Você também pode gostar

- Set Off & Carry Forward of LossesDocumento21 páginasSet Off & Carry Forward of LossesanchalAinda não há avaliações

- Set Off & Carry Forward of LossesDocumento17 páginasSet Off & Carry Forward of Lossesabdulraqeeb alareqiAinda não há avaliações

- Set-Off and Carry ForwardDocumento3 páginasSet-Off and Carry ForwardAnu KAinda não há avaliações

- Set Off and Carry ForwardDocumento3 páginasSet Off and Carry ForwardAnjali Krishna SAinda não há avaliações

- 1.inter-Source Set-Off: Sec 70 Loss From One Source of Income Can Be Set-Off AgainstDocumento2 páginas1.inter-Source Set-Off: Sec 70 Loss From One Source of Income Can Be Set-Off AgainstHarshithaAinda não há avaliações

- Set of Carry ForwardDocumento4 páginasSet of Carry ForwardShobhit ShuklaAinda não há avaliações

- Set Off and Carry Forward of Losses Are Covered Under Income Tax Act 1961 From Section 70 To 74Documento7 páginasSet Off and Carry Forward of Losses Are Covered Under Income Tax Act 1961 From Section 70 To 74Venugopal MantraratnamAinda não há avaliações

- 18887sm DTL Finalnew Cp10Documento16 páginas18887sm DTL Finalnew Cp10Ravee MishraAinda não há avaliações

- 29 Carry Forward and Set Off of Losses in Case of Certain CompaniesDocumento13 páginas29 Carry Forward and Set Off of Losses in Case of Certain CompaniesSeiya KapahiAinda não há avaliações

- Set Off and Carry Forward of LossesDocumento16 páginasSet Off and Carry Forward of LossesDivyansh JaiswalAinda não há avaliações

- Taxation General RulesDocumento7 páginasTaxation General RulesAnurag BhardwajAinda não há avaliações

- Ganesh Siddheshwar Mba Ii (Financial Management)Documento22 páginasGanesh Siddheshwar Mba Ii (Financial Management)ganesh_sidAinda não há avaliações

- TTP Unit IVDocumento19 páginasTTP Unit IVAmandeep KaurAinda não há avaliações

- Setoff & Carry Forward of LossDocumento3 páginasSetoff & Carry Forward of LossDr. Mustafa KozhikkalAinda não há avaliações

- HW 24371Documento50 páginasHW 24371Allen RaoAinda não há avaliações

- Set Off and Carry Forward Off Losses PDFDocumento5 páginasSet Off and Carry Forward Off Losses PDFMuhammad sheran sattiAinda não há avaliações

- 6.set OffDocumento39 páginas6.set OffSruthi NairAinda não há avaliações

- Set Off and Carry ForwardDocumento4 páginasSet Off and Carry ForwardAmit Roy100% (1)

- Set Off and Carry Forward of Losses Under Income Tax Act 1961Documento5 páginasSet Off and Carry Forward of Losses Under Income Tax Act 1961Abhay KushwahaAinda não há avaliações

- It 5 Set OffDocumento2 páginasIt 5 Set Offmohammadrafeeqj7Ainda não há avaliações

- Tax Planning With Respect To Amalgamation and MergersDocumento29 páginasTax Planning With Respect To Amalgamation and MergerssadathnooriAinda não há avaliações

- Article On Set-Off and Carry-Forward of The Losses Under The Income-Tax Act, 1961Documento5 páginasArticle On Set-Off and Carry-Forward of The Losses Under The Income-Tax Act, 1961Ravi ChandraAinda não há avaliações

- Set Off & Carry FWDDocumento1 páginaSet Off & Carry FWDmushfeqaAinda não há avaliações

- Set Off and Carry Forward of LossesDocumento3 páginasSet Off and Carry Forward of LossesAdeem Ashrafi0% (1)

- Capital Gain TaxationDocumento6 páginasCapital Gain TaxationYuvi SinghAinda não há avaliações

- Set Off Carried Forward of LossesDocumento32 páginasSet Off Carried Forward of Lossesabhirocks_bigjAinda não há avaliações

- ET OFF Arry Forward OF LossesDocumento9 páginasET OFF Arry Forward OF LossesrajeevmbaAinda não há avaliações

- Set Off and Carry Forward of LossesDocumento5 páginasSet Off and Carry Forward of LossesRohansh AroraAinda não há avaliações

- Setoff and Carry ForwardDocumento2 páginasSetoff and Carry Forwardsatyamgupta96666Ainda não há avaliações

