Você também pode gostar

- Airtel StrategiesDocumento3 páginasAirtel Strategiesprabhakar_elexAinda não há avaliações

- Microsoft PowerPoint - Cesim PresentationDocumento18 páginasMicrosoft PowerPoint - Cesim PresentationTran Van HienAinda não há avaliações

- Orascom Telecom Holding Annual Report 2009Documento83 páginasOrascom Telecom Holding Annual Report 2009류현정Ainda não há avaliações

- TCC LTDDocumento17 páginasTCC LTDjithukpAinda não há avaliações

- What Are The Critical Legal Issues in This Case?Documento5 páginasWhat Are The Critical Legal Issues in This Case?Atif MajeedAinda não há avaliações

- Saudi Budget 2017 - Kingdom of Saudi ArabiaDocumento40 páginasSaudi Budget 2017 - Kingdom of Saudi ArabiaSaudi ExpatriateAinda não há avaliações

- Renault-Nissan Alliance Perspective: Thierry MOULONGUETDocumento11 páginasRenault-Nissan Alliance Perspective: Thierry MOULONGUETSathish KumarAinda não há avaliações

- Oligopoly in Oil Refinery IndustryDocumento5 páginasOligopoly in Oil Refinery IndustryDokania Anish100% (2)

- Case Study:: Singapore Airlines - The India DecisionDocumento27 páginasCase Study:: Singapore Airlines - The India DecisionCon FluenceAinda não há avaliações

- Net ScapeDocumento15 páginasNet ScapestefanofontanaAinda não há avaliações

- QNB Research On Macro Trends GCCDocumento55 páginasQNB Research On Macro Trends GCCdhoomketuAinda não há avaliações

- ECON 625 Problem Set 3Documento5 páginasECON 625 Problem Set 3Rising Home Tutions0% (2)

- CFIN Formula Sheet UpdatedDocumento2 páginasCFIN Formula Sheet UpdatedChakri MunagalaAinda não há avaliações

- Deloitte Maverick: A Study and Analysis of The US Telco CaseDocumento11 páginasDeloitte Maverick: A Study and Analysis of The US Telco CaseNikhil SharmaAinda não há avaliações

- Grameen PhoneDocumento37 páginasGrameen PhoneSK Nasif HasanAinda não há avaliações

- TechNote - DIS Daiki Japan Seawater Electrochlorination ProposalsDocumento5 páginasTechNote - DIS Daiki Japan Seawater Electrochlorination ProposalsRomeo Jaka RAinda não há avaliações

- EOS House of TATA RevitalizationDocumento4 páginasEOS House of TATA Revitalizationchinmayee beheraAinda não há avaliações

- MRO On The Move: Outsourcing Maintenance, Repair and OperationsDocumento12 páginasMRO On The Move: Outsourcing Maintenance, Repair and Operationssha_yadAinda não há avaliações

- Tata Motors Acquisition of JLRDocumento13 páginasTata Motors Acquisition of JLRHarsh TimbadiaAinda não há avaliações

- Tata CorusDocumento16 páginasTata CorusTarun Daga100% (2)

- Global Home Appliance Industry Market Research 2017Documento8 páginasGlobal Home Appliance Industry Market Research 2017Norah TrentAinda não há avaliações

- Operation Strategy at Galanz - Piyush KatejaDocumento11 páginasOperation Strategy at Galanz - Piyush KatejaPiyush KatejaAinda não há avaliações

- Bharat Rasayan StockDocumento8 páginasBharat Rasayan StockajaynkotiAinda não há avaliações

- DressenDocumento22 páginasDressenGonz�lez Alonzo Juan ManuelAinda não há avaliações

- AirbusDocumento2 páginasAirbusapi-221421240Ainda não há avaliações

- Tata Corus DealDocumento39 páginasTata Corus DealdhavalkurveyAinda não há avaliações

- Barrick Gold Corporation - TanzaniaDocumento19 páginasBarrick Gold Corporation - TanzaniaRajesh Kumar PradhanAinda não há avaliações

- Motorola RAZR - Case PDFDocumento8 páginasMotorola RAZR - Case PDFSergio AlejandroAinda não há avaliações

- Scope of Renault and NissanDocumento17 páginasScope of Renault and NissanUmais Shafqat100% (1)

- Toyota Al Futtaim FinalDocumento15 páginasToyota Al Futtaim FinalVanessa_Dsilva_1300Ainda não há avaliações

- BPCL's Petrol Pump Retail RevolutionDocumento16 páginasBPCL's Petrol Pump Retail RevolutionASHISHRD100% (1)

- 18P086 SM BikanerwalaDocumento11 páginas18P086 SM BikanerwalakshipraAinda não há avaliações

- Pneumatic Oil Security Data SheetDocumento4 páginasPneumatic Oil Security Data SheetSayed Diab AlsayedAinda não há avaliações

- Growth Possibilities For US TelcoDocumento9 páginasGrowth Possibilities For US TelcoAnkit GoyalAinda não há avaliações

