Você também pode gostar

- India - Index of Industrial ProductionDocumento1 páginaIndia - Index of Industrial ProductionEduardo PetazzeAinda não há avaliações

- Turkey - Gross Domestic Product, Outlook 2016-2017Documento1 páginaTurkey - Gross Domestic Product, Outlook 2016-2017Eduardo PetazzeAinda não há avaliações

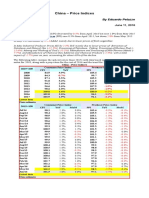

- China - Price IndicesDocumento1 páginaChina - Price IndicesEduardo PetazzeAinda não há avaliações

- Commitment of Traders - Futures Only Contracts - NYMEX (American)Documento1 páginaCommitment of Traders - Futures Only Contracts - NYMEX (American)Eduardo PetazzeAinda não há avaliações

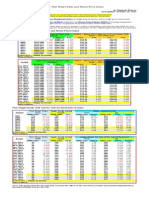

- U.S. New Home Sales and House Price IndexDocumento1 páginaU.S. New Home Sales and House Price IndexEduardo PetazzeAinda não há avaliações

- Germany - Renewable Energies ActDocumento1 páginaGermany - Renewable Energies ActEduardo PetazzeAinda não há avaliações

- Highlights, Wednesday June 8, 2016Documento1 páginaHighlights, Wednesday June 8, 2016Eduardo PetazzeAinda não há avaliações

- Reflections On The Greek Crisis and The Level of EmploymentDocumento1 páginaReflections On The Greek Crisis and The Level of EmploymentEduardo PetazzeAinda não há avaliações

- Analysis and Estimation of The US Oil ProductionDocumento1 páginaAnalysis and Estimation of The US Oil ProductionEduardo PetazzeAinda não há avaliações

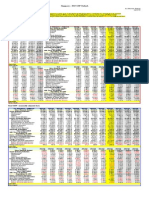

- WTI Spot PriceDocumento4 páginasWTI Spot PriceEduardo Petazze100% (1)

- China - Demand For Petroleum, Energy Efficiency and Consumption Per CapitaDocumento1 páginaChina - Demand For Petroleum, Energy Efficiency and Consumption Per CapitaEduardo PetazzeAinda não há avaliações

- U.S. Employment Situation - 2015 / 2017 OutlookDocumento1 páginaU.S. Employment Situation - 2015 / 2017 OutlookEduardo PetazzeAinda não há avaliações

- China - Power GenerationDocumento1 páginaChina - Power GenerationEduardo PetazzeAinda não há avaliações

- Singapore - 2015 GDP OutlookDocumento1 páginaSingapore - 2015 GDP OutlookEduardo PetazzeAinda não há avaliações

- India 2015 GDPDocumento1 páginaIndia 2015 GDPEduardo PetazzeAinda não há avaliações

- Japan, Population and Labour Force - 2015-2017 OutlookDocumento1 páginaJapan, Population and Labour Force - 2015-2017 OutlookEduardo PetazzeAinda não há avaliações

- South Africa - 2015 GDP OutlookDocumento1 páginaSouth Africa - 2015 GDP OutlookEduardo PetazzeAinda não há avaliações

- U.S. Federal Open Market Committee: Federal Funds RateDocumento1 páginaU.S. Federal Open Market Committee: Federal Funds RateEduardo PetazzeAinda não há avaliações

- Highlights in Scribd, Updated in April 2015Documento1 páginaHighlights in Scribd, Updated in April 2015Eduardo PetazzeAinda não há avaliações

- US Mining Production IndexDocumento1 páginaUS Mining Production IndexEduardo PetazzeAinda não há avaliações

- Mainland China - Interest Rates and InflationDocumento1 páginaMainland China - Interest Rates and InflationEduardo PetazzeAinda não há avaliações

- México, PBI 2015Documento1 páginaMéxico, PBI 2015Eduardo PetazzeAinda não há avaliações

- USA - Oil and Gas Extraction - Estimated Impact by Low Prices On Economic AggregatesDocumento1 páginaUSA - Oil and Gas Extraction - Estimated Impact by Low Prices On Economic AggregatesEduardo PetazzeAinda não há avaliações

- Brazilian Foreign TradeDocumento1 páginaBrazilian Foreign TradeEduardo PetazzeAinda não há avaliações

- European Commission, Spring 2015 Economic Forecast, Employment SituationDocumento1 páginaEuropean Commission, Spring 2015 Economic Forecast, Employment SituationEduardo PetazzeAinda não há avaliações

- South Korea, Monthly Industrial StatisticsDocumento1 páginaSouth Korea, Monthly Industrial StatisticsEduardo PetazzeAinda não há avaliações

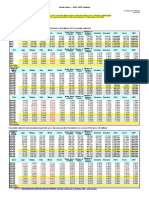

- Chile, Monthly Index of Economic Activity, IMACECDocumento2 páginasChile, Monthly Index of Economic Activity, IMACECEduardo PetazzeAinda não há avaliações

- Japan, Indices of Industrial ProductionDocumento1 páginaJapan, Indices of Industrial ProductionEduardo PetazzeAinda não há avaliações

- US - Personal Income and Outlays - 2015-2016 OutlookDocumento1 páginaUS - Personal Income and Outlays - 2015-2016 OutlookEduardo PetazzeAinda não há avaliações

