Você também pode gostar

- Daniel Deli, Paul Hanouna, Christof W. Stahel, Yue Tang and William YostDocumento97 páginasDaniel Deli, Paul Hanouna, Christof W. Stahel, Yue Tang and William YostMarketsWikiAinda não há avaliações

- The Complete Guide to Portfolio Construction and ManagementNo EverandThe Complete Guide to Portfolio Construction and ManagementAinda não há avaliações

- Investing in Hedge Funds: A Guide to Measuring Risk and Return CharacteristicsNo EverandInvesting in Hedge Funds: A Guide to Measuring Risk and Return CharacteristicsAinda não há avaliações

- The Future of Hedge Fund Investing: A Regulatory and Structural Solution for a Fallen IndustryNo EverandThe Future of Hedge Fund Investing: A Regulatory and Structural Solution for a Fallen IndustryAinda não há avaliações

- Alternatives in Todays Capital MarketsDocumento16 páginasAlternatives in Todays Capital MarketsjoanAinda não há avaliações

- Global Equity MarketsDocumento20 páginasGlobal Equity MarketsMohsin JavedAinda não há avaliações

- Long Term Capital Management The Dangers of LeverageDocumento25 páginasLong Term Capital Management The Dangers of LeveragepidieAinda não há avaliações

- Consultative Document (2nd) : Assessment Methodologies For Identifying Non-Bank Non-Insurer Global Systemically Important Financial InstitutionsDocumento16 páginasConsultative Document (2nd) : Assessment Methodologies For Identifying Non-Bank Non-Insurer Global Systemically Important Financial Institutionsapi-249785899Ainda não há avaliações

- Triton Presentation 1Documento28 páginasTriton Presentation 1yfatihAinda não há avaliações

- The Alpha Masters: Unlocking the Genius of the World's Top Hedge FundsNo EverandThe Alpha Masters: Unlocking the Genius of the World's Top Hedge FundsNota: 4 de 5 estrelas4/5 (15)

- Hedge Funds and Financial StabilityDocumento5 páginasHedge Funds and Financial StabilityAshish Live To WinAinda não há avaliações

- Wealth Global Navigating the International Financial MarketsNo EverandWealth Global Navigating the International Financial MarketsAinda não há avaliações

- Portfolio Optimization With International DiversificationDocumento23 páginasPortfolio Optimization With International DiversificationGulboddin MuradiAinda não há avaliações

- EN EN: and Participants Are Regulated or Subject To Oversight, As Appropriate To Their Circumstance'Documento8 páginasEN EN: and Participants Are Regulated or Subject To Oversight, As Appropriate To Their Circumstance'Manikanta ChintalaAinda não há avaliações

- A Project Report On Technical Analysis at Share KhanDocumento105 páginasA Project Report On Technical Analysis at Share KhanBabasab Patil (Karrisatte)100% (3)

- A Project Report On Technical Analysis at Cement Sector in Share KhanDocumento105 páginasA Project Report On Technical Analysis at Cement Sector in Share KhanBabasab Patil (Karrisatte)100% (1)

- A ProjectreportontechnicalanalysisDocumento102 páginasA ProjectreportontechnicalanalysisAnkita DoddamaniAinda não há avaliações

- Mastering the Market: A Comprehensive Guide to Successful Stock InvestingNo EverandMastering the Market: A Comprehensive Guide to Successful Stock InvestingAinda não há avaliações

- Overview of The Mutual Fund IndustryDocumento5 páginasOverview of The Mutual Fund Industry29_ramesh170Ainda não há avaliações

- Risky Business An Empirical Analysis of Foreign Exchange Risk Exposure in MicrofinanceDocumento36 páginasRisky Business An Empirical Analysis of Foreign Exchange Risk Exposure in MicrofinanceKafigi Nicholaus JejeAinda não há avaliações

