Você também pode gostar

- Corpo Case Digests 2Documento41 páginasCorpo Case Digests 2Marshan GualbertoAinda não há avaliações

- Alcan Pakaging Starpack Corporation vs. The City Treasurer of Manila PDFDocumento3 páginasAlcan Pakaging Starpack Corporation vs. The City Treasurer of Manila PDFJuralexAinda não há avaliações

- Calasanz Vs CommDocumento4 páginasCalasanz Vs CommEAAinda não há avaliações

- Activity 9 - ComplaintDocumento5 páginasActivity 9 - ComplaintGilbert A. RecosanaAinda não há avaliações

- Gabionza v. CADocumento17 páginasGabionza v. CADelmar Jess TuquibAinda não há avaliações

- Bertillo - Phil. Guaranty Co. Inc. Vs CIR and CTADocumento2 páginasBertillo - Phil. Guaranty Co. Inc. Vs CIR and CTAStella BertilloAinda não há avaliações

- Valera Vs VelascoDocumento6 páginasValera Vs VelascoRyanAinda não há avaliações

- CIR V Puregold Duty FreeDocumento4 páginasCIR V Puregold Duty FreeCelina Marie Panaligan0% (1)

- City of Manila Vs ColetDocumento3 páginasCity of Manila Vs ColetErika ColladoAinda não há avaliações

- CIR V Raul Gonzales DigestDocumento3 páginasCIR V Raul Gonzales DigestEstelle Rojas TanAinda não há avaliações

- Corp Cases - 1st WeekDocumento55 páginasCorp Cases - 1st WeekJanineAinda não há avaliações

- 119willaware Products V Jesichris Manufacturing (Gonzales, Rafael)Documento1 página119willaware Products V Jesichris Manufacturing (Gonzales, Rafael)Rafael GonzalesAinda não há avaliações

- South African Airways Vs CIR GR No 180356 February 16 2010Documento7 páginasSouth African Airways Vs CIR GR No 180356 February 16 2010Jacinto Jr JameroAinda não há avaliações

- Wise Holdings vs. Garcia (Digest)Documento2 páginasWise Holdings vs. Garcia (Digest)Miguel Alleandro Alag100% (1)

- Ab Initio or Is Rescindable by Reason of The Fraudulent Concealment orDocumento2 páginasAb Initio or Is Rescindable by Reason of The Fraudulent Concealment orIldefonso HernaezAinda não há avaliações

- Estate and Donor's TaxDocumento6 páginasEstate and Donor's TaxKimberly SendinAinda não há avaliações

- 08 Proton V RepublicDocumento2 páginas08 Proton V RepublicJoshua Erik MadriaAinda não há avaliações

- CIR Vs BinalbaganDocumento2 páginasCIR Vs BinalbaganjohnkyleAinda não há avaliações

- Omandan v. CADocumento7 páginasOmandan v. CAJoanne CamacamAinda não há avaliações

- 3-Cir VS LealDocumento3 páginas3-Cir VS LealRenEleponioAinda não há avaliações

- Bir Ruling 197-93 (May 7, 1993)Documento5 páginasBir Ruling 197-93 (May 7, 1993)matinikkiAinda não há avaliações

- Tax VAT CIR Vs GotamcoDocumento3 páginasTax VAT CIR Vs GotamcoRhea Mae A. SibalaAinda não há avaliações

- 2019 Bar Review: Taxation Law Chair'S CasesDocumento19 páginas2019 Bar Review: Taxation Law Chair'S CasesClarisse-joan Bumanglag GarmaAinda não há avaliações

- Macapinlac vs. Gutierrez Repide Jose C. Macapinlac, vs. Francisco Gutierrez Repide, Et Al. G.R. No. 18574 September 20, 1922Documento2 páginasMacapinlac vs. Gutierrez Repide Jose C. Macapinlac, vs. Francisco Gutierrez Repide, Et Al. G.R. No. 18574 September 20, 1922Joanna May G CAinda não há avaliações

- Case Digests On Civil ProcedureDocumento21 páginasCase Digests On Civil ProcedureAingel Joy DomingoAinda não há avaliações

- Asiaworld Vs CIR - CDDocumento2 páginasAsiaworld Vs CIR - CDNolas JayAinda não há avaliações

- Agency - EDocumento25 páginasAgency - EvalkyriorAinda não há avaliações

- Pansacola v. CIRDocumento3 páginasPansacola v. CIRSean GalvezAinda não há avaliações

- 32 College of Oral & Dental Surgery V CTADocumento2 páginas32 College of Oral & Dental Surgery V CTAReinier Jeffrey AbdonAinda não há avaliações

- Evangelista Vs CollectorDocumento1 páginaEvangelista Vs CollectorLisa GarciaAinda não há avaliações

- Philex Mining vs. CIR, 294 SCRA 687Documento12 páginasPhilex Mining vs. CIR, 294 SCRA 687KidMonkey2299Ainda não há avaliações

