Você também pode gostar

- Florida Limited Liability Company Operating AgreementDocumento6 páginasFlorida Limited Liability Company Operating AgreementBaseer HaqqieAinda não há avaliações

- Home Assignment - JUNK BOND Subject: Corporate FinanceDocumento3 páginasHome Assignment - JUNK BOND Subject: Corporate FinanceAsad Mazhar100% (1)

- Gottfried Feder - The Programme of The NSDAPDocumento51 páginasGottfried Feder - The Programme of The NSDAPc108Ainda não há avaliações

- MODULE 04 - Engineering Economy - DepreciationDocumento22 páginasMODULE 04 - Engineering Economy - DepreciationNoel So jr100% (2)

- Practice Technicals 4Documento20 páginasPractice Technicals 4tigerAinda não há avaliações

- Applied Corporate Finance. What is a Company worth?No EverandApplied Corporate Finance. What is a Company worth?Nota: 3 de 5 estrelas3/5 (2)

- MODULE 05 - Engineering Economy - Present EconomyDocumento12 páginasMODULE 05 - Engineering Economy - Present EconomyNoel So jr100% (1)

- Final PDFDocumento21 páginasFinal PDFWaleed OsmanAinda não há avaliações

- Worktext in EE 006 (Basic EE For CE)Documento232 páginasWorktext in EE 006 (Basic EE For CE)Jean Divinagracia100% (1)

- (1 Point) : True FalseDocumento18 páginas(1 Point) : True FalseElla DavisAinda não há avaliações

- Engineering Economy: Capital FinancingDocumento17 páginasEngineering Economy: Capital FinancingJohn Kenneth MantesAinda não há avaliações

- British Guiana Village Administration 1838 To 1903 AshmoreDocumento12 páginasBritish Guiana Village Administration 1838 To 1903 AshmoreKAW100% (1)

- Accounting For Managers PDFDocumento367 páginasAccounting For Managers PDFNiranjan Kumar100% (2)

- Diageo AnalysisDocumento2 páginasDiageo Analysisgckodali0% (1)

- Uniform-Arithmetic-Gradient Encon 1 PDFDocumento4 páginasUniform-Arithmetic-Gradient Encon 1 PDFErina SmithAinda não há avaliações

- Annuity Lecture - Engineering EconomyDocumento13 páginasAnnuity Lecture - Engineering Economyjohnhenryyambao0% (1)

- Economical Study MethodsDocumento19 páginasEconomical Study MethodsJom Ancheta BautistaAinda não há avaliações

- Gradient Series and AsDocumento8 páginasGradient Series and AsJayrMenes100% (1)

- Glenview Capital Third Quarter 2009Documento12 páginasGlenview Capital Third Quarter 2009balevinAinda não há avaliações

- Engineering Economy Chapter # 02Documento55 páginasEngineering Economy Chapter # 02imran_chaudhryAinda não há avaliações

- Module 00 Engineering Economics PDFDocumento330 páginasModule 00 Engineering Economics PDFJON EDWARD ABAYAAinda não há avaliações

- UPSUMCO Vs CA CaseDocumento2 páginasUPSUMCO Vs CA CaseJohnson YaplinAinda não há avaliações

- Module 2 Engineering EconomicsDocumento15 páginasModule 2 Engineering EconomicsJohn Carlo Bacalando IIAinda não há avaliações

- Capital Recovery CostDocumento2 páginasCapital Recovery CostShahnaz NadivaAinda não há avaliações

- Nucor Steel ASTM A709 Plate Rolling ProcessDocumento54 páginasNucor Steel ASTM A709 Plate Rolling ProcessDave MulvihillAinda não há avaliações

- Nucor Steel ASTM A709 Plate Rolling ProcessDocumento54 páginasNucor Steel ASTM A709 Plate Rolling ProcessDave MulvihillAinda não há avaliações

- Nucor Steel ASTM A709 Plate Rolling ProcessDocumento54 páginasNucor Steel ASTM A709 Plate Rolling ProcessDave MulvihillAinda não há avaliações

- 04 - Money-Time Relationship and Equivalence CHE40Documento77 páginas04 - Money-Time Relationship and Equivalence CHE40Faye Blair Markova0% (1)

- Engineering EconomyDocumento5 páginasEngineering EconomyDayLe Ferrer AbapoAinda não há avaliações

- Steel Fabrication Kickoff Prefabrication Meeting AgendaDocumento3 páginasSteel Fabrication Kickoff Prefabrication Meeting AgendaDave Mulvihill100% (2)

