Você também pode gostar

- Submitted To Madurai Kamaraj University in Partial Fulfilment of The Requirement For The Degree ofDocumento6 páginasSubmitted To Madurai Kamaraj University in Partial Fulfilment of The Requirement For The Degree ofChasity MorseAinda não há avaliações

- Project ReportDocumento117 páginasProject ReportHarshita Jain0% (2)

- Sources of Finance SMEDocumento11 páginasSources of Finance SMEakram balochAinda não há avaliações

- MSME Issues and Challenges 1Documento7 páginasMSME Issues and Challenges 1Rashmi Ranjan PanigrahiAinda não há avaliações

- Research Paper On Micro Small and Medium EnterprisesDocumento5 páginasResearch Paper On Micro Small and Medium EnterprisesvvjrpsbndAinda não há avaliações

- Paper8 ICSSRSeminarPaperDocumento12 páginasPaper8 ICSSRSeminarPaperima doucheAinda não há avaliações

- Vivek FinalReportDocumento41 páginasVivek FinalReportVivek VvkAinda não há avaliações

- Working Capital FinanceDocumento54 páginasWorking Capital FinanceAnkur RazdanAinda não há avaliações

- Thesis On Small and Medium Enterprises in IndiaDocumento5 páginasThesis On Small and Medium Enterprises in Indiacourtneypetersonspringfield100% (2)

- IJEMSVol52 8Documento8 páginasIJEMSVol52 8sajidakhtar6505Ainda não há avaliações

- Sidbi-A Successful Financial Institution in Sme Financing: Manasvi MohanDocumento12 páginasSidbi-A Successful Financial Institution in Sme Financing: Manasvi MohanmanasvimohanAinda não há avaliações

- Msme Sector: Challenges and Opportunities: Neha Singh, Dr. Sneh P. DanielDocumento4 páginasMsme Sector: Challenges and Opportunities: Neha Singh, Dr. Sneh P. DanielSmriti SFS 79Ainda não há avaliações

- Impact On Financial Problems Faced by Msme in IndiaDocumento17 páginasImpact On Financial Problems Faced by Msme in Indiajay joshiAinda não há avaliações

- Black BookDocumento56 páginasBlack Bookyashvidoshi04Ainda não há avaliações

- M.Phil Thesis Final On CREDIT FACILITIES FOR SME's by PUTTU GURU PRASADDocumento148 páginasM.Phil Thesis Final On CREDIT FACILITIES FOR SME's by PUTTU GURU PRASADPUTTU GURU PRASAD SENGUNTHA MUDALIAR100% (10)

- 11 Arihant Surana - Small Scale Industries and Their Role inDocumento33 páginas11 Arihant Surana - Small Scale Industries and Their Role inPrashant RanaAinda não há avaliações

- Sabari Final ProjectDocumento54 páginasSabari Final ProjectRam KumarAinda não há avaliações

- M.B.a. 4th Sem Project ReportDocumento89 páginasM.B.a. 4th Sem Project ReportAkankshaSingh83% (6)

- Statistics Project Report PGDM FinalDocumento45 páginasStatistics Project Report PGDM FinalSoham KhannaAinda não há avaliações

- Major Marketing Problems Faced by Msme SectorsDocumento43 páginasMajor Marketing Problems Faced by Msme SectorsPradeep Kumar Pandey100% (1)

- Various Risks Involved in SME Units and Measures To Fight Them: A Case Study On SME Units With Special Reference To Moradabad-IndiaDocumento6 páginasVarious Risks Involved in SME Units and Measures To Fight Them: A Case Study On SME Units With Special Reference To Moradabad-IndiaInternational Journal of Application or Innovation in Engineering & ManagementAinda não há avaliações

- The Relevance of Working Capital, Financial Literacy and Financial Inclusion On Financial Performance and Sustainability of Micro, Small and Medium-Sized Enterprises (MSMEs)Documento14 páginasThe Relevance of Working Capital, Financial Literacy and Financial Inclusion On Financial Performance and Sustainability of Micro, Small and Medium-Sized Enterprises (MSMEs)AJHSSR JournalAinda não há avaliações