- Title:: Duarte, Jefferson Longstaff, Francis A. Yu, FanDocumento53 páginasTitle:: Duarte, Jefferson Longstaff, Francis A. Yu, FanawylegalskiAinda não há avaliações

- Hedge FundsDocumento9 páginasHedge FundsSagar TanejaAinda não há avaliações

- Internet Stock Trading and Market Research for the Small InvestorNo EverandInternet Stock Trading and Market Research for the Small InvestorAinda não há avaliações

- Overview of Hedge Funds PERACDocumento21 páginasOverview of Hedge Funds PERACNirmal PatidarAinda não há avaliações

- An Introduction To Hedge Funds: Pictet Alternative InvestmentsDocumento16 páginasAn Introduction To Hedge Funds: Pictet Alternative InvestmentsGauravMunjalAinda não há avaliações

- Misclassification of Bond Mutual Funds 2021 ABDCDocumento32 páginasMisclassification of Bond Mutual Funds 2021 ABDCAnushi AroraAinda não há avaliações

- Wealth: How the World's High-Net-Worth Grow, Sustain, and Manage Their FortunesNo EverandWealth: How the World's High-Net-Worth Grow, Sustain, and Manage Their FortunesNota: 1 de 5 estrelas1/5 (1)

- Finance Questions Generally Asked in Interview On Equity MarketDocumento26 páginasFinance Questions Generally Asked in Interview On Equity MarketshubhamAinda não há avaliações

- Stock Market Income Genesis: Internet Business Genesis Series, #8No EverandStock Market Income Genesis: Internet Business Genesis Series, #8Ainda não há avaliações

- An easy approach to common investment funds: The introductory guide to mutual funds and the most effective investment strategies in the field of asset managementNo EverandAn easy approach to common investment funds: The introductory guide to mutual funds and the most effective investment strategies in the field of asset managementAinda não há avaliações

- Working Paper 1011Documento28 páginasWorking Paper 1011Thibaut AokiAinda não há avaliações

- A Guide To Hedge Funds PDFDocumento39 páginasA Guide To Hedge Funds PDFman downAinda não há avaliações

- Accounting for Derivatives: Advanced Hedging under IFRSNo EverandAccounting for Derivatives: Advanced Hedging under IFRSAinda não há avaliações

- INVESTING IN STOCKS: Building Wealth and Financial Freedom through Stock Market Investments (2023 Guide for Beginners)No EverandINVESTING IN STOCKS: Building Wealth and Financial Freedom through Stock Market Investments (2023 Guide for Beginners)Ainda não há avaliações

- Danger of Hedge Funds: Economic and Political Weekly August 20, 2005Documento6 páginasDanger of Hedge Funds: Economic and Political Weekly August 20, 2005Anand BansalAinda não há avaliações

- The Index Revolution: Why Investors Should Join It NowNo EverandThe Index Revolution: Why Investors Should Join It NowAinda não há avaliações

- MFX Risky-Business 2011Documento36 páginasMFX Risky-Business 2011Mario CruzAinda não há avaliações

- The Development of Mutual Funds Around The World: Leora Klapper, Víctor Sulla and Dimitri VittasDocumento43 páginasThe Development of Mutual Funds Around The World: Leora Klapper, Víctor Sulla and Dimitri VittasKamalakar ReddyAinda não há avaliações

- Teaching Notes FMI 342Documento162 páginasTeaching Notes FMI 342Hemanth KumarAinda não há avaliações

- Investments Complete Part 1 1Documento65 páginasInvestments Complete Part 1 1THOTslayer 420Ainda não há avaliações

- Teaching Notes-FMI-342 PDFDocumento162 páginasTeaching Notes-FMI-342 PDFArun PatelAinda não há avaliações

- In Search of Returns 2e: Making Sense of Financial MarketsNo EverandIn Search of Returns 2e: Making Sense of Financial MarketsAinda não há avaliações

- Mutual Funds: Portfolio Structures, Analysis, Management, and StewardshipNo EverandMutual Funds: Portfolio Structures, Analysis, Management, and StewardshipJohn A. HaslemAinda não há avaliações