- A Detailed Project On Secondary Market.Documento40 páginasA Detailed Project On Secondary Market.Jatin Anand100% (1)

- Engineering Economy: Cheerobie B. AranasDocumento27 páginasEngineering Economy: Cheerobie B. AranasCllyan ReyesAinda não há avaliações

- CH 10 - Credit AnalysisDocumento58 páginasCH 10 - Credit Analysishy_saingheng_760260967% (9)

- Engineering Economics Upm Samples 10Documento4 páginasEngineering Economics Upm Samples 10Cesia MontelloAinda não há avaliações

- IEMECON - HandoutsDocumento64 páginasIEMECON - HandoutsEzekiel BernardoAinda não há avaliações

- Chapter 3 - The Time Value of Money (Part I)Documento20 páginasChapter 3 - The Time Value of Money (Part I)Arin ParkAinda não há avaliações

- Solved Problems in Engineering Economy AccountingDocumento10 páginasSolved Problems in Engineering Economy Accountingsaleh gaziAinda não há avaliações

- Chapter 3.3 - Cashflow and Continuous Compounding Sample ProblemsDocumento14 páginasChapter 3.3 - Cashflow and Continuous Compounding Sample ProblemsArin ParkAinda não há avaliações

- Econ c3Documento51 páginasEcon c3larra100% (1)

- Fundamental Concepts: Engineering Economy 1Documento10 páginasFundamental Concepts: Engineering Economy 1Andre BocoAinda não há avaliações

- Thermo 27 45 1 29Documento18 páginasThermo 27 45 1 29Danerys Targaryan0% (1)

- Engg Econ - Part 1Documento22 páginasEngg Econ - Part 1Math Dandridge Ventura0% (1)

- Simple Interest Compound InterestDocumento6 páginasSimple Interest Compound InterestKaye OleaAinda não há avaliações

- Amortization and Uniform Arithmetic GradientDocumento20 páginasAmortization and Uniform Arithmetic GradientCyril Jay G. OrtegaAinda não há avaliações

- Session 6 - Evaluation of AlternativesDocumento7 páginasSession 6 - Evaluation of Alternativesmark flores100% (1)

- Econ 6Documento7 páginasEcon 6Lyzette LeanderAinda não há avaliações

- Engg. EconomicsDocumento2 páginasEngg. EconomicsStevenAinda não há avaliações

- Sharing Is CaringDocumento4 páginasSharing Is CaringChris bongalosaAinda não há avaliações

- Eeco 111716Documento20 páginasEeco 111716Rom HoboiiAinda não há avaliações

- Activity C - Annuities and Capitalized CostDocumento1 páginaActivity C - Annuities and Capitalized CostExcel MigsAinda não há avaliações

- Assignment #1 (Sep2019) - GDB3023-SolutionDocumento3 páginasAssignment #1 (Sep2019) - GDB3023-SolutionDanish ZabidiAinda não há avaliações

- Engineering Economy Lecture2Documento32 páginasEngineering Economy Lecture2Jaed CaraigAinda não há avaliações

- Engineering Economy Simple InterestDocumento1 páginaEngineering Economy Simple InterestNoreen Guiyab TannaganAinda não há avaliações

- Eeco HWDocumento19 páginasEeco HWRejed VillanuevaAinda não há avaliações

- Deferred AnnuityDocumento8 páginasDeferred AnnuityLAURENCE JAN BAGAANAinda não há avaliações

- ENGECODocumento3 páginasENGECOmgoldiieeee20% (5)

- TLA 8.4 Sample Problems On Types of Annuities - Types of Annuity Group No. 6 PDFDocumento10 páginasTLA 8.4 Sample Problems On Types of Annuities - Types of Annuity Group No. 6 PDFGian SanchezAinda não há avaliações

- Engineering Economy Part 3Documento13 páginasEngineering Economy Part 3Josiah FloresAinda não há avaliações

- Chapter 1 - Introduction - IE 112Documento12 páginasChapter 1 - Introduction - IE 112leojhunAinda não há avaliações

- Equation of Value For Ceit-04-501aDocumento9 páginasEquation of Value For Ceit-04-501aAngeli Mae SantosAinda não há avaliações

- Engineering Economy ReviewerDocumento5 páginasEngineering Economy ReviewerBea Abesamis100% (1)

- Handout 8.1 Annuity Due Sample ProblemsDocumento4 páginasHandout 8.1 Annuity Due Sample ProblemsEruel CruzAinda não há avaliações

