Yen impact on corporate Japan

Macro Economic Research May 2013

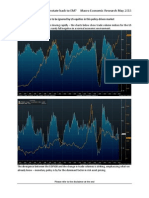

In the recent articles Japan follow up Institutional Exposures and Japan the end of the beginning I have discussed Japanese households financial asset positioning (only some 12.5% in assets that would provide protection in a weaker Yen/higher inflation scenario) and Japanese Institutional hedging (foreign security holdings are typically 80% hedged back into the Yen). What about the corporate sector? How much of the benefits of the weaker Yen are already in the numbers? Toyota reported results for the year to March 2013 on 8th May, so providing us with a topical opportunity to examine this. Their consolidated financial summary is below:

An 18% increase in Revenue was leveraged into a 271% increase in operating profit. The average Yen for the financial year ended March 31 2013 is shown as 83 to the USD, compared to an average of 79 in 2012. The spot rate as I write is over 101, some 22% weaker. The impact of a weaker Yen has not significantly been reflected yet in Toyotas profits. Toyota also provides a forecast for the year ahead:

Please refer to the disclaimer at the end

Yen impact on corporate Japan

Macro Economic Research May 2013

Revenue is expected to grow by 6.5% and operating income by 36%. This uses an average USDJPY of 90 depreciating off the F2013 rate of 83. In reconciling 2013 with the forecast 2014 numbers Toyota specifically identifies the effect of an 8.4% weaker Yen as +Y460bn. If we assume the Yen averages at 100 in F2014 (a 20% depreciation), a simplistic pro-rata adjustment gives us Operating Income of Y2460bn (+86%) for 2014. This is 18% higher than the current consensus forecast operating income per Bloomberg of Y2077bn. Conclusion It is clear that the impact of a weaker Yen still needs to be reflected in Japanese corporates financial accounts and to a lesser extent the forecasts of market participants.

Kevin Cousins is a portfolio manager at Brait Capital Management Limited. ("BraitCM"). This article is prepared by Kevin as an outside business activity. As such, BraitCM does not review or approve materials presented herein. The opinions and any recommendations expressed in this article are those of the author and do not reflect the opinions or recommendations of BraitCM. None of the information or opinions expressed in this article constitutes a solicitation for the purchase or sale of any security or other instrument. Nothing in this article constitutes investment advice and any recommendations that may be contained herein have not been based upon a consideration of the investment objectives, financial situation or particular needs of any specific recipient. Any purchase or sale activity in any securities or other instrument should be based upon your own analysis and conclusions. Either BraitCM or Kevin Cousins may hold or control long or short positions in the securities or instruments mentioned.

Please refer to the disclaimer at the end

Você também pode gostar

- Bilans Uspeha - PROFIT AND LOSS ACCOUNTDocumento2 páginasBilans Uspeha - PROFIT AND LOSS ACCOUNTLorimer010100% (7)

- EY AlpineValuation PDFDocumento36 páginasEY AlpineValuation PDFStuff NewsroomAinda não há avaliações

- FAR MockBoard (NFJPIA) - 2017Documento9 páginasFAR MockBoard (NFJPIA) - 2017ken100% (1)

- 655 Week 9 Notes PDFDocumento75 páginas655 Week 9 Notes PDFsanaha786Ainda não há avaliações

- Japan The End of The Beginning 2013 04Documento8 páginasJapan The End of The Beginning 2013 04kcousinsAinda não há avaliações

- Japan Follow Up Institutional Exposures 2013 05Documento2 páginasJapan Follow Up Institutional Exposures 2013 05kcousinsAinda não há avaliações

- Its Impact 2Documento2 páginasIts Impact 2Vipul GhoghariAinda não há avaliações

- IVA Worldwide QR 2Q13Documento2 páginasIVA Worldwide QR 2Q13BaikaniAinda não há avaliações

- Data1203 All PDFDocumento288 páginasData1203 All PDFlehoangthuchienAinda não há avaliações

- Yes Bank - EnamDocumento3 páginasYes Bank - Enamdeepak1126Ainda não há avaliações

- Market Outlook 12th January 2012Documento4 páginasMarket Outlook 12th January 2012Angel BrokingAinda não há avaliações

- Fundamental Analysis of Airtel ReportDocumento29 páginasFundamental Analysis of Airtel ReportKoushik G SaiAinda não há avaliações

- Maverick Capital Q1 2011Documento13 páginasMaverick Capital Q1 2011Yingluq100% (1)

- Manager's Review: /NYSE ArcaDocumento2 páginasManager's Review: /NYSE Arcaracheltan925Ainda não há avaliações

- (Kotak) ICICI Bank, January 31, 2013Documento14 páginas(Kotak) ICICI Bank, January 31, 2013Chaitanya JagarlapudiAinda não há avaliações

