Você também pode gostar

- Advertisement Notice 1 2014Documento4 páginasAdvertisement Notice 1 2014ihateu1Ainda não há avaliações

- Chapte R No. Title NODocumento3 páginasChapte R No. Title NOManish MahajanAinda não há avaliações

- 2010-Human Resource ManagementDocumento2 páginas2010-Human Resource ManagementManish MahajanAinda não há avaliações

- WWW - Jammuuniversity.in PDF Job-06!06!2014Documento4 páginasWWW - Jammuuniversity.in PDF Job-06!06!2014Manish MahajanAinda não há avaliações

- Ur!.lviiil@: & If & & Lor andDocumento4 páginasUr!.lviiil@: & If & & Lor andManish MahajanAinda não há avaliações

- The Land of RockDocumento5 páginasThe Land of RockManish MahajanAinda não há avaliações

- Form B Certificate of RegistrationDocumento1 páginaForm B Certificate of RegistrationManish MahajanAinda não há avaliações

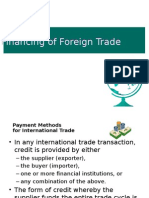

- Financing of Foreign TradeDocumento29 páginasFinancing of Foreign TradeManish MahajanAinda não há avaliações

- 2012-Distribution and Sales MNGTDocumento3 páginas2012-Distribution and Sales MNGTManish MahajanAinda não há avaliações

- CST Regitration FormDocumento3 páginasCST Regitration FormAvanindra BhushanAinda não há avaliações

- Form Vat-01Documento6 páginasForm Vat-01Manish MahajanAinda não há avaliações

- Name:-Divya Gupta ROLL NO. 13-MBA-2013 Subject-Management of Financial ServicesDocumento2 páginasName:-Divya Gupta ROLL NO. 13-MBA-2013 Subject-Management of Financial ServicesManish MahajanAinda não há avaliações

- Fiscal DeficitDocumento32 páginasFiscal DeficitManish MahajanAinda não há avaliações

- CST Regitration FormDocumento3 páginasCST Regitration FormAvanindra BhushanAinda não há avaliações

- ImplementationDocumento32 páginasImplementationManish MahajanAinda não há avaliações

- Fiscal Policy: by Kumar Devrat Rohita Mohit Shukla Nasreen Prashant SharmaDocumento19 páginasFiscal Policy: by Kumar Devrat Rohita Mohit Shukla Nasreen Prashant SharmaMohit ShuklaAinda não há avaliações

- JKPDD: Government of Jammu & KashmirDocumento3 páginasJKPDD: Government of Jammu & KashmirManish MahajanAinda não há avaliações

- Questionnaire A ADocumento3 páginasQuestionnaire A AManish MahajanAinda não há avaliações

- Questionnaire: Demographic InformationDocumento3 páginasQuestionnaire: Demographic InformationManish MahajanAinda não há avaliações

- Capital Budgeting For The Multinational CorporationDocumento18 páginasCapital Budgeting For The Multinational CorporationManish MahajanAinda não há avaliações

- Notification UIIC Assistant PostsDocumento17 páginasNotification UIIC Assistant Postsprabhakar_elexAinda não há avaliações

- Case StudyDocumento3 páginasCase StudyManish MahajanAinda não há avaliações

- The Secrets To Successful Strategy ExecutionDocumento1 páginaThe Secrets To Successful Strategy ExecutionManish MahajanAinda não há avaliações

- 11032015Documento3 páginas11032015Manish MahajanAinda não há avaliações

- 28112014Documento2 páginas28112014Manish MahajanAinda não há avaliações

- 18102014Documento24 páginas18102014Wasim ParrayAinda não há avaliações

- Topic S DescriptionDocumento66 páginasTopic S DescriptionManish MahajanAinda não há avaliações

- Venture CapitalDocumento6 páginasVenture CapitalManish MahajanAinda não há avaliações

- NoticeDocumento1 páginaNoticeManish MahajanAinda não há avaliações

- Bimal Jalan CommitteeDocumento17 páginasBimal Jalan CommitteeManish MahajanAinda não há avaliações

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (120)

- Linear ProgrammingDocumento3 páginasLinear Programmingইমরান এইচ শিশিরAinda não há avaliações

- Fico Fico Xpress Optimization Xpress Optimization: Quick ReferenceDocumento18 páginasFico Fico Xpress Optimization Xpress Optimization: Quick ReferenceYeimmy Julieth Cardenas MillanAinda não há avaliações

