Você também pode gostar

- Weaponization Committee: HOW A "CYBERSECURITY" AGENCY COLLUDED WITH BIG TECH AND "DISINFORMATION" PARTNERS TO CENSOR AMERICANSDocumento37 páginasWeaponization Committee: HOW A "CYBERSECURITY" AGENCY COLLUDED WITH BIG TECH AND "DISINFORMATION" PARTNERS TO CENSOR AMERICANSJim Hoft100% (2)

- China and the US Foreign Debt Crisis: Does China Own the USA?No EverandChina and the US Foreign Debt Crisis: Does China Own the USA?Ainda não há avaliações

- Fifth Circuit Decision Against FDA in Apter CaseDocumento24 páginasFifth Circuit Decision Against FDA in Apter CaseAssociation of American Physicians and Surgeons100% (1)

- German Specification BGR181 (English Version) - Acceptance Criteria For Floorings R Rating As Per DIN 51130Documento26 páginasGerman Specification BGR181 (English Version) - Acceptance Criteria For Floorings R Rating As Per DIN 51130Ankur Singh ANULAB100% (2)

- Budget of the U.S. Government: A New Foundation for American Greatness: Fiscal Year 2018No EverandBudget of the U.S. Government: A New Foundation for American Greatness: Fiscal Year 2018Ainda não há avaliações

- KhanIzh - FGI Life - Offer Letter - V1 - Signed - 20220113154558Documento6 páginasKhanIzh - FGI Life - Offer Letter - V1 - Signed - 20220113154558Izharul HaqueAinda não há avaliações

- Ainsworth, The One-Year-Old Task of The Strange SituationDocumento20 páginasAinsworth, The One-Year-Old Task of The Strange SituationliliaAinda não há avaliações

- Understanding California's Fiscal Recovery: Primary Credit AnalystDocumento6 páginasUnderstanding California's Fiscal Recovery: Primary Credit Analystapi-227433089Ainda não há avaliações

- NY CashflowcrunchDocumento8 páginasNY CashflowcrunchZerohedgeAinda não há avaliações

- California's Fiscal Outlook: The 2011-12 BudgetDocumento45 páginasCalifornia's Fiscal Outlook: The 2011-12 BudgetRichard Costigan IIIAinda não há avaliações

- The FY2011 Federal BudgetDocumento24 páginasThe FY2011 Federal BudgetromulusxAinda não há avaliações

- OND Choeneck ING PLLC: MemorandumDocumento17 páginasOND Choeneck ING PLLC: MemorandumrkarlinAinda não há avaliações

- Implications For New York State of A Federal Government ShutdownDocumento4 páginasImplications For New York State of A Federal Government ShutdownElizabeth BenjaminAinda não há avaliações

- 2011 Quick StartDocumento24 páginas2011 Quick StartNick ReismanAinda não há avaliações

- New York State: Financial Plan For Fiscal Year 2012 First Quarterly UpdateDocumento28 páginasNew York State: Financial Plan For Fiscal Year 2012 First Quarterly UpdateNick ReismanAinda não há avaliações

- Usa Debt Crisis Republicans ViewDocumento6 páginasUsa Debt Crisis Republicans ViewAmit Kumar RoyAinda não há avaliações

- Enacted Budget Report 2020-21Documento22 páginasEnacted Budget Report 2020-21Luke ParsnowAinda não há avaliações

- The Debt Limit: History and Recent Increases: D. Andrew AustinDocumento27 páginasThe Debt Limit: History and Recent Increases: D. Andrew AustinGaryAinda não há avaliações

- Budget Response FY 2012 FINALDocumento17 páginasBudget Response FY 2012 FINALCeleste KatzAinda não há avaliações

- Nys Go Report 1109Documento5 páginasNys Go Report 1109jspectorAinda não há avaliações

- New York's Deficit Shuffle: April 2010Documento23 páginasNew York's Deficit Shuffle: April 2010Casey SeilerAinda não há avaliações

- Tentative Budget - Final Friday Nov 12 RevDocumento111 páginasTentative Budget - Final Friday Nov 12 RevAlfonso RobinsonAinda não há avaliações

- Budget Law SonDocumento16 páginasBudget Law SonObrabotka FotografiyAinda não há avaliações

- Research DocumentDocumento4 páginasResearch DocumentRachel E. Stassen-BergerAinda não há avaliações

- Focus Colorado: Economic and Revenue Forecast: Colorado Legislative Council Staff Economics Section September 20, 2010Documento72 páginasFocus Colorado: Economic and Revenue Forecast: Colorado Legislative Council Staff Economics Section September 20, 2010Circuit MediaAinda não há avaliações

