Você também pode gostar

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- India Equity Analytics Today: Buy Stock of KPIT TechDocumento24 páginasIndia Equity Analytics Today: Buy Stock of KPIT TechNarnolia Securities LimitedAinda não há avaliações

- Nse's Certification in Financial Markets - Options Trading StrategiesDocumento60 páginasNse's Certification in Financial Markets - Options Trading Strategiessachindravid100% (1)

- Securities Market Module - NCFM PDFDocumento216 páginasSecurities Market Module - NCFM PDFGulshan KumarAinda não há avaliações

- Bankers ListDocumento2 páginasBankers ListRohit ChhabraAinda não há avaliações

- TFS New 22Documento2.385 páginasTFS New 22darshil thakkerAinda não há avaliações

- India Equity Analytics Today: Buy Stock of Hindalco Industries LTDDocumento21 páginasIndia Equity Analytics Today: Buy Stock of Hindalco Industries LTDNarnolia Securities LimitedAinda não há avaliações

- Stock Advisory For Today - Buy Stock of Indusind BankDocumento22 páginasStock Advisory For Today - Buy Stock of Indusind BankNarnolia Securities LimitedAinda não há avaliações

- Stock Recommendation For Today: Buy Stock of PNB and Neutral View On Jindal Steel & PowerDocumento21 páginasStock Recommendation For Today: Buy Stock of PNB and Neutral View On Jindal Steel & PowerNarnolia Securities LimitedAinda não há avaliações

- Investment Funds Advisory For Today: Buy Stock of Coal India LTD.Documento22 páginasInvestment Funds Advisory For Today: Buy Stock of Coal India LTD.Narnolia Securities LimitedAinda não há avaliações

- Stock Recommendation For Today: Buy Stock of TCS and Hold HDFC Bank ShareDocumento24 páginasStock Recommendation For Today: Buy Stock of TCS and Hold HDFC Bank ShareNarnolia Securities LimitedAinda não há avaliações

- Commodity Price of Gold, Sliver, Copper, Doller/rs and Many More. Narnolia Securities Limited Market Diary 13.03.2014Documento5 páginasCommodity Price of Gold, Sliver, Copper, Doller/rs and Many More. Narnolia Securities Limited Market Diary 13.03.2014Narnolia Securities LimitedAinda não há avaliações

- Advice To Investor Today: Hold The Stock of ICIC Bank and Book Profit On ACC LimitedDocumento25 páginasAdvice To Investor Today: Hold The Stock of ICIC Bank and Book Profit On ACC LimitedNarnolia Securities LimitedAinda não há avaliações

- Investment Funds Advisory For Today: Buy Stock of HCL Tech Due To Healthy Earnings PerformanceDocumento26 páginasInvestment Funds Advisory For Today: Buy Stock of HCL Tech Due To Healthy Earnings PerformanceNarnolia Securities LimitedAinda não há avaliações

- Stock Advisory For Today: Book Profit On Persistent System StockDocumento5 páginasStock Advisory For Today: Book Profit On Persistent System StockNarnolia Securities LimitedAinda não há avaliações

- Stock Porfolio Advisory For Today: Buy Stock of Shakti Pumps (India) LTD With Price Target of Rs. 105Documento26 páginasStock Porfolio Advisory For Today: Buy Stock of Shakti Pumps (India) LTD With Price Target of Rs. 105Narnolia Securities LimitedAinda não há avaliações

- India Equity Analytics Today:Buy Stock of Tata Steel LTD, V-Guard Industries LTD and InfosysDocumento21 páginasIndia Equity Analytics Today:Buy Stock of Tata Steel LTD, V-Guard Industries LTD and InfosysNarnolia Securities LimitedAinda não há avaliações

- Stock Advisory For Today - Buy Stock of Bank of BarodaDocumento26 páginasStock Advisory For Today - Buy Stock of Bank of BarodaNarnolia Securities LimitedAinda não há avaliações

- See The Chart of Indian Industrial Growth Trend Q3FY14 in Narnolia Securities Limited Market Diary 10.03.2014Documento5 páginasSee The Chart of Indian Industrial Growth Trend Q3FY14 in Narnolia Securities Limited Market Diary 10.03.2014Narnolia Securities LimitedAinda não há avaliações

- India Equity Analytics Today: Hold Rating On Prestige Estates StockDocumento25 páginasIndia Equity Analytics Today: Hold Rating On Prestige Estates StockNarnolia Securities LimitedAinda não há avaliações

- Commodity Price of #Gold, #Sliver, #Copper, #Doller/rs and Many More. Narnolia Securities Limited Market Diary 03.03.2014Documento4 páginasCommodity Price of #Gold, #Sliver, #Copper, #Doller/rs and Many More. Narnolia Securities Limited Market Diary 03.03.2014Narnolia Securities LimitedAinda não há avaliações