- MSME Financing Growth and ChallengeDocumento13 páginasMSME Financing Growth and Challengejay joshiAinda não há avaliações

- Annexure V Cover Page For Academic TasksDocumento9 páginasAnnexure V Cover Page For Academic TasksAbhijeet BhardwajAinda não há avaliações

- IJCRT2105017Documento7 páginasIJCRT2105017G LifecareAinda não há avaliações

- Financing in MSMEs-The Major IssuesDocumento9 páginasFinancing in MSMEs-The Major Issuesjay joshiAinda não há avaliações

- Credit Facilities For Smes. EditedDocumento135 páginasCredit Facilities For Smes. EditedArvin GoswamiAinda não há avaliações

- Entreprenuship ProjectDocumento34 páginasEntreprenuship ProjectBasil JohnAinda não há avaliações

- Micro Small Med-Wps OfficeDocumento25 páginasMicro Small Med-Wps OfficeCapture PhotographyAinda não há avaliações

- Role of MSME in Entrepreneurship Development-A Case Study: Dr. Feroz Hakeem Atif Javed Qazi, Raashidah GaniDocumento5 páginasRole of MSME in Entrepreneurship Development-A Case Study: Dr. Feroz Hakeem Atif Javed Qazi, Raashidah Ganisoheb sayyedAinda não há avaliações

- Micro Small Medium Enterprises Sector in India: A Way ForwardDocumento8 páginasMicro Small Medium Enterprises Sector in India: A Way ForwardMadhwendra SinghAinda não há avaliações

- IJRASET53750 PPRDocumento5 páginasIJRASET53750 PPRSuraj DubeyAinda não há avaliações

- MSME Paper 2 For PublicationDocumento18 páginasMSME Paper 2 For Publicationteam eliteAinda não há avaliações

- Sme Financing: Ipo Issue and Post-Ipo Analysis: Prashant Gupta, Associate Professor at IMI, Delhi, Prashantgupta@imi - EduDocumento10 páginasSme Financing: Ipo Issue and Post-Ipo Analysis: Prashant Gupta, Associate Professor at IMI, Delhi, Prashantgupta@imi - EduSimhaAinda não há avaliações

- Financing TheoryDocumento43 páginasFinancing TheoryDrubo SoburAinda não há avaliações

- Role of Smes in Accelerating Growth of Economic Conditions in BangladeshDocumento13 páginasRole of Smes in Accelerating Growth of Economic Conditions in BangladeshAnika Tabassum RodelaAinda não há avaliações

- Sources of FinanceDocumento59 páginasSources of Financeprayas sarkarAinda não há avaliações

- SME Financing in Bangladesh NewDocumento42 páginasSME Financing in Bangladesh NewDrubo Sobur100% (1)

- Section IDocumento4 páginasSection ISoumya JainAinda não há avaliações

- Tunrayo 1-3Documento34 páginasTunrayo 1-3Ibrahim AlabiAinda não há avaliações

- Problems and Prospects of Micro, Small & Medium Enterprises (MSME's) in IndiaDocumento22 páginasProblems and Prospects of Micro, Small & Medium Enterprises (MSME's) in IndiaAmol LahaneAinda não há avaliações

- An Empirical Study On The Role of MUDRA Yojana in Financing Micro EnterprisesDocumento11 páginasAn Empirical Study On The Role of MUDRA Yojana in Financing Micro EnterprisesRahul V MohareAinda não há avaliações

- Role of SMEDocumento7 páginasRole of SMEAdr HRAinda não há avaliações

- Electa 1-4Documento64 páginasElecta 1-4OSSMANOU MUSTAPHAAinda não há avaliações

- Thesis. Final FileDocumento25 páginasThesis. Final FileSoumitree MazumderAinda não há avaliações

- Growth and Performance of Micro Small and Medium Enterprises in IndiaDocumento12 páginasGrowth and Performance of Micro Small and Medium Enterprises in IndiaDr.R.Vettriselvan A.P.- ABSAinda não há avaliações