- G.R. No. 190506 Coral Bay Nickel Corporation, Petitioner, Commissioner of Internal Revenue, Respondent. Decision Bersamin, J.Documento3 páginasG.R. No. 190506 Coral Bay Nickel Corporation, Petitioner, Commissioner of Internal Revenue, Respondent. Decision Bersamin, J.carlo_tabangcuraAinda não há avaliações

- Santos Vs CA Civ Pro Digest by BebebaaDocumento3 páginasSantos Vs CA Civ Pro Digest by BebebaabebebaaAinda não há avaliações

- Conwi v. Court of Tax Appeals, G.R. No. 48532, August 31, 1992Documento6 páginasConwi v. Court of Tax Appeals, G.R. No. 48532, August 31, 1992zac100% (1)

- CIR Vs PERFDocumento2 páginasCIR Vs PERFKring-kring Peralta BiscaydaAinda não há avaliações

- Alcan Packaging Starpack Corp. v. The Treasurer of The City of ManilaDocumento2 páginasAlcan Packaging Starpack Corp. v. The Treasurer of The City of ManilaCharles Roger RayaAinda não há avaliações

- Procter and Gamble Phils. (204 SCRA 377)Documento3 páginasProcter and Gamble Phils. (204 SCRA 377)Karl MinglanaAinda não há avaliações

- IBM Daksh Vs Rosallie LABORDocumento1 páginaIBM Daksh Vs Rosallie LABORLemuel Angelo M. EleccionAinda não há avaliações

- Velasquez - Jr. - v. - Lisondra - Land - Inc.20201104-8-1ectq1eDocumento17 páginasVelasquez - Jr. - v. - Lisondra - Land - Inc.20201104-8-1ectq1eJade ClementeAinda não há avaliações

- F108Documento3 páginasF108Jheng NuquiAinda não há avaliações

- Meralco Vs YatcoDocumento4 páginasMeralco Vs YatcoArkhaye SalvatoreAinda não há avaliações

- Lincoln Philippine Life Insurance Company, Inc Vs CADocumento10 páginasLincoln Philippine Life Insurance Company, Inc Vs CAJazem AnsamaAinda não há avaliações

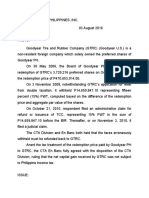

- CIR V Goodyear Philippines Inc., G.R. No. 216130, August 3, 2016.Documento2 páginasCIR V Goodyear Philippines Inc., G.R. No. 216130, August 3, 2016.mae ann rodolfoAinda não há avaliações

- CIR V CTA and Smith KlineDocumento1 páginaCIR V CTA and Smith KlineEmman CariñoAinda não há avaliações

- Prudential Bank Vs NLRCDocumento2 páginasPrudential Bank Vs NLRCErika Mariz CunananAinda não há avaliações

- 957 959Documento19 páginas957 959Erwin April MidsapakAinda não há avaliações

- Filipinas Synthetic Fiber Corporation vs. CA, Cta, and CirDocumento1 páginaFilipinas Synthetic Fiber Corporation vs. CA, Cta, and CirmwaikeAinda não há avaliações

- SILICON PHILIPPINES, INC., (Formerly INTEL PHILIPPINES MANUFACTURING, INC.) vs. COMMISSIONER OF INTERNAL REVENUEDocumento4 páginasSILICON PHILIPPINES, INC., (Formerly INTEL PHILIPPINES MANUFACTURING, INC.) vs. COMMISSIONER OF INTERNAL REVENUETrishaAinda não há avaliações

- Atlas Consolidated Mining Vs CIRDocumento6 páginasAtlas Consolidated Mining Vs CIRMarvin MagaipoAinda não há avaliações

- Bar Examination 2004: TaxationDocumento8 páginasBar Examination 2004: TaxationbubblingbrookAinda não há avaliações

- Sample ComplaintDocumento6 páginasSample ComplaintFrancess Mae AlonzoAinda não há avaliações

- PNB Vs CA Case DigestDocumento2 páginasPNB Vs CA Case Digesttine delos santosAinda não há avaliações

- Lim Tong Lim v. Philippine Fishing Gear Industries Inc. 317 SCRA 728Documento12 páginasLim Tong Lim v. Philippine Fishing Gear Industries Inc. 317 SCRA 728Dennis VelasquezAinda não há avaliações

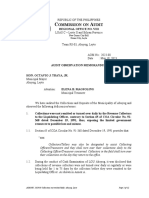

- AOM 2023-008 Collections Not Remitted DailyDocumento13 páginasAOM 2023-008 Collections Not Remitted DailyKean Fernand BocaboAinda não há avaliações

- FAY V WitteDocumento2 páginasFAY V WitteKeith Ivan Ong MeridoresAinda não há avaliações

- Deutsche Bank vs. CirDocumento1 páginaDeutsche Bank vs. CirDee WhyAinda não há avaliações

- CIR v. Cebu PortlandDocumento2 páginasCIR v. Cebu PortlandChelle OngAinda não há avaliações