- Consolidation Update - Why This Stock Is Undervalued, and Not Many People Know About ItDocumento16 páginasConsolidation Update - Why This Stock Is Undervalued, and Not Many People Know About ItEdmund TanAinda não há avaliações

- Top-Down Valuation (EIC Analysis) : EconomyDocumento5 páginasTop-Down Valuation (EIC Analysis) : EconomyManas MohapatraAinda não há avaliações

- SGX APAC Ex Japan Dividend Leaders REIT Index FactsheetDocumento4 páginasSGX APAC Ex Japan Dividend Leaders REIT Index FactsheetZachary NgAinda não há avaliações

- Triveni Turbines: Growth On Track Maintain BuyDocumento3 páginasTriveni Turbines: Growth On Track Maintain Buyajd.nanthakumarAinda não há avaliações

- Barcap GDP Weighted FXDocumento2 páginasBarcap GDP Weighted FXRoberto PerezAinda não há avaliações

- HCL Technologies Ltd. - Q4FY11 Result UpdateDocumento3 páginasHCL Technologies Ltd. - Q4FY11 Result UpdateSeema GusainAinda não há avaliações

- Market Outlook 6th January 2012Documento4 páginasMarket Outlook 6th January 2012Angel BrokingAinda não há avaliações

- Marketexpress: How Long Can Japan Afford Its Huge Debt Ratio?Documento2 páginasMarketexpress: How Long Can Japan Afford Its Huge Debt Ratio?Ernesto MoriartyAinda não há avaliações

- Lane Asset Management Stock Market Commentary September 2015Documento10 páginasLane Asset Management Stock Market Commentary September 2015Edward C LaneAinda não há avaliações

- SBP - Analyst Briefing NoteDocumento3 páginasSBP - Analyst Briefing Notemuddasir1980Ainda não há avaliações

- 2008 Vs 2011 Stock SaleDocumento7 páginas2008 Vs 2011 Stock Salevjignesh1Ainda não há avaliações

- IDBI Bank Q2FY12 Result UpdateDocumento3 páginasIDBI Bank Q2FY12 Result UpdateSeema GusainAinda não há avaliações

- Market Analysis August 2020Documento23 páginasMarket Analysis August 2020noobcatcherAinda não há avaliações

- Wal-Mart Business Valuation: September 2011Documento27 páginasWal-Mart Business Valuation: September 2011Vaishali SharmaAinda não há avaliações

- Weekly Market Commentary 06-27-2011Documento2 páginasWeekly Market Commentary 06-27-2011Jeremy A. MillerAinda não há avaliações

- Oneliners P6Documento8 páginasOneliners P6Nirvana BoyAinda não há avaliações

- Thematic Insights - Welcome 2014Documento3 páginasThematic Insights - Welcome 2014Jignesh71Ainda não há avaliações

- Maruthi Suzuki India Ratio Research Paper (A.ruthwik Bharadwaj)Documento10 páginasMaruthi Suzuki India Ratio Research Paper (A.ruthwik Bharadwaj)jrntr7799Ainda não há avaliações

- Fearful Symmetry Nov 2011Documento4 páginasFearful Symmetry Nov 2011ChrisBeckerAinda não há avaliações

- Market Outlook 22nd November 2011Documento4 páginasMarket Outlook 22nd November 2011Angel BrokingAinda não há avaliações

- Weekly Market CommentaryDocumento4 páginasWeekly Market CommentaryDavid BriggsAinda não há avaliações

- Black Stone Webcast - Outlook For US & Europe 2011.10.05Documento12 páginasBlack Stone Webcast - Outlook For US & Europe 2011.10.05nicknyseAinda não há avaliações

- RMB Nigeria Stockbrokers: A Period of Rising Rates: What Next For Equities?Documento13 páginasRMB Nigeria Stockbrokers: A Period of Rising Rates: What Next For Equities?Jul AAinda não há avaliações

- Snapshot For Straits Times Index STI (FSSTI) Straits Times Index (STI)Documento2 páginasSnapshot For Straits Times Index STI (FSSTI) Straits Times Index (STI)api-237906069Ainda não há avaliações

- July 2019 NewsletterDocumento6 páginasJuly 2019 NewsletterRaghav BehaniAinda não há avaliações

- Ratio Analysis Is The One of The Instruments Used For Measuring Financial Success of CompaniesDocumento3 páginasRatio Analysis Is The One of The Instruments Used For Measuring Financial Success of CompaniesSapcon ThePhoenixAinda não há avaliações

- Global Macro Commentary April 2Documento3 páginasGlobal Macro Commentary April 2dpbasicAinda não há avaliações

- AP REIT - Fund Flash May'21Documento2 páginasAP REIT - Fund Flash May'21Guan JooAinda não há avaliações