- 31170sm DTL Finalnew-May-Nov14 Cp10Documento16 páginas31170sm DTL Finalnew-May-Nov14 Cp10gvcAinda não há avaliações

- List of TablesDocumento4 páginasList of TablesRavi ChandraAinda não há avaliações

- Set Off and Carry Forward of Losses 1218288118076384 8Documento26 páginasSet Off and Carry Forward of Losses 1218288118076384 8jui999Ainda não há avaliações

- 21 - MCQ Set Off and Carry FRWRDDocumento10 páginas21 - MCQ Set Off and Carry FRWRDvipul singhAinda não há avaliações

- Aggregation of Income, Set-Off and Carry Forward of LossesDocumento18 páginasAggregation of Income, Set-Off and Carry Forward of LossesJoseph SalidoAinda não há avaliações

- Set Off & Carry Forward of LossesDocumento4 páginasSet Off & Carry Forward of LossesdamspraveenAinda não há avaliações

- Set-Off and Carry Forward Losses-1Documento9 páginasSet-Off and Carry Forward Losses-1bipin3737Ainda não há avaliações

- Unit 4.2 Income TaxDocumento5 páginasUnit 4.2 Income TaxSAMIR AHMEDAinda não há avaliações

- 21 - MCQ Set Off and Carry ForwardDocumento9 páginas21 - MCQ Set Off and Carry ForwardSajid YaqoobAinda não há avaliações

- Set Off ChapterDocumento4 páginasSet Off ChapterManohar LalAinda não há avaliações

- Set Off and Carry Forward of The Losses-IMISDocumento23 páginasSet Off and Carry Forward of The Losses-IMISMegha MoonkaAinda não há avaliações

- Chapter-6 Set Off and Carry Forward of LossesDocumento7 páginasChapter-6 Set Off and Carry Forward of LossesSumon iqbalAinda não há avaliações

- 040 - Sujal JainDocumento9 páginas040 - Sujal Jainsujal JainAinda não há avaliações

- 21 - MCQ Set Off and Carry FRWRDDocumento10 páginas21 - MCQ Set Off and Carry FRWRDParth UpadhyayAinda não há avaliações

- ACFrOgAgAvlOk8V3KkRXNOd4ZYgPkBKkC-PF6aWUwz0mZvSZEDfOMTgftx So R2VKRRRQROw0Qw2SmvcOS84GhhNLahOUUiXCF6g XTlg4DCLM30fidg16h1U97is5Xo ysVHiCOQ20Pn7RkGljDocumento10 páginasACFrOgAgAvlOk8V3KkRXNOd4ZYgPkBKkC-PF6aWUwz0mZvSZEDfOMTgftx So R2VKRRRQROw0Qw2SmvcOS84GhhNLahOUUiXCF6g XTlg4DCLM30fidg16h1U97is5Xo ysVHiCOQ20Pn7RkGljManleen KaurAinda não há avaliações

- Set of or Carry-11Documento11 páginasSet of or Carry-11s4sahithAinda não há avaliações

- Set Off and Carry ForwardDocumento16 páginasSet Off and Carry Forwarddhwani shahAinda não há avaliações

- Fin. Acounting Project 2022Documento14 páginasFin. Acounting Project 2022Sahil ParmarAinda não há avaliações

- (Section 72) - Carry Forward and Set Off of BusinesDocumento3 páginas(Section 72) - Carry Forward and Set Off of Businessukantabera215Ainda não há avaliações

- Unit 3 Set Off and Carry ForwardDocumento17 páginasUnit 3 Set Off and Carry ForwardAnshu kumarAinda não há avaliações

- TAXATION LAW II (Notes For Exams)Documento59 páginasTAXATION LAW II (Notes For Exams)MrinalBhatnagarAinda não há avaliações

- Set Off & Carry Forward of Losses: Lecture NotesDocumento45 páginasSet Off & Carry Forward of Losses: Lecture Notesapi-3832224100% (1)

- Setoff & CFDocumento21 páginasSetoff & CFwasim_lokAinda não há avaliações

- Indirect Tax AssignmentDocumento3 páginasIndirect Tax AssignmentNitesh ShendeAinda não há avaliações

- Set OffDocumento9 páginasSet OffAditya MehtaniAinda não há avaliações

- Business TaxationDocumento14 páginasBusiness TaxationDisha PoptaniAinda não há avaliações

- Set OffDocumento29 páginasSet OffManoj KuttyAinda não há avaliações

- Set Off & Carry Forward of Losses: Lecture NotesDocumento22 páginasSet Off & Carry Forward of Losses: Lecture Notessantoshsa_1987Ainda não há avaliações

