2) - Introduction To Investment Appraisal Methods 2Ajay Kumar TakiarAinda não há avaliações

- Investment Appraisal: Qs 435 Construction ECONOMICS IIDocumento38 páginasInvestment Appraisal: Qs 435 Construction ECONOMICS IIGithu RobertAinda não há avaliações

- Significance of Capital Budgeting: Discounted Cash Flow MethodDocumento8 páginasSignificance of Capital Budgeting: Discounted Cash Flow MethodSarwat AfreenAinda não há avaliações

- Capital Budgeting: Navigation SearchDocumento16 páginasCapital Budgeting: Navigation SearchVenkat Narayana ReddyAinda não há avaliações

- Engineering Economics Unit 4Documento44 páginasEngineering Economics Unit 4smnavaneethakrishnan.murugesanAinda não há avaliações

- Define Capital Budgeting Techniques in 40 CharactersDocumento2 páginasDefine Capital Budgeting Techniques in 40 CharactersMuhammad Akmal HossainAinda não há avaliações

- Capital Budgeting Methods for New Projects vs ReplacementsDocumento10 páginasCapital Budgeting Methods for New Projects vs ReplacementsTimAinda não há avaliações

- CAPITAL BUDGETING LECTURE NOTES MAY 22 - DodomaDocumento5 páginasCAPITAL BUDGETING LECTURE NOTES MAY 22 - DodomachabeAinda não há avaliações

- Capital Budgeting (Or Investment Appraisal) Is The Planning Process Used To Determine Whether A Firm's Long TermDocumento4 páginasCapital Budgeting (Or Investment Appraisal) Is The Planning Process Used To Determine Whether A Firm's Long TermAshish Kumar100% (2)

- Investment Evaluation CriteriaDocumento15 páginasInvestment Evaluation Criteriainq33108Ainda não há avaliações

- Capital budgeting process and techniquesDocumento9 páginasCapital budgeting process and techniquesshanza munawerAinda não há avaliações

- Topic VII Capital Budgeting TechniquesDocumento16 páginasTopic VII Capital Budgeting TechniquesSeph AgetroAinda não há avaliações

- (Lecture 1 & 2) - Introduction To Investment Appraisal MethodsDocumento21 páginas(Lecture 1 & 2) - Introduction To Investment Appraisal MethodsAjay Kumar Takiar100% (1)

- International Capital Budgeting ExplainedDocumento18 páginasInternational Capital Budgeting ExplainedHitesh Kumar100% (1)

- CH 08 Capital BudgetingDocumento51 páginasCH 08 Capital BudgetingLitika SachdevaAinda não há avaliações

- Capital Investment AppraisalDocumento3 páginasCapital Investment AppraisalGeorge Ayesa Sembereka Jr.Ainda não há avaliações

- Capital Budgeting Techniques and Process ExplainedDocumento6 páginasCapital Budgeting Techniques and Process ExplainedAdnan SethiAinda não há avaliações

- Capital BudgetingDocumento6 páginasCapital BudgetingKhushbu PriyadarshniAinda não há avaliações

- Capital BudgetingDocumento14 páginasCapital BudgetingD Y Patil Institute of MCA and MBAAinda não há avaliações

- Net Present Value: Capital Budgeting (Or Investment Appraisal) Is The Planning Process Used ToDocumento4 páginasNet Present Value: Capital Budgeting (Or Investment Appraisal) Is The Planning Process Used TorohitwinnerAinda não há avaliações

- Capital Budgeting Techniques and Tools for Evaluating Long-Term InvestmentsDocumento8 páginasCapital Budgeting Techniques and Tools for Evaluating Long-Term InvestmentsGm InwatiAinda não há avaliações

- FM AssignmentDocumento5 páginasFM AssignmentMuhammad Haris Muhammad AslamAinda não há avaliações

- Applied Corporate Finance. What is a Company worth?No EverandApplied Corporate Finance. What is a Company worth?Nota: 3 de 5 estrelas3/5 (2)

- Accounting and Finance for Business Strategic PlanningNo EverandAccounting and Finance for Business Strategic PlanningAinda não há avaliações

- Financial Derivatives ExplainedDocumento8 páginasFinancial Derivatives ExplainedAmit babarAinda não há avaliações

- Most Active Investors in The Indian Startup EcosyDocumento1 páginaMost Active Investors in The Indian Startup EcosyShashank MishraAinda não há avaliações

- Financial Manamegent Prelim ModuleDocumento52 páginasFinancial Manamegent Prelim ModuleExequiel Adrada100% (1)