- Egypt Complete DataDocumento309 páginasEgypt Complete DataPreetam GodboleAinda não há avaliações

- Established in 1995Documento2 páginasEstablished in 1995Kande AbhijitAinda não há avaliações

- Jaguar Report Case StudyDocumento23 páginasJaguar Report Case StudyAkshay JoshiAinda não há avaliações

- Tata Corus Case Analysis at GargDocumento20 páginasTata Corus Case Analysis at GargNikhil Garg80% (5)

- HRM CaseDocumento20 páginasHRM CasePriyam ChakrabortyAinda não há avaliações

- Operations Management: Ace Institute of ManagementDocumento10 páginasOperations Management: Ace Institute of ManagementSunsay GubhajuAinda não há avaliações

- GE CaseDocumento20 páginasGE CaseMeenal MalhotraAinda não há avaliações

- Mannesmann Vs VodafoneDocumento17 páginasMannesmann Vs VodafoneDiana MoiseAinda não há avaliações

- Tata HitachiDocumento16 páginasTata HitachiSamadarshi SarkarAinda não há avaliações

- 1 Jackwelch and General ElectricDocumento6 páginas1 Jackwelch and General ElectricrahulkejAinda não há avaliações

- Dhahran Simplified StarterDocumento6 páginasDhahran Simplified StarterAbdullah AhmedAinda não há avaliações

- Sample - Contact Lenses Market Analysis and Segment Forecasts To 2025Documento48 páginasSample - Contact Lenses Market Analysis and Segment Forecasts To 2025GargiSanzgiriAinda não há avaliações

- Submitted To: Submitted By:: Waste Management System Using Vehicle Tracking SystemDocumento38 páginasSubmitted To: Submitted By:: Waste Management System Using Vehicle Tracking SystemEr Rajat KumarAinda não há avaliações

- Finanacial Restructuring 2Documento48 páginasFinanacial Restructuring 2Jim Mathilakathu100% (2)

- West Faded FlamesDocumento10 páginasWest Faded FlamesAbhijeet PatilAinda não há avaliações

- Facebook Acquires WhatsAppDocumento7 páginasFacebook Acquires WhatsAppJoel DavisAinda não há avaliações

- Mode of EntryDocumento3 páginasMode of EntrybhavsheelkohliAinda não há avaliações

- Take Home Quiz: This Study Resource WasDocumento4 páginasTake Home Quiz: This Study Resource Wasகப்பல்ஹசன்நபி0% (1)

- 06 Investors Presentation Juin 2021Documento70 páginas06 Investors Presentation Juin 2021bioseedAinda não há avaliações

- DanfossDocumento25 páginasDanfossalirrehmanAinda não há avaliações

- CESIM CaseDocumento8 páginasCESIM CaseDhawal PanchalAinda não há avaliações

- Case Chapter 11: Management Information SystemsDocumento12 páginasCase Chapter 11: Management Information SystemsAnonymous zxzokTrX2OAinda não há avaliações

- SNGPLDocumento28 páginasSNGPLKashif Naveed100% (2)

- Msdi Alcala de Henares, Spain: Click To Edit Master Subtitle StyleDocumento24 páginasMsdi Alcala de Henares, Spain: Click To Edit Master Subtitle StyleShashank Shekhar100% (1)

- Bahrain Jordan Kuwait Iraq Saudi Arabia Sudan LebanonDocumento4 páginasBahrain Jordan Kuwait Iraq Saudi Arabia Sudan LebanonSyed M. HussainAinda não há avaliações

- Presented By: Syndicate 5 Anupam Agrawal Anshuman Sen Anish Bhatt Dipali Lavangare Pawan Talvare Subhrajit BhaumikDocumento17 páginasPresented By: Syndicate 5 Anupam Agrawal Anshuman Sen Anish Bhatt Dipali Lavangare Pawan Talvare Subhrajit Bhaumikanupam_agAinda não há avaliações

- MMC Group's Corporate Presentation May 2012Documento13 páginasMMC Group's Corporate Presentation May 2012Carlos ValdecantosAinda não há avaliações

- MMC Group IPTV Strategy Case Study Jan2012Documento30 páginasMMC Group IPTV Strategy Case Study Jan2012Carlos Valdecantos100% (1)

- MMC Pricing Elasticity Analysis June2011Documento17 páginasMMC Pricing Elasticity Analysis June2011Carlos ValdecantosAinda não há avaliações

- Results: January-December / 2010 January December / 2010Documento75 páginasResults: January-December / 2010 January December / 2010Carlos ValdecantosAinda não há avaliações

- CMR 2010 FinalDocumento379 páginasCMR 2010 FinalfaizanhabibAinda não há avaliações

- MMC Group - Mobile Intenert Market Spain2010Documento6 páginasMMC Group - Mobile Intenert Market Spain2010Carlos ValdecantosAinda não há avaliações

