Você também pode gostar

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Micronet TMRDocumento316 páginasMicronet TMRHaithem BrebishAinda não há avaliações

- The Consulting Industry and Its Transformations in WordDocumento23 páginasThe Consulting Industry and Its Transformations in Wordlei ann magnayeAinda não há avaliações

- Basler Electric TCCDocumento7 páginasBasler Electric TCCGalih Trisna NugrahaAinda não há avaliações

- Credit Risk ManagementDocumento64 páginasCredit Risk Managementcherry_nu100% (12)

- Multi Core Architectures and ProgrammingDocumento10 páginasMulti Core Architectures and ProgrammingRIYA GUPTAAinda não há avaliações

- HUAWEI PowerCube 500Documento41 páginasHUAWEI PowerCube 500soumen95Ainda não há avaliações

- Notice To The MarketDocumento1 páginaNotice To The MarketJBS RIAinda não há avaliações

- Release and FS 1Q17Documento53 páginasRelease and FS 1Q17JBS RIAinda não há avaliações

- Notice To The MarketDocumento1 páginaNotice To The MarketJBS RIAinda não há avaliações

- 1Q17 Conference Call TranscriptDocumento13 páginas1Q17 Conference Call TranscriptJBS RIAinda não há avaliações

- 1Q17 Financial StatementsDocumento31 páginas1Q17 Financial StatementsJBS RIAinda não há avaliações

- Notice To The MarketDocumento1 páginaNotice To The MarketJBS RIAinda não há avaliações

- Minutes of The Board of Directors' Meeting Held On May 08, 2017Documento2 páginasMinutes of The Board of Directors' Meeting Held On May 08, 2017JBS RIAinda não há avaliações

- 1Q17 Earnings PresentationDocumento15 páginas1Q17 Earnings PresentationJBS RIAinda não há avaliações

- JBS - Annual and Sustainability Report 2016Documento144 páginasJBS - Annual and Sustainability Report 2016JBS RIAinda não há avaliações

- JBS S.A. Releases Its 2016 Annual and Sustainability ReportDocumento1 páginaJBS S.A. Releases Its 2016 Annual and Sustainability ReportJBS RIAinda não há avaliações

- Minutes of The Fiscal Council's Meeting Held On May 04, 2017Documento2 páginasMinutes of The Fiscal Council's Meeting Held On May 04, 2017JBS RIAinda não há avaliações

- Minutes of The Board of Directors' Meeting Held On May 05, 2017Documento2 páginasMinutes of The Board of Directors' Meeting Held On May 05, 2017JBS RIAinda não há avaliações

- Minutes of The Fiscal Council's Meeting Held On April 05, 2017Documento5 páginasMinutes of The Fiscal Council's Meeting Held On April 05, 2017JBS RIAinda não há avaliações

- JBS S.A. Announces The Conclusion of Plumrose AcquisitionDocumento1 páginaJBS S.A. Announces The Conclusion of Plumrose AcquisitionJBS RIAinda não há avaliações

- Minutes of The Board of Directors' Meeting Held On March 13, 2017Documento4 páginasMinutes of The Board of Directors' Meeting Held On March 13, 2017JBS RIAinda não há avaliações

- JBS Institutional Presentation Including 4Q16 and 2016 ResultsDocumento24 páginasJBS Institutional Presentation Including 4Q16 and 2016 ResultsJBS RIAinda não há avaliações

- MGMT Report FS 2015 (Reap 2017)Documento95 páginasMGMT Report FS 2015 (Reap 2017)JBS RIAinda não há avaliações

- JBS - ARCA - 2017 04 06 - Aprovao Reapresentao DFs 2015 e 2016 (JUCESP) EngDocumento5 páginasJBS - ARCA - 2017 04 06 - Aprovao Reapresentao DFs 2015 e 2016 (JUCESP) EngJBS RIAinda não há avaliações

- MGMT Report FS 2016 (Reap 2017)Documento97 páginasMGMT Report FS 2016 (Reap 2017)JBS RIAinda não há avaliações

- REMOTE VOTING FORM OF OESM To Be Held On April 28, 2017Documento5 páginasREMOTE VOTING FORM OF OESM To Be Held On April 28, 2017JBS RIAinda não há avaliações

- 4Q16 and 2016 Earnings PresentationDocumento21 páginas4Q16 and 2016 Earnings PresentationJBS RIAinda não há avaliações

- 4Q16 Conference Call TranscriptDocumento16 páginas4Q16 Conference Call TranscriptJBS RIAinda não há avaliações