- Domestic & External Debt Situation - Debt Maturities Expected To Remain Within LimitsDocumento4 páginasDomestic & External Debt Situation - Debt Maturities Expected To Remain Within LimitsMuhammad Ali KhanAinda não há avaliações

- The Marginal Pressure Factor Its Relationship With The SPY & BND in 2011Documento9 páginasThe Marginal Pressure Factor Its Relationship With The SPY & BND in 2011GlobMacResAinda não há avaliações

- Economist Insights 20120716Documento2 páginasEconomist Insights 20120716buyanalystlondonAinda não há avaliações

- Man AHL Analysis CTA Intelligence - On The Dangers of Following The Consensus ENG 20141022Documento1 páginaMan AHL Analysis CTA Intelligence - On The Dangers of Following The Consensus ENG 20141022kevinAinda não há avaliações

- Blog - Is This A Defining Moment For The Bond MarketDocumento4 páginasBlog - Is This A Defining Moment For The Bond MarketOwm Close CorporationAinda não há avaliações

- Optimal Fiscal Policy Rule For Achieving Fiscal Sustainability: A Japanese Case StudyDocumento19 páginasOptimal Fiscal Policy Rule For Achieving Fiscal Sustainability: A Japanese Case StudyADBI PublicationsAinda não há avaliações

- Fundamentalanalysis 150227053710 Conversion Gate02Documento46 páginasFundamentalanalysis 150227053710 Conversion Gate02Meera SeshannaAinda não há avaliações

- Exide Industries (EXIIND) : Finally, Margins Surprise "Positively"Documento1 páginaExide Industries (EXIIND) : Finally, Margins Surprise "Positively"prince1900Ainda não há avaliações

- Basis Points Fixed Income StrategyDocumento11 páginasBasis Points Fixed Income StrategyPhilip LeonardAinda não há avaliações

- India - A Land of Many (Re) Turns: EquitiesDocumento2 páginasIndia - A Land of Many (Re) Turns: EquitiesSaad AliAinda não há avaliações

- Asian Year Ahead 2014Documento562 páginasAsian Year Ahead 2014DivakCT100% (1)

- Management Assignment........... 1Documento38 páginasManagement Assignment........... 1Muhammad MubashirAinda não há avaliações

- Guide to Management Accounting CCC (Cash Conversion Cycle) for ManagersNo EverandGuide to Management Accounting CCC (Cash Conversion Cycle) for ManagersAinda não há avaliações

- Guide to Management Accounting CCC for managers-Cash Conversion Cycle_2020 EditionNo EverandGuide to Management Accounting CCC for managers-Cash Conversion Cycle_2020 EditionAinda não há avaliações

- Guide to Management Accounting CCC for managers 2020 EditionNo EverandGuide to Management Accounting CCC for managers 2020 EditionAinda não há avaliações

- Economic UpdateDocumento2 páginasEconomic UpdateiosalcedoAinda não há avaliações

- Empower June 2012Documento68 páginasEmpower June 2012pravin963Ainda não há avaliações

- RBI Monetary Policy ReviewDocumento4 páginasRBI Monetary Policy ReviewAngel BrokingAinda não há avaliações

- Third Quarter 2016 Investment Outlook: Asset Class SectorDocumento6 páginasThird Quarter 2016 Investment Outlook: Asset Class SectorAnonymous DJrec2Ainda não há avaliações

- ICICI KotakDocumento4 páginasICICI KotakwowcoolmeAinda não há avaliações

- JANUARY 2016: Bond FundDocumento2 páginasJANUARY 2016: Bond FundFaiq FuatAinda não há avaliações

- Situation Index Handbook 2014Documento43 páginasSituation Index Handbook 2014kcousinsAinda não há avaliações

- Financial Depth - The Rand's Hidden AssetDocumento3 páginasFinancial Depth - The Rand's Hidden AssetkcousinsAinda não há avaliações

- The True Risk StoryDocumento25 páginasThe True Risk StorykcousinsAinda não há avaliações

- Financial Instability Hypothesis - MinskyDocumento10 páginasFinancial Instability Hypothesis - MinskyCervino InstituteAinda não há avaliações

- Japanese Bonds Move 2013 05Documento2 páginasJapanese Bonds Move 2013 05kcousinsAinda não há avaliações

- Chart Review - Can We Rotate Back To EM? Macro Economic Research May 2013Documento4 páginasChart Review - Can We Rotate Back To EM? Macro Economic Research May 2013kcousinsAinda não há avaliações

- 2011-02-28 Brait Multi Strategy Fund OverviewDocumento2 páginas2011-02-28 Brait Multi Strategy Fund OverviewkcousinsAinda não há avaliações

- 2011-07-31 Brait Multi StrategyDocumento2 páginas2011-07-31 Brait Multi StrategykcousinsAinda não há avaliações