- What Is Foreign Currency Reserves (US$ BN) & Exchange Rate? See This Chart in Narnolia Securities Limited Market Diary 11.03.2014Documento5 páginasWhat Is Foreign Currency Reserves (US$ BN) & Exchange Rate? See This Chart in Narnolia Securities Limited Market Diary 11.03.2014Narnolia Securities LimitedAinda não há avaliações

- Get Daily Update About Nifty, Sensex, DOW, NASDAQ, CAC, DAX, FTSE, NIKKIE, HANG SENG, and EW ALL SHARE. Narnolia Securities Limited Market Diary 06.03.2014Documento5 páginasGet Daily Update About Nifty, Sensex, DOW, NASDAQ, CAC, DAX, FTSE, NIKKIE, HANG SENG, and EW ALL SHARE. Narnolia Securities Limited Market Diary 06.03.2014Narnolia Securities LimitedAinda não há avaliações

- Commodity Price of Gold, Sliver, Copper, Doller/rs and Many More. Narnolia Securities Limited Market Diary 07.03.201Documento5 páginasCommodity Price of Gold, Sliver, Copper, Doller/rs and Many More. Narnolia Securities Limited Market Diary 07.03.201Narnolia Securities LimitedAinda não há avaliações

- Commodity Price of Gold, Sliver, Copper, Doller/rs and Many More. Narnolia Securities Limited Market Diary 07.03.201Documento5 páginasCommodity Price of Gold, Sliver, Copper, Doller/rs and Many More. Narnolia Securities Limited Market Diary 07.03.201Narnolia Securities LimitedAinda não há avaliações

- Investment Funds Advisory For Today: Buy Stock of Powergrid and IFGL Refractories LTDDocumento23 páginasInvestment Funds Advisory For Today: Buy Stock of Powergrid and IFGL Refractories LTDNarnolia Securities LimitedAinda não há avaliações

- Fund Portfolio For Today: Public Sector Banks Result Review 3QFY14Documento28 páginasFund Portfolio For Today: Public Sector Banks Result Review 3QFY14Narnolia Securities LimitedAinda não há avaliações

- Investing in Shares For Today:Buy Stock of Hindustan Zinc LTD and Book Profit On Swaraj Engines LTDDocumento18 páginasInvesting in Shares For Today:Buy Stock of Hindustan Zinc LTD and Book Profit On Swaraj Engines LTDNarnolia Securities LimitedAinda não há avaliações

- India Equity Analytics: Buy Stock of Eros Media and Escorts LTDDocumento21 páginasIndia Equity Analytics: Buy Stock of Eros Media and Escorts LTDNarnolia Securities LimitedAinda não há avaliações

- See Chart of HSBC Manufacturing PMI No and Index Action-Nifty in Narnolia Securities Limited Market Diary 04.03.2014Documento5 páginasSee Chart of HSBC Manufacturing PMI No and Index Action-Nifty in Narnolia Securities Limited Market Diary 04.03.2014Narnolia Securities LimitedAinda não há avaliações

- Look at Nifty SNAPSHOT Snapshot where you get details of Nifty Mar and Apr 2013 Future, Nifty Mar 2013 Open Interest, 7 DMA of Spot Nifty and Put call Ratio. Narnolia Securities Limited Market Diary 05.03.2014Documento5 páginasLook at Nifty SNAPSHOT Snapshot where you get details of Nifty Mar and Apr 2013 Future, Nifty Mar 2013 Open Interest, 7 DMA of Spot Nifty and Put call Ratio. Narnolia Securities Limited Market Diary 05.03.2014Narnolia Securities LimitedAinda não há avaliações

- See The Chart of Indian Bond MKT & Sensex Trend in Narnolia Securities Limited Market Diary 26.02.2014Documento5 páginasSee The Chart of Indian Bond MKT & Sensex Trend in Narnolia Securities Limited Market Diary 26.02.2014Narnolia Securities LimitedAinda não há avaliações

- India Equity Analytics Today: Book Profit On Shree Cement and Axis Bank StockDocumento31 páginasIndia Equity Analytics Today: Book Profit On Shree Cement and Axis Bank StockNarnolia Securities LimitedAinda não há avaliações

- Suggested Topics For Research (M. Com: Advanced Accounting, Auditing and Taxation)Documento3 páginasSuggested Topics For Research (M. Com: Advanced Accounting, Auditing and Taxation)nehaAinda não há avaliações

