Você também pode gostar

- Ev Charging Inverter Brochure NamDocumento4 páginasEv Charging Inverter Brochure NamOmar ElshahatAinda não há avaliações

- 101 - Syllabus Fall 2016Documento7 páginas101 - Syllabus Fall 2016Omar ElshahatAinda não há avaliações

- Sbordo - Beauty Rediscovers The Male BodyDocumento17 páginasSbordo - Beauty Rediscovers The Male BodyOmar ElshahatAinda não há avaliações

- Highway & Traffic Engineering: Steven Rames, PEDocumento17 páginasHighway & Traffic Engineering: Steven Rames, PEOmar ElshahatAinda não há avaliações

- The First Major Cable Stayed Bridge in Egypt and The Middle East, and The Highest Cable Stayed Bridge in The WorldDocumento1 páginaThe First Major Cable Stayed Bridge in Egypt and The Middle East, and The Highest Cable Stayed Bridge in The WorldOmar ElshahatAinda não há avaliações

- Lecture 15: Double Integrals: SF HK N L FHK N L-Fh0LDocumento2 páginasLecture 15: Double Integrals: SF HK N L FHK N L-Fh0LOmar ElshahatAinda não há avaliações

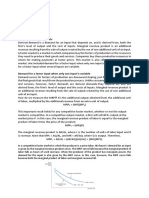

- DR Emad Economics Ex1Documento1 páginaDR Emad Economics Ex1Omar ElshahatAinda não há avaliações

- Thermal Physics 1 - Specific Heat CapacityDocumento14 páginasThermal Physics 1 - Specific Heat CapacityOmar ElshahatAinda não há avaliações

- 1 Course Offering Fall2012coDocumento5 páginas1 Course Offering Fall2012coOmar ElshahatAinda não há avaliações

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Unit 5 - ElasticityDocumento47 páginasUnit 5 - ElasticityMilagra MukwamboAinda não há avaliações

- Assignment 2 - Micro1Documento8 páginasAssignment 2 - Micro1Teak Tattee0% (1)

- AM2 FTU Official 2022 DEC 1Documento87 páginasAM2 FTU Official 2022 DEC 1quỳnh nguyễnAinda não há avaliações

- Microeconomics Theory and Applications With Calculus 3rd Edition Perloff Test BankDocumento19 páginasMicroeconomics Theory and Applications With Calculus 3rd Edition Perloff Test Banksiphilisdysluite7xrxc100% (24)

- CHAPTER 4 Demand and SupplyDocumento12 páginasCHAPTER 4 Demand and SupplyLorenzo Taguinod EsparasAinda não há avaliações

- Practice w2 MCTDocumento16 páginasPractice w2 MCTYuki TanAinda não há avaliações

- Chapter 2 Economics - ReviewDocumento5 páginasChapter 2 Economics - ReviewHằng LêAinda não há avaliações

- Managerial Economics - NotesDocumento35 páginasManagerial Economics - NotesShivaprasad NageshAinda não há avaliações

- PM Exercise Solutions Session 1-6 CH 2-10Documento47 páginasPM Exercise Solutions Session 1-6 CH 2-10sxywangAinda não há avaliações

- Labor Economics ManualDocumento97 páginasLabor Economics ManualLam Wai Kuen100% (3)

- 03 - Prob Set - SS and DDDocumento7 páginas03 - Prob Set - SS and DDIshmamAinda não há avaliações

- Economics Tutor Guide Grade 12 (1) - 1Documento25 páginasEconomics Tutor Guide Grade 12 (1) - 1Tshegofatso JacksonAinda não há avaliações

- BL Econ 6142 Lec 1933T Managerial EconomicsDocumento9 páginasBL Econ 6142 Lec 1933T Managerial EconomicsJamie Balisi100% (1)

- Epple, D. & McCallum, B. (2006) - Simultaneous Equation Econometrics The Missing ExampleDocumento28 páginasEpple, D. & McCallum, B. (2006) - Simultaneous Equation Econometrics The Missing ExampleJoselyn SharonAinda não há avaliações

- Managerial Economics - BY Sonia Singh: Amity Business SchoolDocumento27 páginasManagerial Economics - BY Sonia Singh: Amity Business SchoolAparna MongaAinda não há avaliações

- Chapter - 22 Federal SystemDocumento7 páginasChapter - 22 Federal SystemHeap Ke XinAinda não há avaliações

- Chapter 5: (Elasticity and Its Application) Section ADocumento7 páginasChapter 5: (Elasticity and Its Application) Section APhạm Huy100% (1)

- Economics DemandDocumento5 páginasEconomics DemandMuhammad Tariq100% (2)

- Module 5&6 - Linear Demand Function and Supply Function (Application) - Part 2Documento10 páginasModule 5&6 - Linear Demand Function and Supply Function (Application) - Part 2Danica Ann B. TanguilanAinda não há avaliações

- Theory of Demand - 1Documento32 páginasTheory of Demand - 1hiriiiitii100% (2)

- Economics AssignmentDocumento6 páginasEconomics AssignmentNsh JshAinda não há avaliações

- Economics 7th Edition Hubbard Solutions ManualDocumento25 páginasEconomics 7th Edition Hubbard Solutions ManualKristinRichardsygci100% (61)

- PS2 SolutionsDocumento9 páginasPS2 SolutionsRyan Ma100% (1)

- Markets For Factor Inputs PDFDocumento14 páginasMarkets For Factor Inputs PDFJennifer CarliseAinda não há avaliações

- Applied Economics: Application of Supply and DemandDocumento24 páginasApplied Economics: Application of Supply and DemandCASTOR Z CMNHSAinda não há avaliações

- Economics Demand SupplyDocumento6 páginasEconomics Demand SupplykhurramAinda não há avaliações

- LN03 Keat020827 07 Me LN03Documento43 páginasLN03 Keat020827 07 Me LN03DRIP HARDLYAinda não há avaliações

- Micro Quiz 2Documento7 páginasMicro Quiz 2Gia Han TranAinda não há avaliações

- Market DemandDocumento18 páginasMarket DemandOlusholaAinda não há avaliações