Você também pode gostar

- MSMEs or Micro Small and Medium Enterprses Share in India Exports 2013-2014Documento4 páginasMSMEs or Micro Small and Medium Enterprses Share in India Exports 2013-2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Coal Reserves To Last 100 YearsDocumento3 páginasIndia's Coal Reserves To Last 100 YearsJhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- #IndiaStockExchange #BSE Update On 24th June 2015Documento2 páginas#IndiaStockExchange #BSE Update On 24th June 2015Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

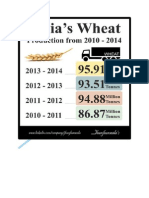

- India's Wheat Production From 2010 To 2014Documento4 páginasIndia's Wheat Production From 2010 To 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Crude Steel Production Estimate For 2014 To 2017Documento3 páginasIndia's Crude Steel Production Estimate For 2014 To 2017Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

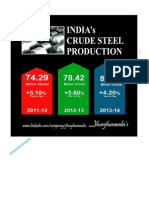

- India Crude Steel Production From 2011-2014Documento4 páginasIndia Crude Steel Production From 2011-2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Per Capita Food Grain For 2014Documento3 páginasIndia's Per Capita Food Grain For 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- Foreign Direct Investment in Equity Market in IndiaDocumento4 páginasForeign Direct Investment in Equity Market in IndiaJhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India Coir Trade From April To October 2014Documento4 páginasIndia Coir Trade From April To October 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Diamond Reserves With Diamond Trade Update For 2014Documento6 páginasIndia's Diamond Reserves With Diamond Trade Update For 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- Foreign Institutional Investors Investment in India During 2014-15 Until 27th November 2014Documento3 páginasForeign Institutional Investors Investment in India During 2014-15 Until 27th November 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

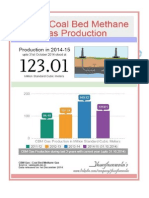

- India's Coal Bed Methane Production For Last 3 Years With Current Year 2014-15 (Upto 31 Oct 2014)Documento3 páginasIndia's Coal Bed Methane Production For Last 3 Years With Current Year 2014-15 (Upto 31 Oct 2014)Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's UREA Trade On 2013-14 and 2014-15 Up To November 2014.Documento3 páginasIndia's UREA Trade On 2013-14 and 2014-15 Up To November 2014.Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Rice Trade For 2014Documento5 páginasIndia's Rice Trade For 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Coal Production For Last 5 Years Upto October 2014Documento2 páginasIndia's Coal Production For Last 5 Years Upto October 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- Commercially Operating Nuclear Reactors in The World at The End of 2013Documento4 páginasCommercially Operating Nuclear Reactors in The World at The End of 2013Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Import and Export Update For September and December 2014Documento16 páginasIndia's Import and Export Update For September and December 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Methane Hydrates Reserves 25th November 2014Documento3 páginasIndia's Methane Hydrates Reserves 25th November 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- Indians Railways Revenue Earnings With Freight Traffic During April To October 2014Documento18 páginasIndians Railways Revenue Earnings With Freight Traffic During April To October 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- Global Central Banks Highlights For Monetary Policy Rates For October 2014Documento31 páginasGlobal Central Banks Highlights For Monetary Policy Rates For October 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- Foreign Investment Promotion Board Approves 12 Proposals of Foreign Direct Investment in India As On 19th December 2014Documento27 páginasForeign Investment Promotion Board Approves 12 Proposals of Foreign Direct Investment in India As On 19th December 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Kharif and Rabi Crops Area Coverage For October and January 2014Documento10 páginasIndia's Kharif and Rabi Crops Area Coverage For October and January 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Mineral Production in Month of August 2014Documento3 páginasIndia's Mineral Production in Month of August 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- Fuel Price Change For Petrol, Diesel, and JetFuel in IndiaDocumento11 páginasFuel Price Change For Petrol, Diesel, and JetFuel in IndiaJhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Tourism Sector Performance For January and October 2014Documento15 páginasIndia's Tourism Sector Performance For January and October 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Index of Eight Core Industries From June To November 2014Documento57 páginasIndia's Index of Eight Core Industries From June To November 2014Jhunjhunwalas Digital Finance & Business Info Library100% (1)

- India Tax Collection From April To November 2014Documento11 páginasIndia Tax Collection From April To November 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India 'S Total Kharif Crop Sowing Area As On July and August 2014Documento6 páginasIndia 'S Total Kharif Crop Sowing Area As On July and August 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