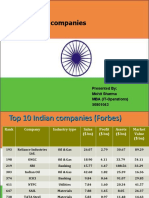

- Top 5 Indian Companies: Presented By: Mohit Sharma MBA (IT-Operations) 50801043Documento18 páginasTop 5 Indian Companies: Presented By: Mohit Sharma MBA (IT-Operations) 50801043Manu SharmaAinda não há avaliações

- Online Trading FM AssignmentDocumento20 páginasOnline Trading FM AssignmentRudraksh PareyAinda não há avaliações

- PS2023Documento50 páginasPS2023Lucky PrinceAinda não há avaliações

- Devyani International Limited - Initial Public Offer - R: Common Bid Cum Application FormDocumento12 páginasDevyani International Limited - Initial Public Offer - R: Common Bid Cum Application FormAbisekAinda não há avaliações

- Asset Size 31 03 2021 100cr AboveDocumento2 páginasAsset Size 31 03 2021 100cr Aboveravi ohlyanAinda não há avaliações

- BCL Industries LTD: Videos Images Maps News Shopping Books Flights Search ToolsDocumento5 páginasBCL Industries LTD: Videos Images Maps News Shopping Books Flights Search ToolsManish SinghAinda não há avaliações

- Nifty DDKDK LFKDSFSDKFDK KF Sdkfdlsfkldskfds LLFKSLDLFKSLD KF DSKL FKLDSK Fks DKFKDKFKKF DSKFL DSFK LDSFK LKF LDK Lks LK K LK DK LL K LK KDocumento42 páginasNifty DDKDK LFKDSFSDKFDK KF Sdkfdlsfkldskfds LLFKSLDLFKSLD KF DSKL FKLDSK Fks DKFKDKFKKF DSKFL DSFK LDSFK LKF LDK Lks LK K LK DK LL K LK KVikas RockAinda não há avaliações

- Summer Black BookDocumento46 páginasSummer Black BookAvinash KarkhileAinda não há avaliações

- Tin Plate India Ltd Research Report AnalysisDocumento8 páginasTin Plate India Ltd Research Report AnalysisPriyank PatelAinda não há avaliações

- Indus Equity Advisors Pvt Ltd NSE/BSE Delivery Position as on 05/11/2020Documento22 páginasIndus Equity Advisors Pvt Ltd NSE/BSE Delivery Position as on 05/11/2020Vimal SharmaAinda não há avaliações

- SAUDA DETAIL REPORT cl3618 PDFDocumento1 páginaSAUDA DETAIL REPORT cl3618 PDFPrachi PatwariAinda não há avaliações

- Nodalofficers 26102020Documento270 páginasNodalofficers 26102020Abhijeet AnkushAinda não há avaliações

- Visualizing and Forecasting Stocks: Submitted in Partial Fulfillment of The Requirement of For The Degree ofDocumento31 páginasVisualizing and Forecasting Stocks: Submitted in Partial Fulfillment of The Requirement of For The Degree ofAinul AlamAinda não há avaliações

- Akhil K Bse Nse Indo NextDocumento18 páginasAkhil K Bse Nse Indo Nextakhil kAinda não há avaliações

- HPC StockDocumento18 páginasHPC StockSneha SahaAinda não há avaliações

- SEBI Handbook 15Documento216 páginasSEBI Handbook 15adoniscalAinda não há avaliações

- Chapter 10 Index Number QMDocumento24 páginasChapter 10 Index Number QMReya BardhanAinda não há avaliações

- HDFC Bank Limited - Placement Document - Feb 2015 PDFDocumento589 páginasHDFC Bank Limited - Placement Document - Feb 2015 PDFpriyadarshiniAinda não há avaliações

- Risk Return Anaysis of Telecom CompaniesDocumento79 páginasRisk Return Anaysis of Telecom CompaniesAkash Venugopal0% (1)

- Learn about Indian stock exchanges, NSE, SHCIL and key conceptsDocumento55 páginasLearn about Indian stock exchanges, NSE, SHCIL and key conceptsKavita GarkotiAinda não há avaliações

- Updates On Open Offer (Company Update)Documento80 páginasUpdates On Open Offer (Company Update)Shyam SunderAinda não há avaliações

- Imagine Marketing Limited DRHPDocumento394 páginasImagine Marketing Limited DRHPResham FililiAinda não há avaliações

- Evaluation of Investor Awareness On Techniques UseDocumento12 páginasEvaluation of Investor Awareness On Techniques UseRonat JainAinda não há avaliações

- Bayer Cropscience - 4QFY19 Result - Kotak PDFDocumento6 páginasBayer Cropscience - 4QFY19 Result - Kotak PDFdarshanmadeAinda não há avaliações

- Swot AnalysisDocumento40 páginasSwot AnalysisMohmmedKhayyumAinda não há avaliações