- Research Proposal Impact of Capital Structure On Firms Performance FinalDocumento29 páginasResearch Proposal Impact of Capital Structure On Firms Performance FinalTennyson MudendaAinda não há avaliações

- Icici Securities Internship ReportDocumento33 páginasIcici Securities Internship ReportDhanush.RAinda não há avaliações

- Answer Key Chapter 1 Audit of Investments and Related AccountsDocumento22 páginasAnswer Key Chapter 1 Audit of Investments and Related AccountsBazinga HidalgoAinda não há avaliações

- Forecasting Exchange Rates 1Documento32 páginasForecasting Exchange Rates 1Afrianto Budi Aan100% (1)

- Risk and Return Analysis of Stocks: A Literature ReviewDocumento15 páginasRisk and Return Analysis of Stocks: A Literature ReviewNitesh TripathyAinda não há avaliações

- Beaver W 1968 The Information Content of Annual Earnings AnnouncementsDocumento15 páginasBeaver W 1968 The Information Content of Annual Earnings AnnouncementsYuvendren LingamAinda não há avaliações

- A Study On Asset Liability Management in Yes BankDocumento29 páginasA Study On Asset Liability Management in Yes BankSurabhi Purwar0% (1)

- Balance Sheet Analysis ConceptsDocumento34 páginasBalance Sheet Analysis ConceptsPrathamesh Deo100% (1)

- 8ff3e9 Listing of SecuritiesDocumento33 páginas8ff3e9 Listing of SecuritiesYashvi100% (1)

- Balangoda Plantations PLC and Madulsima Planrtations PLC (1193)Documento21 páginasBalangoda Plantations PLC and Madulsima Planrtations PLC (1193)Bajalock VirusAinda não há avaliações

- Relevance of EntrepreneurshipDocumento8 páginasRelevance of EntrepreneurshipCarlo AplacadorAinda não há avaliações

- Accounting for InflationDocumento6 páginasAccounting for InflationkunjapAinda não há avaliações

- (Final) Acco 30013 - Accounting For Special TransactionsDocumento20 páginas(Final) Acco 30013 - Accounting For Special TransactionsJona kelssAinda não há avaliações

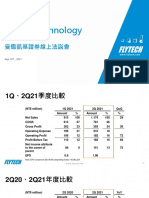

- Flytech TechnologyDocumento7 páginasFlytech TechnologyLouis ChenAinda não há avaliações

- Chap016 Financial Reporting AnalysisDocumento15 páginasChap016 Financial Reporting AnalysisThalia SandersAinda não há avaliações

- Module 6 Assignment Security AnalaysisDocumento4 páginasModule 6 Assignment Security AnalaysisCindy E. RamosAinda não há avaliações

- Presentation On Pre Acquisition and Post Acquisition, Cost of Control and Maturity InterestDocumento7 páginasPresentation On Pre Acquisition and Post Acquisition, Cost of Control and Maturity InterestShubham SharmaAinda não há avaliações

- Value Investing - Aswath DamodaranDocumento43 páginasValue Investing - Aswath Damodaranapi-3821333100% (1)

- Kotak Multi Asset Allocation Fund 2-Page (Front-Back) Leaflet A4 Printab...Documento2 páginasKotak Multi Asset Allocation Fund 2-Page (Front-Back) Leaflet A4 Printab...rajbir singh ChauhanAinda não há avaliações

- Principles of Corporate Finance 12th Edition Brealey Test BankDocumento19 páginasPrinciples of Corporate Finance 12th Edition Brealey Test BankGloria Nicol100% (30)

- Reverta 1st Half 2017 Financial ReportDocumento14 páginasReverta 1st Half 2017 Financial ReportpowpizzaAinda não há avaliações

- Blaine Kitchenware: Case Exhibit 1Documento15 páginasBlaine Kitchenware: Case Exhibit 1Fahad AliAinda não há avaliações

- Phases of StartupsDocumento5 páginasPhases of StartupsSAARANSH AGARWALAinda não há avaliações

- TRIAL Food Drink Marketplace Financial Model Excel Template v.1.0.122020Documento90 páginasTRIAL Food Drink Marketplace Financial Model Excel Template v.1.0.122020motebangAinda não há avaliações

- Pro Forma StatementDocumento14 páginasPro Forma StatementEse Peace100% (1)

- Kes 2 - EPPM3644 BBAE KL - CLEAR LAKE BAKERY - KUMP 3Documento5 páginasKes 2 - EPPM3644 BBAE KL - CLEAR LAKE BAKERY - KUMP 3Durga LetchumananAinda não há avaliações

- Accounts Important Questions by Rajat Jain SirDocumento31 páginasAccounts Important Questions by Rajat Jain SirRajiv JhaAinda não há avaliações