Você também pode gostar

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- Management Review Agenda and Minutes1Documento7 páginasManagement Review Agenda and Minutes1sadbad660% (5)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- FAD 4.0 - IsO-IEC 17065 GAC Application DocumentDocumento44 páginasFAD 4.0 - IsO-IEC 17065 GAC Application Documentsadbad6Ainda não há avaliações

- BYJu'S PresentationDocumento15 páginasBYJu'S PresentationManpreet Kaur33% (3)

- June 2021 Mark SchemeDocumento17 páginasJune 2021 Mark SchemeElenaAinda não há avaliações

- Government Securities MarketDocumento11 páginasGovernment Securities MarketVikasDalal100% (2)

- Iso AuditDocumento4 páginasIso Auditsadbad6Ainda não há avaliações

- BRC Certification Guideline - Rev 09Documento22 páginasBRC Certification Guideline - Rev 09sadbad6100% (1)

- ISO 22000 Food Safety Management Quality Manual PDFDocumento46 páginasISO 22000 Food Safety Management Quality Manual PDFsadbad656% (9)

- ISO 17025 2017 Training Course and ChangesDocumento48 páginasISO 17025 2017 Training Course and Changessadbad6100% (4)

- A Guide To Pest Control in WarehousesDocumento21 páginasA Guide To Pest Control in Warehousessadbad6100% (3)

- Iso 22000 - Oprps Vs HaccpDocumento47 páginasIso 22000 - Oprps Vs Haccpsadbad667% (3)

- INTERNATIONALHandbook of Foodborne Pathogenes PDFDocumento809 páginasINTERNATIONALHandbook of Foodborne Pathogenes PDFsadbad6Ainda não há avaliações

- ISO 22000 Pauline JonesDocumento48 páginasISO 22000 Pauline Jonessadbad6100% (1)

- FSSC Auditor TrainingDocumento32 páginasFSSC Auditor Trainingsadbad6100% (3)

- ThermalDocumento51 páginasThermalsadbad6Ainda não há avaliações

- Sap MM - MRP - CBPDocumento2 páginasSap MM - MRP - CBPismailimran09Ainda não há avaliações

- Black Book ProjectDocumento55 páginasBlack Book ProjectTrupti Kuvalekar75% (4)

- Lethalityy Treatment Determination Calculating T Thermal Inactivation of PathogensDocumento14 páginasLethalityy Treatment Determination Calculating T Thermal Inactivation of Pathogenssadbad6Ainda não há avaliações

- How To Calculate F or P Values of Thermal Processes Using ExcelDocumento8 páginasHow To Calculate F or P Values of Thermal Processes Using Excelsadbad6Ainda não há avaliações

- F-Value Calculator - A Tool For Calculation of Acceptable F-Value in Canned Luncheon Meat Reduced in NaClDocumento4 páginasF-Value Calculator - A Tool For Calculation of Acceptable F-Value in Canned Luncheon Meat Reduced in NaClsadbad6Ainda não há avaliações

- L20 - Hani M - Al-Mazeedi Arabic English 2Documento101 páginasL20 - Hani M - Al-Mazeedi Arabic English 2sadbad6Ainda não há avaliações

- Webinar - FSSC 22000 Version 4Documento25 páginasWebinar - FSSC 22000 Version 4sadbad6100% (4)

- Certificate HalalDocumento9 páginasCertificate Halalsadbad6Ainda não há avaliações

- Processing of Pulp of Various Cultivars of Guava (Psidium Guajava L.) ForDocumento9 páginasProcessing of Pulp of Various Cultivars of Guava (Psidium Guajava L.) Forsadbad6Ainda não há avaliações

- Haacp For Be GainerDocumento36 páginasHaacp For Be Gainersadbad6Ainda não há avaliações

- Manvith 2nd Internal PPTDocumento10 páginasManvith 2nd Internal PPTMd NizamAinda não há avaliações

- Class No 14 & 15Documento31 páginasClass No 14 & 15WILD๛SHOTッ tanvirAinda não há avaliações