- CIR v. Asalus CorpDocumento9 páginasCIR v. Asalus CorpMeg ReyesAinda não há avaliações

- 8 Sison Vs AnchetaDocumento1 página8 Sison Vs AnchetarjAinda não há avaliações

- G.R. No. L-9061Documento5 páginasG.R. No. L-9061Eloisa FloresAinda não há avaliações

- Cases Right of WayDocumento33 páginasCases Right of WayLizzzAinda não há avaliações

- Army Book NagaDocumento14 páginasArmy Book NagaLileath100% (1)

- The Sopranos - Complete 1st Season (DVDRip - Xvid) (h33t) (Big - Dad - E)Documento3 páginasThe Sopranos - Complete 1st Season (DVDRip - Xvid) (h33t) (Big - Dad - E)Canea VasileAinda não há avaliações

- Brimite v. United States of America - Document No. 14Documento2 páginasBrimite v. United States of America - Document No. 14Justia.comAinda não há avaliações

- Crime FictionDocumento19 páginasCrime FictionsanazhAinda não há avaliações

- Carlos BolusanDocumento14 páginasCarlos BolusanCristel BagaoisanAinda não há avaliações

- Magallona V Ermita Case DigestDocumento2 páginasMagallona V Ermita Case DigestJenny Cypres-Paguiligan82% (11)

- Lokpal and Lokayukta by Abhash Aryan (1701001)Documento6 páginasLokpal and Lokayukta by Abhash Aryan (1701001)abhashAinda não há avaliações

- Persepolis Notes GatheredDocumento34 páginasPersepolis Notes Gatheredgemma costelloAinda não há avaliações

- CrimRev Cases - Aug 4 2018 COMPRESSEDDocumento156 páginasCrimRev Cases - Aug 4 2018 COMPRESSEDJohn Patrick GarciaAinda não há avaliações

- Primary Jurisdiction and Exhaustion of Administrative RemediesDocumento23 páginasPrimary Jurisdiction and Exhaustion of Administrative RemediesFernan Del Espiritu Santo100% (2)

- Prubankers Association Vs Prudential BankDocumento2 páginasPrubankers Association Vs Prudential BankGillian Caye Geniza Briones0% (1)

- Williams Homelessness March12Documento6 páginasWilliams Homelessness March12Rasaq MojeedAinda não há avaliações

- Broidy vs. Global Risk Advisors LLC Et Al.Documento112 páginasBroidy vs. Global Risk Advisors LLC Et Al.Mike SmithAinda não há avaliações

- Native Tribes of Britain The CeltsDocumento3 páginasNative Tribes of Britain The Celtsmaría joséAinda não há avaliações

- Philippine Banking Corp. v. Judge TensuanDocumento3 páginasPhilippine Banking Corp. v. Judge TensuanCHRISTY NGALOYAinda não há avaliações

- Project Snowblind - Manual - PS2 PDFDocumento15 páginasProject Snowblind - Manual - PS2 PDFJasonAinda não há avaliações

- 2013.09.20 Letter To SEC Chair WhiteDocumento4 páginas2013.09.20 Letter To SEC Chair WhiteJoe WallinAinda não há avaliações

- From Here To Eternity (1953) Full PDFDocumento10 páginasFrom Here To Eternity (1953) Full PDFapdesaidwdAinda não há avaliações

- 15 4473 RTJDocumento6 páginas15 4473 RTJEd MoralesAinda não há avaliações

- History MSDocumento18 páginasHistory MSAnshu RajputAinda não há avaliações

- Merovingian Women's Clothing of The 6th & 7th CenturiesDocumento23 páginasMerovingian Women's Clothing of The 6th & 7th CenturiesLibby Brooks100% (3)

- Pro-Ante AgreementDocumento1 páginaPro-Ante AgreementAmber NicosiaAinda não há avaliações

- Adeptus Titanicus - Armes Ref SheetDocumento2 páginasAdeptus Titanicus - Armes Ref SheetPsyKo TineAinda não há avaliações

- Public Int'l Law Has Traditionally Been Regarded As A System of Principles and Rules Designed To Govern Relations Between Sovereign StatesDocumento59 páginasPublic Int'l Law Has Traditionally Been Regarded As A System of Principles and Rules Designed To Govern Relations Between Sovereign StatesStuti BaradiaAinda não há avaliações

- Waeker v. American Family, 10th Cir. (2008)Documento5 páginasWaeker v. American Family, 10th Cir. (2008)Scribd Government DocsAinda não há avaliações

- UAPSA ChaptersDocumento7 páginasUAPSA ChaptersHarvin Julius LasqueroAinda não há avaliações

- Zulhairy KamaruzamanDocumento17 páginasZulhairy KamaruzamanLavernyaAinda não há avaliações

- Note From Steve Clemons:confidential PDFDocumento1 páginaNote From Steve Clemons:confidential PDFB50% (2)

- Case DigestDocumento2 páginasCase DigestBHEJAY ORTIZAinda não há avaliações