- Solution 1-5 1Documento4 páginasSolution 1-5 1Dan Edison RamosAinda não há avaliações

- Engineering Economics - SolutionsDocumento11 páginasEngineering Economics - SolutionsIssacus Youssouf100% (1)

- Interest & DiscountDocumento5 páginasInterest & DiscountThur MykAinda não há avaliações

- ESENECO (7) Basic Methods For Making Economy StudiesDocumento17 páginasESENECO (7) Basic Methods For Making Economy StudiesNicole ReyesAinda não há avaliações

- Compiled Notes in EE40Documento29 páginasCompiled Notes in EE40April SaccuanAinda não há avaliações

- NUt 6 SA9 SSN 65Documento38 páginasNUt 6 SA9 SSN 65Don RomantikoAinda não há avaliações

- Lecture 1 Part 2 - Present EconomyDocumento9 páginasLecture 1 Part 2 - Present EconomyIvan Dave TorrecampoAinda não há avaliações

- Engineering Economy Lecture6Documento40 páginasEngineering Economy Lecture6Jaed CaraigAinda não há avaliações

- Cee 109 - First ExamDocumento43 páginasCee 109 - First ExamRonald Renon QuiranteAinda não há avaliações

- BES 221 (PART I - Prefinal Module)Documento9 páginasBES 221 (PART I - Prefinal Module)Kristy SalmingoAinda não há avaliações

- Orca Share Media1533208944176Documento90 páginasOrca Share Media1533208944176Christian Jimenez Reyes0% (1)

- Lecture 5Documento14 páginasLecture 5Khalid RehmanAinda não há avaliações

- MATHINVS - Simple Annuities 3.6Documento7 páginasMATHINVS - Simple Annuities 3.6Kathryn SantosAinda não há avaliações

- Engineering Economics: Rate of Return AnalysisDocumento29 páginasEngineering Economics: Rate of Return AnalysisEkoAinda não há avaliações

- Saw Storage HandlingDocumento1 páginaSaw Storage HandlingDave MulvihillAinda não há avaliações

- Rental Inspection Checklist: Entry Way & HallDocumento7 páginasRental Inspection Checklist: Entry Way & HallDave MulvihillAinda não há avaliações

- Miller - 2010 Welding Heavy Structural Steel SucessfulyyDocumento15 páginasMiller - 2010 Welding Heavy Structural Steel SucessfulyyLleiLleiAinda não há avaliações

- ASTM A572 Tensile RequirementsDocumento1 páginaASTM A572 Tensile RequirementsDave MulvihillAinda não há avaliações

- State of Idaho Public Works Statutes Rules 2021Documento55 páginasState of Idaho Public Works Statutes Rules 2021Dave MulvihillAinda não há avaliações

- Tech AlloyDocumento2 páginasTech AlloyDave MulvihillAinda não há avaliações

- 2014amended1 5 2015Documento997 páginas2014amended1 5 2015Dave MulvihillAinda não há avaliações

- Wsdot 9-06.8Documento1 páginaWsdot 9-06.8Dave MulvihillAinda não há avaliações

- 1-07 Legal Relations and Responsibilities To The Public: 1-07.1 Laws To Be ObservedDocumento3 páginas1-07 Legal Relations and Responsibilities To The Public: 1-07.1 Laws To Be ObservedDave MulvihillAinda não há avaliações

- Seattle 2011 Standard Specifications For ConstructionDocumento745 páginasSeattle 2011 Standard Specifications For ConstructionDave MulvihillAinda não há avaliações

- 1-07 Legal Relations and Responsibilities To The Public: 1-07.1 Laws To Be ObservedDocumento3 páginas1-07 Legal Relations and Responsibilities To The Public: 1-07.1 Laws To Be ObservedDave MulvihillAinda não há avaliações

- AAR M-201 - Norma Fundido para TremDocumento66 páginasAAR M-201 - Norma Fundido para TremFlavioNocelliAinda não há avaliações

- MFG333: Stat Methods Quality Improvement Final Class NotesDocumento2 páginasMFG333: Stat Methods Quality Improvement Final Class NotesDave MulvihillAinda não há avaliações

- Wsdot 9-06.8Documento1 páginaWsdot 9-06.8Dave MulvihillAinda não há avaliações

- Wsdot 6-03.3 (43) ADocumento1 páginaWsdot 6-03.3 (43) ADave MulvihillAinda não há avaliações

- Wsdot 6-03.3Documento3 páginasWsdot 6-03.3Dave MulvihillAinda não há avaliações