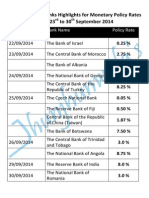

- Global Central Banks Highlights For Monetary Policy Rates From 23rd To 30th September 2014Documento11 páginasGlobal Central Banks Highlights For Monetary Policy Rates From 23rd To 30th September 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- Indian Currency Rupee Exchange Rate of 19 Foreign Currencies Relating To Import and Export Goods From July To September 2014Documento5 páginasIndian Currency Rupee Exchange Rate of 19 Foreign Currencies Relating To Import and Export Goods From July To September 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- Auditing Chapter 2 Part IIIDocumento3 páginasAuditing Chapter 2 Part IIIRegine A. AnsongAinda não há avaliações

- Reactions of Capital Markets To Financial ReportingDocumento25 páginasReactions of Capital Markets To Financial ReportingnarmadaAinda não há avaliações

- Prospects and Challenges of Industrialization in Bangladesh: M. A. Rashid SarkarDocumento17 páginasProspects and Challenges of Industrialization in Bangladesh: M. A. Rashid SarkarShakila JamanAinda não há avaliações

- DWSD Lifeline Plan - June 2022Documento12 páginasDWSD Lifeline Plan - June 2022Malachi BarrettAinda não há avaliações

- Lehman Brothers Examiners Report COMBINEDDocumento2.292 páginasLehman Brothers Examiners Report COMBINEDTroy UhlmanAinda não há avaliações

- UntitledDocumento986 páginasUntitledJindalAinda não há avaliações

- No. Tipe Akun Kode Perkiraan NamaDocumento6 páginasNo. Tipe Akun Kode Perkiraan Namapkm.sdjAinda não há avaliações

- Test Bank For Corporate Finance 4th Canadian Edition by BerkDocumento37 páginasTest Bank For Corporate Finance 4th Canadian Edition by Berkangelahollandwdeirnczob100% (23)

- Account StatementDocumento13 páginasAccount StatementMoses MguniAinda não há avaliações

- 4 Novozymes - Household - Care - Delivering Bioinnovation PDFDocumento7 páginas4 Novozymes - Household - Care - Delivering Bioinnovation PDFtmlAinda não há avaliações

- Introduction to Accounting EquationDocumento1 páginaIntroduction to Accounting Equationcons theAinda não há avaliações

- Bank LoansDocumento54 páginasBank LoansMark Alvin LandichoAinda não há avaliações

- Politicas Publicas EnergeticasDocumento38 páginasPoliticas Publicas EnergeticasRodrigo Arce RojasAinda não há avaliações

- ECO 120 Principles of Economics: Chapter 2: Theory of DEMAND and SupplyDocumento30 páginasECO 120 Principles of Economics: Chapter 2: Theory of DEMAND and Supplyizah893640Ainda não há avaliações

- BOI - New LetterDocumento5 páginasBOI - New Lettersandip_banerjeeAinda não há avaliações

- GRI 3: Material Topics 2021: Universal StandardDocumento30 páginasGRI 3: Material Topics 2021: Universal StandardMaría Belén MartínezAinda não há avaliações

- Workday Glossary of TermsDocumento27 páginasWorkday Glossary of Termsnaimenim100% (1)

- Lkas 27Documento15 páginasLkas 27nithyAinda não há avaliações

- Role of Public Financial Management in Risk Management For Developing Country GovernmentsDocumento31 páginasRole of Public Financial Management in Risk Management For Developing Country GovernmentsFreeBalanceGRPAinda não há avaliações

- PM RN A4.Throughput CostingDocumento5 páginasPM RN A4.Throughput Costinghow cleverAinda não há avaliações

- Market StructureDocumento14 páginasMarket StructurevmktptAinda não há avaliações

- Auto Finance Industry AnalysisDocumento15 páginasAuto Finance Industry AnalysisMitul SuranaAinda não há avaliações

- DHL TaiwanDocumento25 páginasDHL TaiwanPhương VõAinda não há avaliações

- A Study of Non Performing Assets in Bank of BarodaDocumento88 páginasA Study of Non Performing Assets in Bank of BarodaShubham MayekarAinda não há avaliações

- Rural Urban MigrationDocumento42 páginasRural Urban MigrationSabitha Ansif100% (1)

- Kalamba Games - 51% Majority Stake Investment Opportunity - July23Documento17 páginasKalamba Games - 51% Majority Stake Investment Opportunity - July23Calvin LimAinda não há avaliações

- Pacific Oxygen Vs Central BankDocumento3 páginasPacific Oxygen Vs Central BankAmmie AsturiasAinda não há avaliações

- ISM - PrimarkDocumento17 páginasISM - PrimarkRatri Ika PratiwiAinda não há avaliações

- Team 6 - Pricing Assignment 2 - Cambridge Software Corporation V 1.0Documento7 páginasTeam 6 - Pricing Assignment 2 - Cambridge Software Corporation V 1.0SJ100% (1)

- Overview of Franchising Activities in VietnamDocumento5 páginasOverview of Franchising Activities in VietnamNo NameAinda não há avaliações