- An Overview of Hedge Funds and Structured Products: Issues in Leverage and RiskDocumento20 páginasAn Overview of Hedge Funds and Structured Products: Issues in Leverage and RiskxuhaibimAinda não há avaliações

- Portfolio Mastery: Navigating the Financial Art and ScienceNo EverandPortfolio Mastery: Navigating the Financial Art and ScienceAinda não há avaliações

- Hedge FundsDocumento59 páginasHedge FundsjinalvikamseyAinda não há avaliações

- Structure : Securities and Exchange Commission Board of Directors Board of TrusteesDocumento8 páginasStructure : Securities and Exchange Commission Board of Directors Board of Trusteestanya tanwarAinda não há avaliações

- Structure : Securities and Exchange Commission Board of Directors Board of TrusteesDocumento17 páginasStructure : Securities and Exchange Commission Board of Directors Board of Trusteestanya tanwarAinda não há avaliações

- A Study On Technical Analysis At: Industry Overview Company ProfileDocumento109 páginasA Study On Technical Analysis At: Industry Overview Company ProfilePrathamesh TaywadeAinda não há avaliações

- Strategic Risk Management: A Practical Guide to Portfolio Risk ManagementNo EverandStrategic Risk Management: A Practical Guide to Portfolio Risk ManagementNota: 5 de 5 estrelas5/5 (1)

- HFF Hedge FundsDocumento34 páginasHFF Hedge Fundsaba3abaAinda não há avaliações

- Aprojectreportontechnicalanalysisatsharekhan 120809060800 Phpapp02Documento109 páginasAprojectreportontechnicalanalysisatsharekhan 120809060800 Phpapp02touffiqAinda não há avaliações

- The Complete Guide to Hedge Funds and Hedge Fund StrategiesNo EverandThe Complete Guide to Hedge Funds and Hedge Fund StrategiesNota: 3 de 5 estrelas3/5 (1)

- Turkey - Gross Domestic Product, Outlook 2016-2017Documento1 páginaTurkey - Gross Domestic Product, Outlook 2016-2017Eduardo PetazzeAinda não há avaliações

- Germany - Renewable Energies ActDocumento1 páginaGermany - Renewable Energies ActEduardo PetazzeAinda não há avaliações

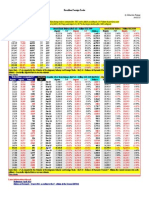

- WTI Spot PriceDocumento4 páginasWTI Spot PriceEduardo Petazze100% (1)

- Highlights, Wednesday June 8, 2016Documento1 páginaHighlights, Wednesday June 8, 2016Eduardo PetazzeAinda não há avaliações

- Analysis and Estimation of The US Oil ProductionDocumento1 páginaAnalysis and Estimation of The US Oil ProductionEduardo PetazzeAinda não há avaliações

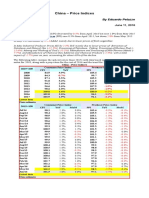

- China - Price IndicesDocumento1 páginaChina - Price IndicesEduardo PetazzeAinda não há avaliações

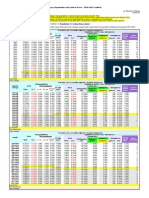

- India - Index of Industrial ProductionDocumento1 páginaIndia - Index of Industrial ProductionEduardo PetazzeAinda não há avaliações

- China - Demand For Petroleum, Energy Efficiency and Consumption Per CapitaDocumento1 páginaChina - Demand For Petroleum, Energy Efficiency and Consumption Per CapitaEduardo PetazzeAinda não há avaliações

- U.S. Employment Situation - 2015 / 2017 OutlookDocumento1 páginaU.S. Employment Situation - 2015 / 2017 OutlookEduardo PetazzeAinda não há avaliações

- U.S. New Home Sales and House Price IndexDocumento1 páginaU.S. New Home Sales and House Price IndexEduardo PetazzeAinda não há avaliações