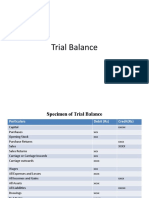

- Week 3 Lecture SlidesDocumento17 páginasWeek 3 Lecture SlidesDave MulvihillAinda não há avaliações

- Wsdot 9-06.8Documento1 páginaWsdot 9-06.8Dave MulvihillAinda não há avaliações

- Degree and Course InformationDocumento2 páginasDegree and Course InformationDave MulvihillAinda não há avaliações

- Seven Keys To Improving Customer SatisfactionDocumento4 páginasSeven Keys To Improving Customer SatisfactionDave MulvihillAinda não há avaliações

- OIT MFG333 Midterm NotesDocumento2 páginasOIT MFG333 Midterm NotesDave MulvihillAinda não há avaliações

- WABO Approved Fabricator Renewal: David MulvihillDocumento1 páginaWABO Approved Fabricator Renewal: David MulvihillDave MulvihillAinda não há avaliações

- Seattle 2011 Standard Specifications For ConstructionDocumento745 páginasSeattle 2011 Standard Specifications For ConstructionDave MulvihillAinda não há avaliações

- OIT MFG333 Midterm NotesDocumento2 páginasOIT MFG333 Midterm NotesDave MulvihillAinda não há avaliações

- Economics 201 Chapter 1Documento3 páginasEconomics 201 Chapter 1Dave MulvihillAinda não há avaliações

- Alaska Standard Specifications For Construction 2004Documento438 páginasAlaska Standard Specifications For Construction 2004Dave MulvihillAinda não há avaliações

- CREW: Department of Education: Regarding For-Profit Education: 12/3/10 - 10-01704-F NewDocumento343 páginasCREW: Department of Education: Regarding For-Profit Education: 12/3/10 - 10-01704-F NewCREWAinda não há avaliações

- Acc 7Documento4 páginasAcc 7ruthu ruthvikAinda não há avaliações

- Financial Modelling, Simulation, and Optimisation: Mihir Dash Alliance Business School, Bangalore, IndiaDocumento10 páginasFinancial Modelling, Simulation, and Optimisation: Mihir Dash Alliance Business School, Bangalore, IndiahaythoAinda não há avaliações

- UntitledDocumento53 páginasUntitledapi-228714775Ainda não há avaliações

- Financial Ratios of Unilever PakistanDocumento4 páginasFinancial Ratios of Unilever PakistanecicaAinda não há avaliações

- New Economics Boyle eDocumento5 páginasNew Economics Boyle eDi MitriAinda não há avaliações

- Licaros vs. Gatmaitan G.R. No. 142838, August 9, 2001Documento8 páginasLicaros vs. Gatmaitan G.R. No. 142838, August 9, 2001Fides DamascoAinda não há avaliações

- Holydays Homework EcoDocumento3 páginasHolydays Homework EcoAkshita ChauhanAinda não há avaliações

- Solutions Manual: Fundamentals of Corporate Finance (Asia Global Edition)Documento8 páginasSolutions Manual: Fundamentals of Corporate Finance (Asia Global Edition)Silver Bullet100% (1)

- Chp1 - Simple Interest and Simple DiscountDocumento13 páginasChp1 - Simple Interest and Simple DiscountYanie Taha0% (1)

- Title of Research WorkDocumento22 páginasTitle of Research WorkAnupam BaliAinda não há avaliações

- Course Module 1 Mathematics of InvestmentDocumento18 páginasCourse Module 1 Mathematics of InvestmentAnne Maerick Jersey OteroAinda não há avaliações

- Financial Management PDFDocumento7 páginasFinancial Management PDFdishu kumarAinda não há avaliações

- The Problem and Its Setting: North Eastern Mindanao State UniversityDocumento69 páginasThe Problem and Its Setting: North Eastern Mindanao State UniversityAnthony PonlaonAinda não há avaliações

- General Quarter 2 - Week 1: ZZZZZZDocumento14 páginasGeneral Quarter 2 - Week 1: ZZZZZZJakim Lopez0% (1)

- Credit RetingDocumento10 páginasCredit Retingnikhu_shuklaAinda não há avaliações

- Capital Structure: Particulars Company X Company YDocumento7 páginasCapital Structure: Particulars Company X Company YAbhishek GavandeAinda não há avaliações

- Tutorial Questions Unit 2-AnsDocumento9 páginasTutorial Questions Unit 2-AnsPrincessCC20Ainda não há avaliações