- Net Operating Loss Tax Loss Carryback Net Operating LossDocumento9 páginasNet Operating Loss Tax Loss Carryback Net Operating Lossamar_aliveAinda não há avaliações

- Advanced Rulings - Income Tax PDFDocumento222 páginasAdvanced Rulings - Income Tax PDFAbhishek Sharma0% (1)

- Section Article 14 Bench Strength 8............................................. This Article Corresponds To The EqualDocumento34 páginasSection Article 14 Bench Strength 8............................................. This Article Corresponds To The EqualAbhishek SharmaAinda não há avaliações

- Circumstantial EvidenceDocumento12 páginasCircumstantial EvidenceAbhishek SharmaAinda não há avaliações

- SC-UoI Panel 11.12.14Documento29 páginasSC-UoI Panel 11.12.14Abhishek SharmaAinda não há avaliações

- Appreciation of Evidence CriminalDocumento18 páginasAppreciation of Evidence CriminalAbhishek SharmaAinda não há avaliações

- Bail & Anticipatory BailDocumento76 páginasBail & Anticipatory BailAbhishek SharmaAinda não há avaliações

- Signature Not VerifiedDocumento28 páginasSignature Not VerifiedAbhishek SharmaAinda não há avaliações

- Proforma For Mentioning1Documento1 páginaProforma For Mentioning1Abhishek SharmaAinda não há avaliações

- Sl. No. Legislative Power Bench StrengthDocumento6 páginasSl. No. Legislative Power Bench StrengthAbhishek SharmaAinda não há avaliações

- Principle of ParityDocumento4 páginasPrinciple of ParityAbhishek SharmaAinda não há avaliações

- 227 239 251Documento55 páginas227 239 251Abhishek SharmaAinda não há avaliações

- Computation of Total Income and Tax LiabilityDocumento2 páginasComputation of Total Income and Tax LiabilityAbhishek SharmaAinda não há avaliações

- Sl. No. S.173, Code of Criminal Procedure Bench Streng TH 11. When A Report Forwarded by The Police To The MagistrateDocumento9 páginasSl. No. S.173, Code of Criminal Procedure Bench Streng TH 11. When A Report Forwarded by The Police To The MagistrateAbhishek SharmaAinda não há avaliações

- Bar Council of India Rules, Part V OnwardsDocumento102 páginasBar Council of India Rules, Part V OnwardsAbhishek Sharma100% (1)

- IPO ProcedureDocumento2 páginasIPO ProcedureAbhishek SharmaAinda não há avaliações

- Excise BookDocumento70 páginasExcise BookAbhishek SharmaAinda não há avaliações

- 320 - 482Documento35 páginas320 - 482Abhishek SharmaAinda não há avaliações

- Punjab and Haryana High Court Rules Volume IVDocumento483 páginasPunjab and Haryana High Court Rules Volume IVAbhishek SharmaAinda não há avaliações

- Foreign Exchange Management Act The RestrictionDocumento2 páginasForeign Exchange Management Act The RestrictionAbhishek SharmaAinda não há avaliações

- Gauhati High Court Judgement - CBI UnconstitutionalDocumento89 páginasGauhati High Court Judgement - CBI UnconstitutionalSuresh NakhuaAinda não há avaliações

- General Elections 2014 Detailed NotificationDocumento85 páginasGeneral Elections 2014 Detailed NotificationAbhishek SharmaAinda não há avaliações

- Supreme Court Rules 2013Documento106 páginasSupreme Court Rules 2013Abhishek SharmaAinda não há avaliações

- Bombay High Court Original Side FormsDocumento147 páginasBombay High Court Original Side FormsAbhishek Sharma100% (2)

- Delhi High Court RulesDocumento1.468 páginasDelhi High Court RulesAbhishek SharmaAinda não há avaliações

- Bombay High Court Original Side RulesDocumento308 páginasBombay High Court Original Side RulesAbhishek Sharma92% (12)

- Bombay High Court Appellate Side RulesDocumento198 páginasBombay High Court Appellate Side RulesAbhishek Sharma50% (4)

- Advocate-on-Record Name Lending Judgment.Documento18 páginasAdvocate-on-Record Name Lending Judgment.Abhishek SharmaAinda não há avaliações

- Multi Page PDFDocumento164 páginasMulti Page PDFAung Zaw HtweAinda não há avaliações

- State Money Transmission Laws vs. Bitcoins: Protecting Consumers or Hindering Innovation?Documento30 páginasState Money Transmission Laws vs. Bitcoins: Protecting Consumers or Hindering Innovation?boyburger17Ainda não há avaliações