- Intelligent Manufacturing AutomationsDocumento15 páginasIntelligent Manufacturing AutomationsSazones Perú Gerardo SalazarAinda não há avaliações

- Kone Case WriteupDocumento7 páginasKone Case WriteupAnwesha RoyAinda não há avaliações

- Chapter-5: Accounting For Merchandising OperationsDocumento39 páginasChapter-5: Accounting For Merchandising OperationsNoel Buenafe JrAinda não há avaliações

- Marketing Management (Pricing Strategies)Documento17 páginasMarketing Management (Pricing Strategies)ketshepaone thekishoAinda não há avaliações

- 3 PDFDocumento2 páginas3 PDFAbdiasisAinda não há avaliações

- Solved at A Management Luncheon Two Managers Were Overheard Arguing AboutDocumento1 páginaSolved at A Management Luncheon Two Managers Were Overheard Arguing AboutM Bilal SaleemAinda não há avaliações

- Test Questions Chapter 11 DRS IBEO 12Documento20 páginasTest Questions Chapter 11 DRS IBEO 12mrscrouge100% (2)

- DELMIAWORKS Brochure 2019aDocumento11 páginasDELMIAWORKS Brochure 2019aVicente OrtizAinda não há avaliações

- Shipinvest4004 Introduction - Executive VersionDocumento30 páginasShipinvest4004 Introduction - Executive VersionDPR007Ainda não há avaliações

- Crisk MGMTDocumento39 páginasCrisk MGMTRavi GuptaAinda não há avaliações

- Product Strategies: Branding & Packaging DecisionsDocumento17 páginasProduct Strategies: Branding & Packaging Decisionsyeschowdhary6722Ainda não há avaliações

- Depreciation Provisions and Reserves Class 11 NotesDocumento48 páginasDepreciation Provisions and Reserves Class 11 Notesjainayan8190Ainda não há avaliações

- Example: Historical Financial StatementsDocumento10 páginasExample: Historical Financial StatementstopherxAinda não há avaliações

- Doc-20230305-Wa0030. 20231201 130624 0000Documento3 páginasDoc-20230305-Wa0030. 20231201 130624 0000H&M TRADERS INTERNATIONALAinda não há avaliações

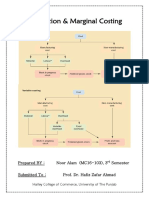

- Absorption & Marginal Costing - Noor Alam (MC16-103)Documento24 páginasAbsorption & Marginal Costing - Noor Alam (MC16-103)Ahmed Ali Khan100% (2)

- On December 1 2014 Fullerton Company Had The Following AccountDocumento2 páginasOn December 1 2014 Fullerton Company Had The Following AccountAmit PandeyAinda não há avaliações

- Global Credit Policy 2021 and Further Modifications KEDAR - 21.04.2022Documento9 páginasGlobal Credit Policy 2021 and Further Modifications KEDAR - 21.04.2022Rajkot academyAinda não há avaliações

- Syllabus 2021 IV SEM MGT 345 IMC April To July Semester Covid Short SemesterDocumento5 páginasSyllabus 2021 IV SEM MGT 345 IMC April To July Semester Covid Short SemesterSaurabh MishraAinda não há avaliações

- Pos Malaysia Value Chain & MoreDocumento2 páginasPos Malaysia Value Chain & Moremark_hew100% (1)

- Collection of RRLsDocumento14 páginasCollection of RRLsZedrielle MartinezAinda não há avaliações

- Galanz Assignment 2Documento16 páginasGalanz Assignment 2Richa ShahiAinda não há avaliações

- Concept of Merger Acquisation and AmalgamtionDocumento5 páginasConcept of Merger Acquisation and Amalgamtionbarkha chandnaAinda não há avaliações

- Merchandising Calender: By: Harsha Siddham Sanghamitra Kalita Sayantani SahaDocumento29 páginasMerchandising Calender: By: Harsha Siddham Sanghamitra Kalita Sayantani SahaSanghamitra KalitaAinda não há avaliações