- JBS - ARCF - 2017 03 10 - Aprovao DFs 4T2016 (Livro) MZT EngDocumento4 páginasJBS - ARCF - 2017 03 10 - Aprovao DFs 4T2016 (Livro) MZT EngJBS RIAinda não há avaliações

- MgmtReport FSDocumento96 páginasMgmtReport FSJBS RIAinda não há avaliações

- MATERIAL FACT - JBS Announces The Acquisition of Plumrose USADocumento2 páginasMATERIAL FACT - JBS Announces The Acquisition of Plumrose USAJBS RIAinda não há avaliações

- Notice To The Market - Federal Police OperationDocumento1 páginaNotice To The Market - Federal Police OperationJBS RIAinda não há avaliações

- MgmtReport FSDocumento96 páginasMgmtReport FSJBS RIAinda não há avaliações

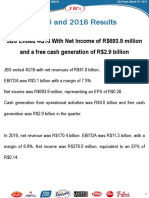

- 4Q16 and 2016 Earnings ReleaseDocumento31 páginas4Q16 and 2016 Earnings ReleaseJBS RI100% (1)

- Minutes of The Board of Directors' Meeting Held On February 23, 2017Documento20 páginasMinutes of The Board of Directors' Meeting Held On February 23, 2017JBS RIAinda não há avaliações

- UntitledDocumento4 páginasUntitledJBS RIAinda não há avaliações

- A Vision System For Surface Roughness Characterization Using The Gray Level Co-Occurrence MatrixDocumento12 páginasA Vision System For Surface Roughness Characterization Using The Gray Level Co-Occurrence MatrixPraveen KumarAinda não há avaliações

- B2B Marketing: Chapter-8Documento23 páginasB2B Marketing: Chapter-8Saurabh JainAinda não há avaliações

- Regulated and Non Regulated BodiesDocumento28 páginasRegulated and Non Regulated Bodiesnivea rajAinda não há avaliações

- TOR AND SCOPING Presentation SlidesDocumento23 páginasTOR AND SCOPING Presentation SlidesSRESTAA BHATTARAIAinda não há avaliações

- Mtech Vlsi Lab ManualDocumento38 páginasMtech Vlsi Lab ManualRajesh Aaitha100% (2)

- Laporan Keuangan TRIN Per Juni 2023-FinalDocumento123 páginasLaporan Keuangan TRIN Per Juni 2023-FinalAdit RamdhaniAinda não há avaliações

- Silk Road Ensemble in Chapel HillDocumento1 páginaSilk Road Ensemble in Chapel HillEmil KangAinda não há avaliações

- Portfolio Write-UpDocumento4 páginasPortfolio Write-UpJonFromingsAinda não há avaliações

- Presentation No. 3 - Songs and ChantsDocumento44 páginasPresentation No. 3 - Songs and Chantsandie hinchAinda não há avaliações

- Vignyapan 18-04-2024Documento16 páginasVignyapan 18-04-2024adil1787Ainda não há avaliações

- Hydropneumatic Booster Set MFDocumento5 páginasHydropneumatic Booster Set MFdonchakdeAinda não há avaliações

- Lit 30Documento2 páginasLit 30ReemAlashhab81Ainda não há avaliações

- Letter of Acceptfor TDocumento3 páginasLetter of Acceptfor TCCSAinda não há avaliações

- 12 Constructor and DistructorDocumento15 páginas12 Constructor and DistructorJatin BhasinAinda não há avaliações

- Introduction To History AnswerDocumento3 páginasIntroduction To History AnswerLawrence De La RosaAinda não há avaliações

- PC's & Laptop Accessories PDFDocumento4 páginasPC's & Laptop Accessories PDFsundar chapagainAinda não há avaliações

- Bahan Ajar Application LetterDocumento14 páginasBahan Ajar Application LetterNevada Setya BudiAinda não há avaliações

- Ladies Code I'm Fine Thank YouDocumento2 páginasLadies Code I'm Fine Thank YoubobbybiswaggerAinda não há avaliações

- Tanque: Equipment Data SheetDocumento1 páginaTanque: Equipment Data SheetAlonso DIAZAinda não há avaliações

- AT10 Meat Tech 1Documento20 páginasAT10 Meat Tech 1Reubal Jr Orquin Reynaldo100% (1)

- Straw Bale ConstructionDocumento37 páginasStraw Bale ConstructionelissiumAinda não há avaliações

- GT I9100g Service SchematicsDocumento8 páginasGT I9100g Service SchematicsMassolo RoyAinda não há avaliações

- DS SX1280-1-2 V3.0Documento143 páginasDS SX1280-1-2 V3.0bkzzAinda não há avaliações

- Technical and Business WritingDocumento3 páginasTechnical and Business WritingMuhammad FaisalAinda não há avaliações