- Double Dip 2010 05Documento3 páginasDouble Dip 2010 05kcousinsAinda não há avaliações

- Tim Bond v. Hugh Hendry 2009 08Documento15 páginasTim Bond v. Hugh Hendry 2009 08kcousinsAinda não há avaliações

- Brait Multi Strategy Fund Overview October 2010Documento2 páginasBrait Multi Strategy Fund Overview October 2010kcousinsAinda não há avaliações

- Brait Multi Strategy Fund Overview 30 August 2009Documento13 páginasBrait Multi Strategy Fund Overview 30 August 2009kcousinsAinda não há avaliações

- Arm Wrestling in Commodities 2009 10Documento3 páginasArm Wrestling in Commodities 2009 10kcousinsAinda não há avaliações

- Forgotten Commies 2007 07Documento9 páginasForgotten Commies 2007 07kcousinsAinda não há avaliações

- Adam Khoo - Get Out of The Rat RaceDocumento17 páginasAdam Khoo - Get Out of The Rat RaceRian Kurniawan100% (2)

- 9708 s09 QP 1Documento12 páginas9708 s09 QP 1roukaiya_peerkhanAinda não há avaliações

- A Study On Dividend Policy FinalDocumento111 páginasA Study On Dividend Policy FinalrahulAinda não há avaliações

- TDS Vendor AgreementDocumento2 páginasTDS Vendor AgreementScott Dauenhauer, CFP, MSFP, AIFAinda não há avaliações

- Investment Decision Under Conditions of UncertainityDocumento15 páginasInvestment Decision Under Conditions of UncertainityjassubharathiAinda não há avaliações

- PC1 Edible Oil FinalDocumento37 páginasPC1 Edible Oil FinalFarhat DurraniAinda não há avaliações

- Common-Size Financial StatementsDocumento16 páginasCommon-Size Financial StatementsApril IsidroAinda não há avaliações

- C+ F P N F+PDocumento6 páginasC+ F P N F+PIfka HassanAinda não há avaliações

- Accounting For Non AccountantsDocumento66 páginasAccounting For Non AccountantsPrinceAndre100% (2)

- Monopoly Market StructureDocumento17 páginasMonopoly Market StructureMeet PasariAinda não há avaliações

- Safal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetDocumento24 páginasSafal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetVIGNESH RKAinda não há avaliações

- McdonaldsDocumento77 páginasMcdonaldsaster5262100% (1)

- Romney Ais13 PPT 15Documento8 páginasRomney Ais13 PPT 15Sone VipgdAinda não há avaliações

- Overview of Financial Reporting, Financial Statement Analysis, and ValuationDocumento32 páginasOverview of Financial Reporting, Financial Statement Analysis, and ValuationVũ Việt Vân AnhAinda não há avaliações

- Assignment On Principles of Management: Mainul IslamDocumento6 páginasAssignment On Principles of Management: Mainul IslamAmirAinda não há avaliações

- Health Insurance Domain Basics PDFDocumento47 páginasHealth Insurance Domain Basics PDFGautam Kumar DwivedyAinda não há avaliações

- 04 Sample PaperDocumento45 páginas04 Sample Papergaming loverAinda não há avaliações

- 1tunliq5px-N5t0oqa9qlru Uadaqs5 WDocumento56 páginas1tunliq5px-N5t0oqa9qlru Uadaqs5 WDayanandhi ElangovanAinda não há avaliações

- Variable Pay and Executive Compensation Variable Pay and Executive CompensationDocumento27 páginasVariable Pay and Executive Compensation Variable Pay and Executive CompensationHimaKumariAinda não há avaliações

- Transaction Cycles - Test of Controls and Substantive Tests of TransactionsDocumento9 páginasTransaction Cycles - Test of Controls and Substantive Tests of TransactionsfeAinda não há avaliações

- Times Interest Earned Ratio: Compare Interest Payments With Income Available To Pay ThemDocumento13 páginasTimes Interest Earned Ratio: Compare Interest Payments With Income Available To Pay Themfrank_grimesAinda não há avaliações

- Revenue Memorandum Order No. 22-2007: SUBJECT: Prescribing Additional Procedures in The Audit of Input TaxesDocumento2 páginasRevenue Memorandum Order No. 22-2007: SUBJECT: Prescribing Additional Procedures in The Audit of Input Taxesjames luzonAinda não há avaliações

- SheDocumento2 páginasSheRhozeiah LeiahAinda não há avaliações

- Decision Making .PPT 4th Sem McomDocumento16 páginasDecision Making .PPT 4th Sem Mcomnousheen rehmanAinda não há avaliações

- Asl Energy Pte KFT - 1Documento5 páginasAsl Energy Pte KFT - 1Ibra RizkiAinda não há avaliações