- Extending The State Fiscal Relief Provisions of The American Recovery and Reinvestment Act (ARRA)Documento8 páginasExtending The State Fiscal Relief Provisions of The American Recovery and Reinvestment Act (ARRA)Public Policy and Education Fund of NYAinda não há avaliações

- Attacking The Fiscal Crisis - What The States Have Taught Us About The Way ForwardDocumento7 páginasAttacking The Fiscal Crisis - What The States Have Taught Us About The Way ForwardDamian PanaitescuAinda não há avaliações

- Solomon Island: Letter of Intent, Memorandum of Economic andDocumento19 páginasSolomon Island: Letter of Intent, Memorandum of Economic andkurukuru12Ainda não há avaliações

- Distribution of Spending: Why Study Public Finance?Documento1 páginaDistribution of Spending: Why Study Public Finance?penelopegerhardAinda não há avaliações

- Commission of Inquiry Report 4 - 4Documento8 páginasCommission of Inquiry Report 4 - 4michael_olson6605Ainda não há avaliações

- Chicag o Fed Letter: How Much Debt Does The U.S. Government Owe?Documento4 páginasChicag o Fed Letter: How Much Debt Does The U.S. Government Owe?TBP_Think_TankAinda não há avaliações

- Current Status of The State Fiscal Year 2010-11 Budget: Executive SummaryDocumento8 páginasCurrent Status of The State Fiscal Year 2010-11 Budget: Executive SummaryrkarlinAinda não há avaliações

- 2008 GAO Audit ReportDocumento24 páginas2008 GAO Audit ReportkaligelisAinda não há avaliações

- Finance AccountsDocumento5 páginasFinance Accountsravi yadavaAinda não há avaliações

- A DECADE OF SQUANDERED OPPORTUNITY by JM MinorDocumento55 páginasA DECADE OF SQUANDERED OPPORTUNITY by JM MinorDesmond Sullivan100% (1)

- 2016 17 Enacted Budget FinplanDocumento47 páginas2016 17 Enacted Budget FinplanMatthew HamiltonAinda não há avaliações

- Report On The State Fiscal Year 2014 - 15 Enacted Budget Financial Plan and The Capital Program and Financing PlanDocumento37 páginasReport On The State Fiscal Year 2014 - 15 Enacted Budget Financial Plan and The Capital Program and Financing PlanRick KarlinAinda não há avaliações

- Budget Overview 2014Documento44 páginasBudget Overview 2014Juan FordAinda não há avaliações

- List of Statements in Finance Account: Volume-I: Summarised Statements 1 2Documento8 páginasList of Statements in Finance Account: Volume-I: Summarised Statements 1 2ARAVIND KAinda não há avaliações

- The $21 Billion State Budget: South Carolina's Three Spending CategoriesDocumento25 páginasThe $21 Billion State Budget: South Carolina's Three Spending CategoriesSteve CouncilAinda não há avaliações

- El2010 20Documento4 páginasEl2010 20arborjimbAinda não há avaliações

- Debt Limit Analysis: AU GUST 2017Documento63 páginasDebt Limit Analysis: AU GUST 2017National Press FoundationAinda não há avaliações

- Governor Withholding ReportDocumento4 páginasGovernor Withholding ReportColumbia Daily TribuneAinda não há avaliações

- 13 TH FC MemorandumDocumento141 páginas13 TH FC Memorandumatikbarbhuiya1432Ainda não há avaliações

- 2014-15 Financial Plan Enacted BudgetDocumento37 páginas2014-15 Financial Plan Enacted BudgetjspectorAinda não há avaliações

- Office of The State Comptroller: Executive SummaryDocumento5 páginasOffice of The State Comptroller: Executive SummaryCeleste KatzAinda não há avaliações

- Sovereigns: U.S. Public Finances - Overview and OutlookDocumento15 páginasSovereigns: U.S. Public Finances - Overview and OutlookchanduAinda não há avaliações

- Macroeconomics Effects of Structural Fiscal Policy Changes in ColombiaDocumento44 páginasMacroeconomics Effects of Structural Fiscal Policy Changes in ColombiaAndres ZapataAinda não há avaliações

- Do Budget Deficits Cause in Ation?: by Keith SillDocumento8 páginasDo Budget Deficits Cause in Ation?: by Keith SillluminaAinda não há avaliações

- Timing The US Melt Down and RebirthDocumento10 páginasTiming The US Melt Down and RebirthchartcruzerAinda não há avaliações

- State Budget Shortfalls 2010Documento10 páginasState Budget Shortfalls 2010Nathan MartinAinda não há avaliações