- A Study On Effects of Micro Financing On Msmes in KarnatakaDocumento9 páginasA Study On Effects of Micro Financing On Msmes in KarnatakaPavithra GowthamAinda não há avaliações

- Literature Review For Retail BankingDocumento10 páginasLiterature Review For Retail BankingNishant Grover100% (1)

- The Influence of Financial Literacy On Smes Performance Through Access 1528 2635 24-5-595Documento17 páginasThe Influence of Financial Literacy On Smes Performance Through Access 1528 2635 24-5-595rexAinda não há avaliações

- Thesis On Small Scale Industries in IndiaDocumento5 páginasThesis On Small Scale Industries in Indiabsr8frht100% (2)

- English Assignment 1Documento30 páginasEnglish Assignment 1Satyapriya PangiAinda não há avaliações

- Title: Study of Impact of Coronavirus Pandemic On Small and Medium Enterprises (SME's) in IndiaDocumento7 páginasTitle: Study of Impact of Coronavirus Pandemic On Small and Medium Enterprises (SME's) in IndiaShruti JainAinda não há avaliações

- Thesis On Micro Small and Medium EnterprisesDocumento7 páginasThesis On Micro Small and Medium Enterprisesafcnfajtd100% (2)

- DocumentDocumento7 páginasDocumentAkashAinda não há avaliações

- Draft Research Report-1Documento23 páginasDraft Research Report-1Prince FranieAinda não há avaliações

- Small and Medium EnterprisesDocumento9 páginasSmall and Medium EnterprisesDr NallusamyAinda não há avaliações

- Impact of Motivation and Digitization on Women EntrepreneurshipNo EverandImpact of Motivation and Digitization on Women EntrepreneurshipAinda não há avaliações

- The Future Path of SMEs: How to Grow in the New Global EconomyNo EverandThe Future Path of SMEs: How to Grow in the New Global EconomyAinda não há avaliações

- Demystifying Venture Capital: How It Works and How to Get ItNo EverandDemystifying Venture Capital: How It Works and How to Get ItAinda não há avaliações

- DK'KH Fgunw Fo'Ofo - Ky : Lire Izxfr IzfrosnuDocumento9 páginasDK'KH Fgunw Fo'Ofo - Ky : Lire Izxfr IzfrosnuAnonymous V9E1ZJtwoEAinda não há avaliações

- Usiky Ls ÇDKF'KR Usikyh HKK"KK Ds Çeq (K Nsfud Lekpkj I Ksa DK Vè UDocumento2 páginasUsiky Ls ÇDKF'KR Usikyh HKK"KK Ds Çeq (K Nsfud Lekpkj I Ksa DK Vè UAnonymous V9E1ZJtwoEAinda não há avaliações

- Project Report On Online Examination System: Submitted To Submitted By: Pooja Yadav Pinky Singh Bca Vi SemDocumento2 páginasProject Report On Online Examination System: Submitted To Submitted By: Pooja Yadav Pinky Singh Bca Vi SemAnonymous V9E1ZJtwoEAinda não há avaliações

- Attitude of Secondary School Students of Ballia District Towards Online LearningDocumento4 páginasAttitude of Secondary School Students of Ballia District Towards Online LearningAnonymous V9E1ZJtwoEAinda não há avaliações

- DLWDocumento83 páginasDLWAnonymous V9E1ZJtwoEAinda não há avaliações

- A Study On Housing Finance Services in Kerala With Special Reference To HDFC and Lic Housing Finance LTDDocumento1 páginaA Study On Housing Finance Services in Kerala With Special Reference To HDFC and Lic Housing Finance LTDAnonymous V9E1ZJtwoEAinda não há avaliações

- Shri Baldev P.G. College - Varanasi: Project On NutritonDocumento1 páginaShri Baldev P.G. College - Varanasi: Project On NutritonAnonymous V9E1ZJtwoEAinda não há avaliações