- Reflections On The Greek Crisis and The Level of EmploymentDocumento1 páginaReflections On The Greek Crisis and The Level of EmploymentEduardo PetazzeAinda não há avaliações

- India 2015 GDPDocumento1 páginaIndia 2015 GDPEduardo PetazzeAinda não há avaliações

- Commitment of Traders - Futures Only Contracts - NYMEX (American)Documento1 páginaCommitment of Traders - Futures Only Contracts - NYMEX (American)Eduardo PetazzeAinda não há avaliações

- Singapore - 2015 GDP OutlookDocumento1 páginaSingapore - 2015 GDP OutlookEduardo PetazzeAinda não há avaliações

- USA - Oil and Gas Extraction - Estimated Impact by Low Prices On Economic AggregatesDocumento1 páginaUSA - Oil and Gas Extraction - Estimated Impact by Low Prices On Economic AggregatesEduardo PetazzeAinda não há avaliações

- South Africa - 2015 GDP OutlookDocumento1 páginaSouth Africa - 2015 GDP OutlookEduardo PetazzeAinda não há avaliações

- México, PBI 2015Documento1 páginaMéxico, PBI 2015Eduardo PetazzeAinda não há avaliações

- US Mining Production IndexDocumento1 páginaUS Mining Production IndexEduardo PetazzeAinda não há avaliações

- Highlights in Scribd, Updated in April 2015Documento1 páginaHighlights in Scribd, Updated in April 2015Eduardo PetazzeAinda não há avaliações

- U.S. Federal Open Market Committee: Federal Funds RateDocumento1 páginaU.S. Federal Open Market Committee: Federal Funds RateEduardo PetazzeAinda não há avaliações

- China - Power GenerationDocumento1 páginaChina - Power GenerationEduardo PetazzeAinda não há avaliações

- European Commission, Spring 2015 Economic Forecast, Employment SituationDocumento1 páginaEuropean Commission, Spring 2015 Economic Forecast, Employment SituationEduardo PetazzeAinda não há avaliações

- Mainland China - Interest Rates and InflationDocumento1 páginaMainland China - Interest Rates and InflationEduardo PetazzeAinda não há avaliações

- Chile, Monthly Index of Economic Activity, IMACECDocumento2 páginasChile, Monthly Index of Economic Activity, IMACECEduardo PetazzeAinda não há avaliações

- US - Personal Income and Outlays - 2015-2016 OutlookDocumento1 páginaUS - Personal Income and Outlays - 2015-2016 OutlookEduardo PetazzeAinda não há avaliações

- Japan, Indices of Industrial ProductionDocumento1 páginaJapan, Indices of Industrial ProductionEduardo PetazzeAinda não há avaliações

- Japan, Population and Labour Force - 2015-2017 OutlookDocumento1 páginaJapan, Population and Labour Force - 2015-2017 OutlookEduardo PetazzeAinda não há avaliações

- Brazilian Foreign TradeDocumento1 páginaBrazilian Foreign TradeEduardo PetazzeAinda não há avaliações

- South Korea, Monthly Industrial StatisticsDocumento1 páginaSouth Korea, Monthly Industrial StatisticsEduardo PetazzeAinda não há avaliações

- United States - Gross Domestic Product by IndustryDocumento1 páginaUnited States - Gross Domestic Product by IndustryEduardo PetazzeAinda não há avaliações

- GBC Jot Case Study FINALDocumento29 páginasGBC Jot Case Study FINALSharmin Lisa100% (1)

- Group 2 Case 1 Assignment Bubble Bee Organic The Need For Pro Forma Financial Modeling SupplDocumento13 páginasGroup 2 Case 1 Assignment Bubble Bee Organic The Need For Pro Forma Financial Modeling SupplSarah WuAinda não há avaliações