- MMC Approach Multiple SIM BlogDocumento17 páginasMMC Approach Multiple SIM BlogCarlos Valdecantos100% (3)

- AMC - Taranis - CH0575781247 - PO - Terms - Final - NEWDocumento19 páginasAMC - Taranis - CH0575781247 - PO - Terms - Final - NEWBuchotAinda não há avaliações

- Financial ServicesDocumento10 páginasFinancial ServicesDinesh Sugumaran100% (4)

- Lecture Notes On Quasi-ReorganizationDocumento2 páginasLecture Notes On Quasi-ReorganizationalyssaAinda não há avaliações

- 3i Group 2007 Annual ReportDocumento116 páginas3i Group 2007 Annual ReportAsiaBuyouts100% (2)

- Capital Gains Tax QuestionsDocumento4 páginasCapital Gains Tax QuestionsRedfield GrahamAinda não há avaliações

- Chapter 1 - Structure of Financial SystemDocumento18 páginasChapter 1 - Structure of Financial SystemNur HazirahAinda não há avaliações

- Omar Halabieh's Review of Market WizardsDocumento2 páginasOmar Halabieh's Review of Market Wizardsmytemp_01Ainda não há avaliações

- Valuation Measuring and Managing The Value of Companies 6th Edition Mckinsey Test BankDocumento8 páginasValuation Measuring and Managing The Value of Companies 6th Edition Mckinsey Test BankRyanArmstrongwnkgs100% (17)

- Financial Institutions Instruments and Markets 8th Edition Viney Solutions ManualDocumento35 páginasFinancial Institutions Instruments and Markets 8th Edition Viney Solutions Manualchicanerdarterfeyq100% (25)

- TEST-8: Lesson 3 Monetary SystemDocumento26 páginasTEST-8: Lesson 3 Monetary SystemDeepak ShahAinda não há avaliações

- Chapter 1Documento37 páginasChapter 1Elma UmmatiAinda não há avaliações

- Steve BelkinDocumento13 páginasSteve BelkinpodxAinda não há avaliações

- Nike Inc q414 Press Release - 6-25-2014 6pm - CleanDocumento9 páginasNike Inc q414 Press Release - 6-25-2014 6pm - CleanmanduramAinda não há avaliações

- Basic Banking ConceptsDocumento17 páginasBasic Banking ConceptsVishnuvardhan VishnuAinda não há avaliações

- Liquidation of CompaniesDocumento12 páginasLiquidation of CompaniesFaisal ManjiAinda não há avaliações

- 2022 - Strategic Management 731 - CA Test 2 Review QuestionsDocumento19 páginas2022 - Strategic Management 731 - CA Test 2 Review QuestionsMaria LettaAinda não há avaliações

- Corporate Finance-Final ExamDocumento3 páginasCorporate Finance-Final ExamAssignment HelperAinda não há avaliações

- 215 Ranu SainiDocumento58 páginas215 Ranu Saininafemip221Ainda não há avaliações

- Why The ISDA SIMM Methdology Is Not What I ExpectedDocumento5 páginasWhy The ISDA SIMM Methdology Is Not What I Expected남상욱Ainda não há avaliações

- Essentials of Private Real Estate International BrochureDocumento16 páginasEssentials of Private Real Estate International BrochureNAinda não há avaliações

- Group Assignment Questions GB30703 - Set 1Documento2 páginasGroup Assignment Questions GB30703 - Set 1March ClaAinda não há avaliações

- BP'S Office of The Chief Technology Officer (A) : Driving Open Innovation Through An Advocate TeamDocumento2 páginasBP'S Office of The Chief Technology Officer (A) : Driving Open Innovation Through An Advocate TeamsruthiAinda não há avaliações

- NAL Online Training Program Online Rapid Learning Series-VDocumento7 páginasNAL Online Training Program Online Rapid Learning Series-VKripal SinghAinda não há avaliações

- LG (Electronics) ,: Total 102260Documento2 páginasLG (Electronics) ,: Total 102260Ben HiranAinda não há avaliações

- ToaDocumento18 páginasToaFritzie Ann ZartigaAinda não há avaliações

- Certificate Program in Financial Analysis, Valuation & Risk ManagementDocumento16 páginasCertificate Program in Financial Analysis, Valuation & Risk ManagementCharvi SaxenaAinda não há avaliações

- Guide For Private Wealth ManagementDocumento248 páginasGuide For Private Wealth Managementvotchen2008Ainda não há avaliações

- All Bullish Candlestick PatternsDocumento24 páginasAll Bullish Candlestick PatternsxhghdghAinda não há avaliações

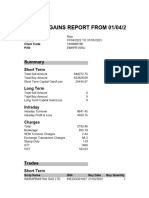

- Capital Gains - Stocks-GrowwDocumento11 páginasCapital Gains - Stocks-Growwriyagupta10122000Ainda não há avaliações

- Module 34 Share Based Compensation TheoryDocumento2 páginasModule 34 Share Based Compensation TheoryThalia UyAinda não há avaliações