Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- L.V. Prasad Eye Institute: Innovating The Business of Eye CareDocumento9 páginasL.V. Prasad Eye Institute: Innovating The Business of Eye CareFadhila Nurfida HanifAinda não há avaliações

- Wokrplace Safety Bizsafe Audit Preparation Special ReportDocumento8 páginasWokrplace Safety Bizsafe Audit Preparation Special Reportisaych33zeAinda não há avaliações

- Establishing Entrepreneurial SystemsDocumento4 páginasEstablishing Entrepreneurial SystemsVictor Charles100% (2)

- Online Education in India 2021Documento56 páginasOnline Education in India 2021anonymomrAinda não há avaliações

- Second Innings September 2019Documento52 páginasSecond Innings September 2019Prof Dr Chowdari PrasadAinda não há avaliações

- 10 International Conference On Problem and Possibilities in Online Education in ManagementDocumento39 páginas10 International Conference On Problem and Possibilities in Online Education in ManagementProf Dr Chowdari PrasadAinda não há avaliações

- Big Data On B-SchoolsDocumento13 páginasBig Data On B-SchoolsProf Dr Chowdari PrasadAinda não há avaliações

- Digital Banking in India 2016Documento21 páginasDigital Banking in India 2016Prof Dr Chowdari PrasadAinda não há avaliações

- Prof Chowdari Prasad CV 26112018Documento11 páginasProf Chowdari Prasad CV 26112018Prof Dr Chowdari PrasadAinda não há avaliações

- Banking Innovation & Green ManagementDocumento24 páginasBanking Innovation & Green ManagementProf Dr Chowdari PrasadAinda não há avaliações

- Social Entrepreneurship2015Documento45 páginasSocial Entrepreneurship2015Prof Dr Chowdari PrasadAinda não há avaliações

- E-Governance in Karnataka"Documento20 páginasE-Governance in Karnataka"Prof Dr Chowdari PrasadAinda não há avaliações

- A Strategy To Connect The Dots For A Big Picture of Indian B-SchoolsDocumento15 páginasA Strategy To Connect The Dots For A Big Picture of Indian B-SchoolsProf Dr Chowdari PrasadAinda não há avaliações

- B-Schools in India and Big Data 2016Documento14 páginasB-Schools in India and Big Data 2016Prof Dr Chowdari PrasadAinda não há avaliações

- Digital Banking in India 2016Documento21 páginasDigital Banking in India 2016Prof Dr Chowdari Prasad100% (3)

- Consumer Protection Act 1986Documento41 páginasConsumer Protection Act 1986Prof Dr Chowdari Prasad100% (1)

- Performance of Crowd Funding in India: Issues and ChallengesDocumento19 páginasPerformance of Crowd Funding in India: Issues and ChallengesProf Dr Chowdari Prasad100% (1)

- Digital Banking Paper IFIM 05022016Documento36 páginasDigital Banking Paper IFIM 05022016Prof Dr Chowdari PrasadAinda não há avaliações

- Seshadripuram Conference Mar.2014 Higher Education: Autonomy Full PaperDocumento14 páginasSeshadripuram Conference Mar.2014 Higher Education: Autonomy Full PaperProf Dr Chowdari PrasadAinda não há avaliações

- Social Entrepreneurship2015Documento45 páginasSocial Entrepreneurship2015Prof Dr Chowdari PrasadAinda não há avaliações

- HR As A Strategic Business PartnerDocumento36 páginasHR As A Strategic Business PartnerProf Dr Chowdari PrasadAinda não há avaliações

- Leaders vs. ManagersDocumento39 páginasLeaders vs. ManagersProf Dr Chowdari PrasadAinda não há avaliações

- Recent Trends of PE Funding in IndiaDocumento38 páginasRecent Trends of PE Funding in IndiaProf Dr Chowdari PrasadAinda não há avaliações

- Tapmi Update 2013Documento120 páginasTapmi Update 2013Prof Dr Chowdari PrasadAinda não há avaliações

- Workshop On BFSI in India at MTL Manipal 10012014Documento56 páginasWorkshop On BFSI in India at MTL Manipal 10012014Prof Dr Chowdari PrasadAinda não há avaliações

- Recent Trends of PE Funding in India 2013Documento9 páginasRecent Trends of PE Funding in India 2013Prof Dr Chowdari PrasadAinda não há avaliações

- FDP On EntrepreneurshipDocumento17 páginasFDP On EntrepreneurshipProf Dr Chowdari PrasadAinda não há avaliações

- Sbi LD 27012012Documento60 páginasSbi LD 27012012Prof Dr Chowdari PrasadAinda não há avaliações

- Lean and Green Banking in India 2012Documento20 páginasLean and Green Banking in India 2012Prof Dr Chowdari Prasad100% (2)

- Types of EntreprneursDocumento45 páginasTypes of EntreprneursProf Dr Chowdari PrasadAinda não há avaliações