- Institute of Rural Management AnandDocumento6 páginasInstitute of Rural Management AnandIndiaresultAinda não há avaliações

- Partnership AccountingDocumento18 páginasPartnership AccountingSani ModiAinda não há avaliações

- Cavite Development vs. Spouses LimDocumento1 páginaCavite Development vs. Spouses LimXel PamisaranAinda não há avaliações

- Interview Letter From Tata Group - For Fist Batch - 011 PDFDocumento3 páginasInterview Letter From Tata Group - For Fist Batch - 011 PDFritesh shrivastavAinda não há avaliações

- Financial Market SummaryDocumento21 páginasFinancial Market SummaryJorufel Tomo PapasinAinda não há avaliações

- Framework: General Concepts Life Insurance Non-Life InsuranceDocumento215 páginasFramework: General Concepts Life Insurance Non-Life InsuranceDevilleres Eliza DenAinda não há avaliações

- The IB League Case StudyDocumento6 páginasThe IB League Case StudyNidhi KumarAinda não há avaliações

- Housing LoanDocumento36 páginasHousing LoanHabeeb UppinangadyAinda não há avaliações

- eFinancialCareers - Careers in Financial MarketsDocumento100 páginaseFinancialCareers - Careers in Financial MarketsAlex SartwitzAinda não há avaliações

- A Study On Customer Satisfaction of Reliance Life Insurance at HyderabadDocumento8 páginasA Study On Customer Satisfaction of Reliance Life Insurance at Hyderabads_kumaresh_raghavanAinda não há avaliações

- Chapter - 14 SummaryDocumento3 páginasChapter - 14 SummaryShyamsunder SinghAinda não há avaliações

- Banking FDDocumento17 páginasBanking FDKumar SouravAinda não há avaliações

- Bni PT Bangun Apr22Documento2 páginasBni PT Bangun Apr22Yehezkiel AdhiAinda não há avaliações

- Ar Questions in Negotiable InstrumentDocumento9 páginasAr Questions in Negotiable InstrumentAtty AnnaAinda não há avaliações

- Account Statement From 1 Jan 2019 To 31 Dec 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento11 páginasAccount Statement From 1 Jan 2019 To 31 Dec 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceKrishna YadavAinda não há avaliações

- Comparative Study of Education Loan Between Sbi and IciciDocumento82 páginasComparative Study of Education Loan Between Sbi and IciciAvtaar Singh50% (2)

- Nods02052014 Feb 12 2014Documento63 páginasNods02052014 Feb 12 2014Kasey JohnsonAinda não há avaliações

- Nigeria Visa ApplicationDocumento2 páginasNigeria Visa ApplicationVishalAinda não há avaliações

- Unit 3. Procedure For Opening & Operating of Deposit AccountDocumento11 páginasUnit 3. Procedure For Opening & Operating of Deposit AccountBhagyesh ThakurAinda não há avaliações

- Landmark Cases in The Law of Contract Order FormDocumento4 páginasLandmark Cases in The Law of Contract Order Formshahbaz_malbari_bballb13Ainda não há avaliações

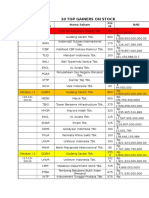

- 10 Top Gainers On Stock: Bulan/Min Ggu Kode Saham Nama Saham Poi NT NABDocumento6 páginas10 Top Gainers On Stock: Bulan/Min Ggu Kode Saham Nama Saham Poi NT NABFajRin WiCaksonoAinda não há avaliações

- Credit Helper: The Complete Credit Restoration Guide & Pre-Typed Legal Letter SystemDocumento40 páginasCredit Helper: The Complete Credit Restoration Guide & Pre-Typed Legal Letter SystemTori Grayer100% (2)

- Internship Report On "Customer Satisfaction of Jamuna Bank Limited"Documento62 páginasInternship Report On "Customer Satisfaction of Jamuna Bank Limited"shakilhm0% (1)

- How To Prepare For A Transfer Pricing AuditDocumento7 páginasHow To Prepare For A Transfer Pricing Auditmejocoba82Ainda não há avaliações

- SWIFT MessagesDocumento521 páginasSWIFT Messagesashish_scribd_23Ainda não há avaliações

- A & C Report of CLZDocumento86 páginasA & C Report of CLZSubhas MishraAinda não há avaliações

- Annual Report 2005 06Documento70 páginasAnnual Report 2005 06mrkeralaAinda não há avaliações

- ICOBSDocumento124 páginasICOBS1474543Ainda não há avaliações