- Learning From Dr. Michael J. Burrys Investment Philosophy 2Documento25 páginasLearning From Dr. Michael J. Burrys Investment Philosophy 2Leonard WijayaAinda não há avaliações

- Abacus Securities Corp. VS. AmpilDocumento21 páginasAbacus Securities Corp. VS. AmpilYour Public ProfileAinda não há avaliações

- Fortress FundDocumento5 páginasFortress FundTuriyaAinda não há avaliações

- AxasxDocumento26 páginasAxasxГал БадрахAinda não há avaliações

- Acct 260 CHAPTER 8Documento25 páginasAcct 260 CHAPTER 8John Guy0% (1)

- Banking Survey 2014Documento52 páginasBanking Survey 2014Hassan TariqAinda não há avaliações

- 07 X07 A Responsibility Accounting and TP Decentralization and Performance EvaluationDocumento11 páginas07 X07 A Responsibility Accounting and TP Decentralization and Performance EvaluationNora Pasa100% (1)

- Excel Margin Call CalculationsDocumento1 páginaExcel Margin Call Calculationsapi-27174321100% (1)

- Financial Management - Compilation of Financial RatiosDocumento6 páginasFinancial Management - Compilation of Financial RatiosIce AlojaAinda não há avaliações

- Financial Analysis On Investment Banks of BDDocumento76 páginasFinancial Analysis On Investment Banks of BDAnika TabassumAinda não há avaliações

- BVADocumento15 páginasBVAJasonAinda não há avaliações

- (1936) New Stock Trend DetectorDocumento52 páginas(1936) New Stock Trend DetectorBellwetherSataraAinda não há avaliações

- Licence To TradeDocumento92 páginasLicence To TradeImrana Saleh67% (3)

- Answer To The Case StudyDocumento11 páginasAnswer To The Case StudyNahidul Islam IU100% (3)

- A Project ReportDocumento30 páginasA Project ReportPRANAT GUPTAAinda não há avaliações

- Objectives and Functions of Alco: Bank Assets and LiabilitiesDocumento8 páginasObjectives and Functions of Alco: Bank Assets and LiabilitiesAlee OvaysAinda não há avaliações

- A Revolutionary Way To Achieve Wealth in UgandaDocumento118 páginasA Revolutionary Way To Achieve Wealth in UgandatwhyAinda não há avaliações

- Assignment On Financial Institution: Dhanlaxmi BankDocumento12 páginasAssignment On Financial Institution: Dhanlaxmi BankAkshay Thampi RCBSAinda não há avaliações

- Fin Exam 1Documento14 páginasFin Exam 1tahaalkibsiAinda não há avaliações

- FinancialPlan - 2013 Version - Prof DR IsmailDocumento129 páginasFinancialPlan - 2013 Version - Prof DR IsmailSyukur Byte0% (1)

- Margin of SafetyDocumento5 páginasMargin of SafetyGerald Handerson100% (1)

- Financial Analysis ProtonDocumento9 páginasFinancial Analysis Protonmoonernest100% (2)

- Accounting AnswersDocumento6 páginasAccounting AnswersSalman KhalidAinda não há avaliações

- Estimating Working CapitalDocumento36 páginasEstimating Working CapitalKylaa Angelica de LeonAinda não há avaliações

- Risk Hedging Instruments and MechanismDocumento11 páginasRisk Hedging Instruments and Mechanism03 TYBMS Prajakta ChoratAinda não há avaliações

- Canara Bank ChargesDocumento8 páginasCanara Bank Chargesaca_trader100% (1)

- Angel One LTD.: Applica On Number: Applica On Type : o New KYC o Modifica On KYCDocumento29 páginasAngel One LTD.: Applica On Number: Applica On Type : o New KYC o Modifica On KYCnm3456008Ainda não há avaliações

- Tata Steel Key Financial Ratios, Tata Steel Financial Statement & AccountsDocumento3 páginasTata Steel Key Financial Ratios, Tata Steel Financial Statement & Accountsmohan chouriwarAinda não há avaliações