- Invoice: Address: Phone: Fax EmailDocumento2 páginasInvoice: Address: Phone: Fax EmailAnonymous V9E1ZJtwoEAinda não há avaliações

- Summer Training ReportDocumento77 páginasSummer Training ReportAnonymous V9E1ZJtwoEAinda não há avaliações

- 1.1 Gaunyle: The Good Will Project Jan.23,2017)Documento40 páginas1.1 Gaunyle: The Good Will Project Jan.23,2017)Anonymous V9E1ZJtwoEAinda não há avaliações

- A Study of The Prospective Teachers' Attitude Towaeds 1 Semester Theory Papers of Two Year B.Ed. Programme of Banaras Hindu UniversityDocumento7 páginasA Study of The Prospective Teachers' Attitude Towaeds 1 Semester Theory Papers of Two Year B.Ed. Programme of Banaras Hindu UniversityAnonymous V9E1ZJtwoEAinda não há avaliações

- Sales and Distribution of Patanjali ProductDocumento87 páginasSales and Distribution of Patanjali ProductAnonymous V9E1ZJtwoE80% (20)

- Cluster Activation &management: Summer Training in Hindustan Coca-Cola Beverage Pvt. LTDDocumento5 páginasCluster Activation &management: Summer Training in Hindustan Coca-Cola Beverage Pvt. LTDAnonymous V9E1ZJtwoEAinda não há avaliações

- Km. Anita KumariDocumento2 páginasKm. Anita KumariAnonymous V9E1ZJtwoEAinda não há avaliações

- Prashant DubeyDocumento106 páginasPrashant DubeyAnonymous V9E1ZJtwoEAinda não há avaliações

- Dwa RikaDocumento75 páginasDwa RikaAnonymous V9E1ZJtwoEAinda não há avaliações

- Combined Defence Services Examination (II) 2016 11636836879 सं यु d땜 र行⊭ा से वा परी行⊭ा (II) 2016Documento1 páginaCombined Defence Services Examination (II) 2016 11636836879 सं यु d땜 र行⊭ा से वा परी行⊭ा (II) 2016Anonymous V9E1ZJtwoEAinda não há avaliações

- Randi BazDocumento42 páginasRandi BazAnonymous V9E1ZJtwoEAinda não há avaliações

- Mahatma Gandhi Kashi Vidyapith UniversityDocumento2 páginasMahatma Gandhi Kashi Vidyapith UniversityAnonymous V9E1ZJtwoEAinda não há avaliações

- WS Retail Services Pvt. LTD.Documento1 páginaWS Retail Services Pvt. LTD.Anonymous V9E1ZJtwoEAinda não há avaliações

- Reliance Letter PadDocumento60 páginasReliance Letter PadAnonymous V9E1ZJtwoEAinda não há avaliações

- UGC - National Eligibility Test December, 2014: Print Copy of Application FormDocumento1 páginaUGC - National Eligibility Test December, 2014: Print Copy of Application FormAnonymous V9E1ZJtwoEAinda não há avaliações

- Sundarpur Varanasi: Project On Professional CommunicationDocumento8 páginasSundarpur Varanasi: Project On Professional CommunicationAnonymous V9E1ZJtwoEAinda não há avaliações

- Bio-Data: For Interview For Faculty PositionsDocumento7 páginasBio-Data: For Interview For Faculty PositionsAnonymous V9E1ZJtwoEAinda não há avaliações

- Wells Fargo Everyday Checking: Important Account InformationDocumento4 páginasWells Fargo Everyday Checking: Important Account InformationLoaiAinda não há avaliações

- Practice Set No. 1Documento6 páginasPractice Set No. 1Rexie Tan100% (2)

- Credit Management in Banks - BasicsDocumento35 páginasCredit Management in Banks - BasicsMuralidharprasad AyaluruAinda não há avaliações

- 73432bos59248 p1Documento32 páginas73432bos59248 p1sneha rajputAinda não há avaliações

- MVB StatementDocumento3 páginasMVB StatementDerrick MorrisonAinda não há avaliações