- Profile of Banks 2010-11Documento99 páginasProfile of Banks 2010-11Vishesh KumarAinda não há avaliações

- Green BankingDocumento25 páginasGreen BankingAnnwar SingamayumAinda não há avaliações

- Using Standard Cost-Direct Labor VariancesDocumento14 páginasUsing Standard Cost-Direct Labor VariancesAlvi RahmanAinda não há avaliações

- 461 110 Falk Torus Elastomeric Coupling CatalogDocumento20 páginas461 110 Falk Torus Elastomeric Coupling CatalogLazzarus Az GunawanAinda não há avaliações

- 20 How Business Is Transacted Instock ExchangeDocumento14 páginas20 How Business Is Transacted Instock ExchangeSimranjeet SinghAinda não há avaliações

- MCI 01 Management ReviewDocumento3 páginasMCI 01 Management ReviewalexrferreiraAinda não há avaliações

- Doing Business in BruneiDocumento67 páginasDoing Business in BruneiAyman MehassebAinda não há avaliações

- Performance Evaluation FormDocumento6 páginasPerformance Evaluation FormBhushan100% (1)

- Pepsi-Cola Products Philippines Inc: - Income Statement For The Year 2014-2017Documento2 páginasPepsi-Cola Products Philippines Inc: - Income Statement For The Year 2014-2017Graciel Dela CruzAinda não há avaliações

- Leverage AnalysisDocumento29 páginasLeverage AnalysisFALAK OBERAIAinda não há avaliações

- Construction & Design Mang ManualDocumento93 páginasConstruction & Design Mang ManualSaad HajjarAinda não há avaliações

- Chapter ThreeDocumento20 páginasChapter Threehenokt129Ainda não há avaliações

- WEEK 6 Seminar Q&AsDocumento26 páginasWEEK 6 Seminar Q&AsMeenakshi SinhaAinda não há avaliações

- Ismail Ab - WahabDocumento57 páginasIsmail Ab - WahabNida RidzuanAinda não há avaliações

- List of Activities For ISO For Small Educational InstitutesDocumento2 páginasList of Activities For ISO For Small Educational InstitutesC P Chandrasekaran100% (2)

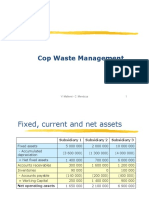

- Cop Waste Management SolutionDocumento5 páginasCop Waste Management SolutionPaul GhanimehAinda não há avaliações

- RFP Template Government ModelDocumento19 páginasRFP Template Government ModellgdkulclsubucvhgdjAinda não há avaliações

- SBIR Program OverviewDocumento13 páginasSBIR Program OverviewFernie1Ainda não há avaliações

- InTech-Project Costs and Risks Estimation Regarding Quality Management System ImplementationDocumento28 páginasInTech-Project Costs and Risks Estimation Regarding Quality Management System ImplementationMohamed ArzathAinda não há avaliações

- Material Inspection Request (MIR) : Fr-QC-17-00Documento1 páginaMaterial Inspection Request (MIR) : Fr-QC-17-00Tayyab AchakzaiAinda não há avaliações

- Case Study On Business Model Adopted by The Pogo Travels: Abu Sufiyan 151GCMD006 R V Institute of ManagementDocumento12 páginasCase Study On Business Model Adopted by The Pogo Travels: Abu Sufiyan 151GCMD006 R V Institute of ManagementSUFIYANAinda não há avaliações

- 523755152-503469149-GO2Bank-Template-2-2 NOVDocumento3 páginas523755152-503469149-GO2Bank-Template-2-2 NOVAlex NeziAinda não há avaliações

- Global Bees Wax Industry Report 2015Documento11 páginasGlobal Bees Wax Industry Report 2015api-282708578Ainda não há avaliações

- SM India Sub Region Back To Basics Problem Management ProcessDocumento12 páginasSM India Sub Region Back To Basics Problem Management ProcessJeevan PramodAinda não há avaliações

- More Than 100 CEOs Pressure Congress To Pass Immigration Bill by Jan. 19Documento1 páginaMore Than 100 CEOs Pressure Congress To Pass Immigration Bill by Jan. 19CNBC.comAinda não há avaliações

- Independent Contractor WaiverDocumento2 páginasIndependent Contractor WaiverPankaj PhartiyalAinda não há avaliações

- President COO Managing Director in Norwalk CT Resume Andrew HascoeDocumento2 páginasPresident COO Managing Director in Norwalk CT Resume Andrew HascoeAndrewHascoeAinda não há avaliações

- Learning Objectives - VAT (FINAL)Documento2 páginasLearning Objectives - VAT (FINAL)Pranay GovenderAinda não há avaliações

- Introduction To Industrial Relations - Chapter IDocumento9 páginasIntroduction To Industrial Relations - Chapter IKamal KatariaAinda não há avaliações