- Quick Start Report - 2011-12 - Final 11.5.10Documento50 páginasQuick Start Report - 2011-12 - Final 11.5.10New York SenateAinda não há avaliações

- 2010 Albany BudgetDocumento187 páginas2010 Albany BudgettulocalpoliticsAinda não há avaliações

- 2016 17 Enacted Budget Report PDFDocumento74 páginas2016 17 Enacted Budget Report PDFNick ReismanAinda não há avaliações

- Federal DebtDocumento14 páginasFederal Debtabhimehta90Ainda não há avaliações

- 3rd World CrisisDocumento7 páginas3rd World CrisisD Attitude KidAinda não há avaliações

- Comentario PR Breckinridge Marzo 2012 NotiCelDocumento6 páginasComentario PR Breckinridge Marzo 2012 NotiCelnoticelmesaAinda não há avaliações

- 2011 EUA Crise Teto Da DívidaDocumento12 páginas2011 EUA Crise Teto Da DívidaGabriel LaguerraAinda não há avaliações

- Measures To Enhance Zimbabwe's SpaceDocumento26 páginasMeasures To Enhance Zimbabwe's SpaceBhea BañezAinda não há avaliações

- Macro 7Documento12 páginasMacro 7Àlex SolàAinda não há avaliações

- HIM2016Q3NPDocumento7 páginasHIM2016Q3NPlovehonor0519Ainda não há avaliações

- DC Cuts: How the Federal Budget Went from a Surplus to a Trillion Dollar Deficit in 10 YearsNo EverandDC Cuts: How the Federal Budget Went from a Surplus to a Trillion Dollar Deficit in 10 YearsAinda não há avaliações

- Reynolds Public Health Proclamation - 2020.04.06Documento5 páginasReynolds Public Health Proclamation - 2020.04.06Shane Vander HartAinda não há avaliações

- USD TLGP MaturitiesDocumento1 páginaUSD TLGP MaturitiesCreditTraderAinda não há avaliações

- IG Fundamentals Q22010Documento1 páginaIG Fundamentals Q22010CreditTraderAinda não há avaliações

- SPX Now and ThenDocumento1 páginaSPX Now and ThenCreditTraderAinda não há avaliações

- Credit ContractionDocumento1 páginaCredit ContractionCreditTraderAinda não há avaliações

- IG-HY Vs Stocks Relative-ValueDocumento1 páginaIG-HY Vs Stocks Relative-ValueCreditTraderAinda não há avaliações

- HY-IG Vs StocksDocumento1 páginaHY-IG Vs StocksCreditTraderAinda não há avaliações

- SPL 20101019Documento1 páginaSPL 20101019CreditTraderAinda não há avaliações

- HY Vs IG DurationDocumento1 páginaHY Vs IG DurationCreditTraderAinda não há avaliações

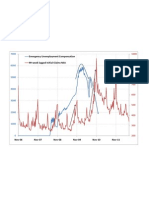

- EUC and 99-Week-Lagged Initial ClaimsDocumento1 páginaEUC and 99-Week-Lagged Initial ClaimsCreditTraderAinda não há avaliações

- CDR Csa 201007Documento1 páginaCDR Csa 201007CreditTraderAinda não há avaliações

- IG Over TSYDocumento1 páginaIG Over TSYCreditTraderAinda não há avaliações

- HY-IG Vs EquityDocumento1 páginaHY-IG Vs EquityCreditTraderAinda não há avaliações

- EUR Vs GDP-Weighted CDSDocumento1 páginaEUR Vs GDP-Weighted CDSCreditTraderAinda não há avaliações

- C&I Loans + ABCP - Aggregate CreditDocumento1 páginaC&I Loans + ABCP - Aggregate CreditCreditTraderAinda não há avaliações

- CDR Csa Aug2010Documento1 páginaCDR Csa Aug2010CreditTraderAinda não há avaliações

- CDR Csa Scatter Aug10Documento1 páginaCDR Csa Scatter Aug10CreditTraderAinda não há avaliações

- FSB30 IntrinsicsDocumento1 páginaFSB30 IntrinsicsCreditTraderAinda não há avaliações

- IG Range CompressionDocumento1 páginaIG Range CompressionCreditTraderAinda não há avaliações

- CDR Csa 20100813Documento1 páginaCDR Csa 20100813CreditTraderAinda não há avaliações

- IG Weekly RangeDocumento1 páginaIG Weekly RangeCreditTraderAinda não há avaliações

- Exchange Rate Regime Analysis For The Chinese YuanDocumento10 páginasExchange Rate Regime Analysis For The Chinese YuanCreditTraderAinda não há avaliações