- CA Foundation Accounts RTP May 2023Documento32 páginasCA Foundation Accounts RTP May 2023PushkarAinda não há avaliações

- LPB 93th JAIBBDocumento4 páginasLPB 93th JAIBBIslam BankAinda não há avaliações

- Insurance Claims For Loss of Stock and Loss of Profit 2 PDFDocumento22 páginasInsurance Claims For Loss of Stock and Loss of Profit 2 PDFEswari Gk100% (1)

- Presentation 1Documento21 páginasPresentation 1Damodharan RanjithAinda não há avaliações

- CA Inter Advanced Account - Regular Course by CA P S BeniwalDocumento346 páginasCA Inter Advanced Account - Regular Course by CA P S BeniwalHarry PotterAinda não há avaliações

- Banzai Life ScenariosDocumento12 páginasBanzai Life Scenariosapi-380813240Ainda não há avaliações

- Bank Confirmation Inquiry-FormatDocumento3 páginasBank Confirmation Inquiry-FormatbarcelonnaAinda não há avaliações

- Working Capital Financing Policy of HDFC, IDBI, Canara Bank, Indian Overseas Bank and Axis BankDocumento17 páginasWorking Capital Financing Policy of HDFC, IDBI, Canara Bank, Indian Overseas Bank and Axis BankjashanAinda não há avaliações

- Learning English Banking - 2Documento6 páginasLearning English Banking - 2AiVi TranAinda não há avaliações

- Credit and Debit CardDocumento2 páginasCredit and Debit Cardnouha KABBAJAinda não há avaliações

- Gen-Next Junior (Saving Account) : Product NatureDocumento6 páginasGen-Next Junior (Saving Account) : Product NaturedinkaramAinda não há avaliações

- Business Advantage Statement: Welcome To Your Anz Account at A GlanceDocumento12 páginasBusiness Advantage Statement: Welcome To Your Anz Account at A GlanceAlexander BondAinda não há avaliações

- Account and Auditing Some NotesDocumento13 páginasAccount and Auditing Some NotesBasilDarlongDiengdohAinda não há avaliações

- 546604050000007Documento29 páginas546604050000007PriyankaAinda não há avaliações

- Regions StatementDocumento4 páginasRegions StatementTemecco BufordAinda não há avaliações

- BRS PDFDocumento14 páginasBRS PDFGautam KhanwaniAinda não há avaliações

- M&T Bank Statement of Oct 21Documento2 páginasM&T Bank Statement of Oct 21Jonathan Seagull LivingstonAinda não há avaliações

- ThirdPartyRetrieveDocument AspDocumento4 páginasThirdPartyRetrieveDocument AspElizabeth HilsonAinda não há avaliações

- Statement of Account: Date of Opening Account Status Account Type Currency Mr. Ranjeet KumarDocumento4 páginasStatement of Account: Date of Opening Account Status Account Type Currency Mr. Ranjeet KumarRohit raagAinda não há avaliações

- Allied Banking Corp V Spouses Macam G.R. No. 200635, (February 1, 2021)Documento12 páginasAllied Banking Corp V Spouses Macam G.R. No. 200635, (February 1, 2021)RLAMMAinda não há avaliações

- Wells Fargo Everyday CheckingDocumento5 páginasWells Fargo Everyday CheckingTrish HitAinda não há avaliações

- Wells Fargo Statement - Oct 2022Documento6 páginasWells Fargo Statement - Oct 2022pradeep yadavAinda não há avaliações

- BUSINESS STUDIES (Code No. 054) : RationaleDocumento8 páginasBUSINESS STUDIES (Code No. 054) : RationaleAyesha QureshiAinda não há avaliações

- Identifying Different Sources of Finance PDFDocumento12 páginasIdentifying Different Sources of Finance PDFMzee KodiaAinda não há avaliações

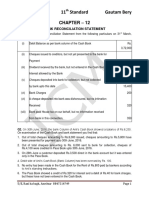

- Bank Reconciliation StatementDocumento22 páginasBank Reconciliation StatementasimaAinda não há avaliações