- United States - Gross Domestic Product by IndustryDocumento1 páginaUnited States - Gross Domestic Product by IndustryEduardo PetazzeAinda não há avaliações

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5784)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- THE IMPACT OF INFLATION CRISIS ON SMALL ENTERPRISES AT SANTOS Updated 3potanginaDocumento20 páginasTHE IMPACT OF INFLATION CRISIS ON SMALL ENTERPRISES AT SANTOS Updated 3potanginaNormi Anne TuazonAinda não há avaliações

- AP Macroeconomics Practice Exam 2 Multiple Choice QuestionsDocumento18 páginasAP Macroeconomics Practice Exam 2 Multiple Choice QuestionsKayAinda não há avaliações

- Choose Yourself - Altucher JamesDocumento151 páginasChoose Yourself - Altucher JamesHoa Tử Đằng100% (4)

- Universal Robina CorporationDocumento2 páginasUniversal Robina CorporationAshlley Nicole VillaranAinda não há avaliações

- SFVJD - Acord de Parteneriat OficialDocumento293 páginasSFVJD - Acord de Parteneriat OficialBranza TelemeaAinda não há avaliações

- DOT: Value of A Statistical Life Guidance, 2016 RevisedDocumento13 páginasDOT: Value of A Statistical Life Guidance, 2016 RevisedWUSA9-TVAinda não há avaliações

- Contractor pricing guidanceDocumento11 páginasContractor pricing guidanceKyle MoolmanAinda não há avaliações

- BBS 2nd Year Syllabus and Mode654432Documento26 páginasBBS 2nd Year Syllabus and Mode654432DiNesh Prajapati50% (2)

- Ltcma Full ReportDocumento150 páginasLtcma Full ReportJuan José Solis DelgadoAinda não há avaliações

- Modern Monetary Theory and Practice An Introductory by William Mitchell, L. Randall Wray, Martin Watts PDFDocumento397 páginasModern Monetary Theory and Practice An Introductory by William Mitchell, L. Randall Wray, Martin Watts PDFAhmed DanafAinda não há avaliações

- BFC5935 - Tutorial 1 Solutions PDFDocumento7 páginasBFC5935 - Tutorial 1 Solutions PDFXue Xu100% (1)

- Demonetization: Impact On Major Macroeconomic Variables: Komal Kanwar Shekhawat and Neha JainDocumento4 páginasDemonetization: Impact On Major Macroeconomic Variables: Komal Kanwar Shekhawat and Neha JainNeha JainAinda não há avaliações

- Insurance Industry Analysis March 2013Documento34 páginasInsurance Industry Analysis March 2013Pieter NoppeAinda não há avaliações

- Add Maths ProjectDocumento18 páginasAdd Maths ProjectPuvan66Ainda não há avaliações

- Empirical Statistics Related To Trade Flow: Submitted To: Rashmi Ma'am Submitted By: Salil TimsinaDocumento25 páginasEmpirical Statistics Related To Trade Flow: Submitted To: Rashmi Ma'am Submitted By: Salil TimsinaSalil TimsinaAinda não há avaliações

- DU Finance BBA Course PlanDocumento31 páginasDU Finance BBA Course PlanToxicant GamerAinda não há avaliações

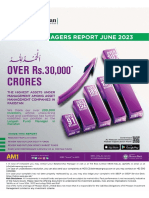

- Fund Manager's Report - JUNE 2023Documento35 páginasFund Manager's Report - JUNE 2023smartboy.sb06Ainda não há avaliações

- Ekonomi Makro Pertemuan Ke 8Documento14 páginasEkonomi Makro Pertemuan Ke 8ariel mahardikaAinda não há avaliações

- Baldacci - Cyclicality of Fiscal Policy in IndonesiaDocumento31 páginasBaldacci - Cyclicality of Fiscal Policy in IndonesiamirzalinaAinda não há avaliações

- Relationship Between Inflation and Foreign TradeDocumento7 páginasRelationship Between Inflation and Foreign TradeInternational Journal of Business Marketing and ManagementAinda não há avaliações

- Middle EastDocumento130 páginasMiddle EastmalshayefAinda não há avaliações

- 2017 11 Economics Sample Paper 02 Ans Ot8ebDocumento5 páginas2017 11 Economics Sample Paper 02 Ans Ot8ebramukolakiAinda não há avaliações

- Bangko Sentral's Role in Monetary PolicyDocumento15 páginasBangko Sentral's Role in Monetary PolicyLaezelie SorianoAinda não há avaliações

- Banking MCQ by Mahindra PDFDocumento57 páginasBanking MCQ by Mahindra PDFHaseebAinda não há avaliações

- Principles of Economics 1St Edition Asarta Test Bank Full Chapter PDFDocumento68 páginasPrinciples of Economics 1St Edition Asarta Test Bank Full Chapter PDFmohurrum.ginkgo.iabwuz100% (6)

- PNADF350Documento47 páginasPNADF350joaozinho fgawAinda não há avaliações

- Chapter 1 Ten Principles of EconomicsDocumento29 páginasChapter 1 Ten Principles of EconomicsSharon YuAinda não há avaliações

- Memorandum Train LawDocumento23 páginasMemorandum Train LawKweeng Tayrus FaelnarAinda não há avaliações

- PSSC Economics QPDocumento43 páginasPSSC Economics QPAndrew ArahaAinda não há avaliações

- Strategic management of tourism industryDocumento22 páginasStrategic management of tourism industryTapan RathAinda não há avaliações