- Reflection 2019Documento1 páginaReflection 2019Elizabeth RubioAinda não há avaliações

- 2nd Term Quatitative TechniquesDocumento112 páginas2nd Term Quatitative TechniquesShreedhar100% (1)

- Plant Design PDFDocumento97 páginasPlant Design PDFermias abayAinda não há avaliações

- New Cima p1 2019 NotesDocumento112 páginasNew Cima p1 2019 NotesNassib SongoroAinda não há avaliações

- Operations Research Linear Programming CHeggDocumento19 páginasOperations Research Linear Programming CHeggAkaki TkeshelashviliAinda não há avaliações

- OR Module 2 SESSION 2Documento52 páginasOR Module 2 SESSION 2Vicky VijayAinda não há avaliações

- Introduction To Linear ProgrammingDocumento19 páginasIntroduction To Linear ProgrammingzawadzahinAinda não há avaliações

- Operations Research Assignment - Shivani Khare - SecB - 21020037Documento9 páginasOperations Research Assignment - Shivani Khare - SecB - 21020037shivani khareAinda não há avaliações

- Linear Programming Applied To Water Quality ManagementDocumento9 páginasLinear Programming Applied To Water Quality ManagementfddfadsfadsfAinda não há avaliações

- MILP Unit Commitment FormulationDocumento8 páginasMILP Unit Commitment FormulationAhmed AsimAinda não há avaliações

- Mock Test - Attempt ReviewDocumento16 páginasMock Test - Attempt Reviewkiralight511Ainda não há avaliações

- Sequential Quadratic ProgrammingDocumento52 páginasSequential Quadratic ProgrammingTaylorAinda não há avaliações

- Introduction To LPPDocumento10 páginasIntroduction To LPPAmiya ArnavAinda não há avaliações

- Decision Science - MCQDocumento36 páginasDecision Science - MCQpritesh0% (1)

- Proforma Mte 3104 - Decision MathematicsDocumento3 páginasProforma Mte 3104 - Decision MathematicsMUHAMMAD RIDHUAN BIN HANAFIAinda não há avaliações

- De La Cruz John D. BSMA 1 B MGTSCI MIDTERM EXAMDocumento8 páginasDe La Cruz John D. BSMA 1 B MGTSCI MIDTERM EXAMJohn DelacruzAinda não há avaliações

- EContent 1 2023 06 24 10 20 29 QTDM Studymaterialfeb23pdf 2023 03 15 11 44 02Documento23 páginasEContent 1 2023 06 24 10 20 29 QTDM Studymaterialfeb23pdf 2023 03 15 11 44 02Tom CruiseAinda não há avaliações

- Paper Exposed Ore ReserveDocumento9 páginasPaper Exposed Ore ReserveMatías Ignacio Loyola GaldamesAinda não há avaliações

- Lagrangian Relaxation: An Overview: General IdeaDocumento4 páginasLagrangian Relaxation: An Overview: General Ideaami554Ainda não há avaliações

- EFIM20005: Management Science: Video Lecture Part A: Formulating A LP ModelDocumento61 páginasEFIM20005: Management Science: Video Lecture Part A: Formulating A LP ModeljkleAinda não há avaliações

- Lecture 01 SimplexDocumento37 páginasLecture 01 Simplexbekmurod.dsAinda não há avaliações

- Zambian Open University: Bba 313 - Operations ResearchDocumento6 páginasZambian Open University: Bba 313 - Operations ResearchMASMO SHIYALAAinda não há avaliações

- 3 Linear Programming ProblemsDocumento17 páginas3 Linear Programming ProblemsnknknknAinda não há avaliações

- Lab Sessions 1 To 5 OTDocumento95 páginasLab Sessions 1 To 5 OTShahbaz ahmadAinda não há avaliações

- Linear Programming III - The Dual ProblemDocumento14 páginasLinear Programming III - The Dual ProblemAnonymous lrILoRYJWAinda não há avaliações

- Base de Datos Diseño de Plantas.Documento7 páginasBase de Datos Diseño de Plantas.Malhi León PáezAinda não há avaliações

- Linear Programming I: Patrik ForssénDocumento14 páginasLinear Programming I: Patrik ForssénmustafaAinda não há avaliações

- Operations Research ModuleDocumento203 páginasOperations Research Modulemedrek100% (1)