- Spread Leverage ComparisonDocumento1 páginaSpread Leverage ComparisonCreditTraderAinda não há avaliações

- CDR Csa 20100716Documento1 páginaCDR Csa 20100716CreditTraderAinda não há avaliações

- IG Vs TSY CycleDocumento1 páginaIG Vs TSY CycleCreditTraderAinda não há avaliações

- JUN Roll by SectorDocumento1 páginaJUN Roll by SectorCreditTraderAinda não há avaliações

- Implied CorrelationDocumento1 páginaImplied CorrelationCreditTraderAinda não há avaliações

- Espiritualidad AFPP - 2018 PDFDocumento5 páginasEspiritualidad AFPP - 2018 PDFEsteban OrellanaAinda não há avaliações

- Final Manuscript GROUP2Documento102 páginasFinal Manuscript GROUP222102279Ainda não há avaliações

- Umur Ekonomis Mesin RevDocumento3 páginasUmur Ekonomis Mesin Revrazali akhmadAinda não há avaliações

- Qi Gong & Meditation - Shaolin Temple UKDocumento5 páginasQi Gong & Meditation - Shaolin Temple UKBhuvnesh TenguriaAinda não há avaliações

- Posi LokDocumento24 páginasPosi LokMarcel Baque100% (1)

- DSM-5 Personality Disorders PDFDocumento2 páginasDSM-5 Personality Disorders PDFIqbal Baryar0% (1)

- Buddahism ReportDocumento36 páginasBuddahism Reportlaica andalAinda não há avaliações

- Community Medicine DissertationDocumento7 páginasCommunity Medicine DissertationCollegePaperGhostWriterSterlingHeights100% (1)

- Just Another RantDocumento6 páginasJust Another RantJuan Manuel VargasAinda não há avaliações

- High School Students' Attributions About Success and Failure in Physics.Documento6 páginasHigh School Students' Attributions About Success and Failure in Physics.Zeynep Tuğba KahyaoğluAinda não há avaliações

- W2 - Fundementals of SepDocumento36 páginasW2 - Fundementals of Sephairen jegerAinda não há avaliações

- Environmental Product Declaration: Plasterboard Knauf Diamant GKFIDocumento11 páginasEnvironmental Product Declaration: Plasterboard Knauf Diamant GKFIIoana CAinda não há avaliações

- The Integration of Technology Into Pharmacy Education and PracticeDocumento6 páginasThe Integration of Technology Into Pharmacy Education and PracticeAjit ThoratAinda não há avaliações

- Quality Assurance Kamera GammaDocumento43 páginasQuality Assurance Kamera GammawiendaintanAinda não há avaliações

- Indiana Administrative CodeDocumento176 páginasIndiana Administrative CodeMd Mamunur RashidAinda não há avaliações

- Soal 2-3ADocumento5 páginasSoal 2-3Atrinanda ajiAinda não há avaliações

- Owner'S Manual: Explosion-Proof Motor Mf07, Mf10, Mf13Documento18 páginasOwner'S Manual: Explosion-Proof Motor Mf07, Mf10, Mf13mediacampaigncc24Ainda não há avaliações

- Calculation Condensation StudentDocumento7 páginasCalculation Condensation StudentHans PeterAinda não há avaliações

- CRM McDonalds ScribdDocumento9 páginasCRM McDonalds ScribdArun SanalAinda não há avaliações

- Management of Developing DentitionDocumento51 páginasManagement of Developing Dentitionahmed alshaariAinda não há avaliações

- Product Sheet - Parsys Cloud - Parsys TelemedicineDocumento10 páginasProduct Sheet - Parsys Cloud - Parsys TelemedicineChristian Lezama Cuellar100% (1)

- BARCODESDocumento7 páginasBARCODESChitPerRhosAinda não há avaliações

- FINALE Final Chapter1 PhoebeKatesMDelicanaPR-IIeditedphoebe 1Documento67 páginasFINALE Final Chapter1 PhoebeKatesMDelicanaPR-IIeditedphoebe 1Jane ParkAinda não há avaliações

- Wa0016Documento3 páginasWa0016Vinay DahiyaAinda não há avaliações

- Marine Advisory 03-22 LRITDocumento2 páginasMarine Advisory 03-22 LRITNikos StratisAinda não há avaliações

- Faculty Based Bank Written PDFDocumento85 páginasFaculty Based Bank Written PDFTamim HossainAinda não há avaliações

- 2022.08.09 Rickenbacker ComprehensiveDocumento180 páginas2022.08.09 Rickenbacker ComprehensiveTony WintonAinda não há avaliações