Você também pode gostar

- Shed Material List Part (1 of 9)Documento2 páginasShed Material List Part (1 of 9)nwright_besterAinda não há avaliações

- Shed PlansDocumento1 páginaShed PlansFrancis Wolfgang UrbanAinda não há avaliações

- Shed PlansDocumento1 páginaShed PlansFrancis Wolfgang UrbanAinda não há avaliações

- Shed PlansDocumento1 páginaShed PlansFrancis Wolfgang UrbanAinda não há avaliações

- Build and Use Small Electric MotorsDocumento5 páginasBuild and Use Small Electric MotorsdarkquinkAinda não há avaliações

- Shed PlansDocumento16 páginasShed PlansFrancis Wolfgang Urban100% (7)

- 15 Foot SailDocumento4 páginas15 Foot SailjdogheadAinda não há avaliações

- Figure E Small Roof: 2x4 Nailers 2x4 Rafter 2x4 Subfascia 1x2 Fascia Trim 24" 32" 29-3/4"Documento1 páginaFigure E Small Roof: 2x4 Nailers 2x4 Rafter 2x4 Subfascia 1x2 Fascia Trim 24" 32" 29-3/4"Francis Wolfgang UrbanAinda não há avaliações

- Shed PlansDocumento1 páginaShed PlansFrancis Wolfgang Urban50% (2)

- Shed PlansDocumento1 páginaShed PlansFrancis Wolfgang UrbanAinda não há avaliações

- 6 Inch Reflector PlansDocumento12 páginas6 Inch Reflector PlansSektordrAinda não há avaliações

- Build a DIY Motorized Mountain BuggyDocumento5 páginasBuild a DIY Motorized Mountain Buggyjii_907001Ainda não há avaliações

- Figure A Trusses: Inner (Common) Truss (9 Req'd)Documento1 páginaFigure A Trusses: Inner (Common) Truss (9 Req'd)Francis Wolfgang UrbanAinda não há avaliações

- 10 Dollar Telescope PlansDocumento9 páginas10 Dollar Telescope Planssandhi88Ainda não há avaliações

- 25 Foot CabinDocumento28 páginas25 Foot Cabinapi-3708365100% (1)

- 3inchrefractorDocumento6 páginas3inchrefractorGianluca SalvatoAinda não há avaliações

- IRS Publication Form Instructions 8941Documento10 páginasIRS Publication Form Instructions 8941Francis Wolfgang UrbanAinda não há avaliações

- 3 Wheel Dune BuggyDocumento5 páginas3 Wheel Dune BuggyyukitadaAinda não há avaliações

- IRS Publication Form Instructions w-2/w-3Documento13 páginasIRS Publication Form Instructions w-2/w-3Francis Wolfgang UrbanAinda não há avaliações

- IRS Publication Form Instructions 8594Documento3 páginasIRS Publication Form Instructions 8594Francis Wolfgang UrbanAinda não há avaliações

- IRS Publication Form Instructions 8829Documento4 páginasIRS Publication Form Instructions 8829Francis Wolfgang UrbanAinda não há avaliações

- IRS Publication Form Instructions 8867Documento2 páginasIRS Publication Form Instructions 8867Francis Wolfgang UrbanAinda não há avaliações

- IRS Publication Form Instructions 8283Documento7 páginasIRS Publication Form Instructions 8283Francis Wolfgang UrbanAinda não há avaliações

- Form 8853 InstructionsDocumento8 páginasForm 8853 InstructionsFrancis Wolfgang UrbanAinda não há avaliações

- IRS Publication Form Instructions 1120sDocumento42 páginasIRS Publication Form Instructions 1120sFrancis Wolfgang UrbanAinda não há avaliações

- IRS Publication Form Instructions 2106Documento8 páginasIRS Publication Form Instructions 2106Francis Wolfgang UrbanAinda não há avaliações

- IRS Publication Form Instructions 5405Documento6 páginasIRS Publication Form Instructions 5405Francis Wolfgang UrbanAinda não há avaliações

- IRS Publication Form Instructions 4797Documento10 páginasIRS Publication Form Instructions 4797Francis Wolfgang UrbanAinda não há avaliações

- IRS Publication Form Instructions SseDocumento6 páginasIRS Publication Form Instructions SseFrancis Wolfgang UrbanAinda não há avaliações

- Instructions for Form 1099-MISCDocumento10 páginasInstructions for Form 1099-MISCFrancis Wolfgang UrbanAinda não há avaliações

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5783)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- Hunter Biden IndictmentDocumento56 páginasHunter Biden IndictmentWashington ExaminerAinda não há avaliações

- ISACA 2023 Invoice PDFDocumento6 páginasISACA 2023 Invoice PDFSatish Kumar Reddy ByreddyAinda não há avaliações

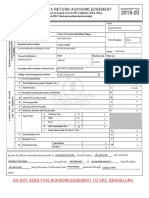

- Indian Income Tax Return Acknowledgement for AY 2019-20Documento1 páginaIndian Income Tax Return Acknowledgement for AY 2019-20Sourav KumarAinda não há avaliações

- April 2021 PAYSLIPDocumento1 páginaApril 2021 PAYSLIPPuja ParekhAinda não há avaliações

- Form 1625062023 043026Documento2 páginasForm 1625062023 043026SHIV BHAJANAinda não há avaliações

- Taxation in IndiaDocumento2 páginasTaxation in Indiasharpshooter0999Ainda não há avaliações

- 68 - Vrundavan ConstructionDocumento1 página68 - Vrundavan ConstructionTikaram PatelAinda não há avaliações

- Journal EntriesDocumento3 páginasJournal EntrieskatAinda não há avaliações

- HTTP Myhr - Bsnl.co - in Portal Pay IncomeTaxDetailsDocumento1 páginaHTTP Myhr - Bsnl.co - in Portal Pay IncomeTaxDetailssudhakar9v2807Ainda não há avaliações

- Form PDFDocumento1 páginaForm PDFChinmoyee SharmaAinda não há avaliações

- Assignment Do It Yourself (Diy)Documento3 páginasAssignment Do It Yourself (Diy)Marites AmorsoloAinda não há avaliações

- CIR Vs Eastern TelecommunicationsDocumento1 páginaCIR Vs Eastern TelecommunicationsLizzy WayAinda não há avaliações

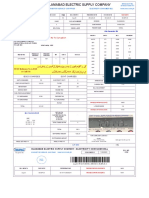

- IESCO Electricity Bill DetailsDocumento1 páginaIESCO Electricity Bill DetailsUmar FarooqAinda não há avaliações

- F3ltd-Payroll With Payslip FormatDocumento6 páginasF3ltd-Payroll With Payslip FormatSonu PathakAinda não há avaliações

- TAX Remedies AmponganDocumento2 páginasTAX Remedies AmponganCharie Mae YdAinda não há avaliações

- PayslipDocumento3 páginasPayslipkarnancy100% (1)

- EKPO PO Details and Asset Master DataDocumento3 páginasEKPO PO Details and Asset Master DatashekarAinda não há avaliações

- Mindanao Bus Co. v. City Assessor and Treasurer - ACERODocumento1 páginaMindanao Bus Co. v. City Assessor and Treasurer - ACEROjosef.acero1Ainda não há avaliações

- Cir V American Express International, IncDocumento1 páginaCir V American Express International, IncDinahAinda não há avaliações

- Indian Income Tax Return AcknowledgementDocumento1 páginaIndian Income Tax Return Acknowledgementaloka.rajAinda não há avaliações

- CP 52 FormDocumento1 páginaCP 52 FormghaniAinda não há avaliações

- Unit 04 Input Tax CreditDocumento20 páginasUnit 04 Input Tax CreditSathya saiAinda não há avaliações

- Ledger Confirmation DetailsDocumento3 páginasLedger Confirmation Detailshemant sharmaAinda não há avaliações

- Fqnrfy202223itall WORD PrintDocumento1.642 páginasFqnrfy202223itall WORD PrintsysfqnrAinda não há avaliações

- RMC No. 134-2020Documento1 páginaRMC No. 134-2020nathalie velasquezAinda não há avaliações

- 2023 - AST - AFTPT2727B - Show Cause Notice - 1057871080 (1) - 10112023Documento2 páginas2023 - AST - AFTPT2727B - Show Cause Notice - 1057871080 (1) - 10112023Vishwas ThakurAinda não há avaliações

- Multi-State Taxation 2021Documento2 páginasMulti-State Taxation 2021Finn KevinAinda não há avaliações

- Computation - Suraj ShahDocumento3 páginasComputation - Suraj ShahSUJIT SINGHAinda não há avaliações

- Provisions On Taxation or Revenue SharingDocumento2 páginasProvisions On Taxation or Revenue SharingAustin Coles33% (3)

- RMC No. 73-2019 - Annex ADocumento1 páginaRMC No. 73-2019 - Annex ALeo R.Ainda não há avaliações