Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- (Solved) Lombard Company Is Contemplating The PurDocumento5 páginas(Solved) Lombard Company Is Contemplating The PurFahmi Ilham Akbar0% (1)

- Preqin - Corp Investor - IndiaDocumento21 páginasPreqin - Corp Investor - Indiasavan anvekarAinda não há avaliações

- Hotel NewsDocumento88 páginasHotel NewsnickiminajAinda não há avaliações

- Mateo Manuscript Om Buma 20093Documento13 páginasMateo Manuscript Om Buma 20093Mhico MateoAinda não há avaliações

- COVID-19 Supply Chain DisruptionDocumento1 páginaCOVID-19 Supply Chain DisruptionvikramAinda não há avaliações

- Intro Mining First AssignmnetDocumento10 páginasIntro Mining First AssignmnetTemesgen SilabatAinda não há avaliações

- Self Test 4. Financial Planning Time: 1 Hour) (Marks: 20 Q. 1. (A) Choose The Correct Alternative From Those Given Below Each Question: 4Documento3 páginasSelf Test 4. Financial Planning Time: 1 Hour) (Marks: 20 Q. 1. (A) Choose The Correct Alternative From Those Given Below Each Question: 4UmarAinda não há avaliações

- Instrumen Self Assessment Risiko Covid-19 (Employee) (1-81)Documento5 páginasInstrumen Self Assessment Risiko Covid-19 (Employee) (1-81)Dicky ChandraAinda não há avaliações

- RR 07-03Documento3 páginasRR 07-03saintkarriAinda não há avaliações

- Fixed Asset Register SampleDocumento51 páginasFixed Asset Register SampleRifalino Al-habibieAinda não há avaliações

- NMIMS Global Access Course: Factors Impacting Demand and SupplyDocumento8 páginasNMIMS Global Access Course: Factors Impacting Demand and Supplyrahul upadhyeAinda não há avaliações

- Articles of Incorporation 2Documento5 páginasArticles of Incorporation 2Marcos DmitriAinda não há avaliações

- MG321 Mid Semester Test, Semester 2, 2021 InstructionsDocumento5 páginasMG321 Mid Semester Test, Semester 2, 2021 InstructionsSanket PatelAinda não há avaliações

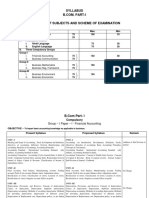

- Syllabus Grouping of Subjects and Scheme of ExaminationDocumento29 páginasSyllabus Grouping of Subjects and Scheme of ExaminationAbhisek AgrawalAinda não há avaliações

- JAIME Company budgeting questionsDocumento2 páginasJAIME Company budgeting questionsLopez, Azzia M.Ainda não há avaliações

- A Case Study by Umang Jain Find Me HereDocumento16 páginasA Case Study by Umang Jain Find Me HereGaurav ManiyarAinda não há avaliações

- Cost Accounting Assignment SolutionsDocumento10 páginasCost Accounting Assignment SolutionsSara PervezAinda não há avaliações

- Public Sector Accounting: Mr. Evans AgalegaDocumento35 páginasPublic Sector Accounting: Mr. Evans AgalegaElvis Yarig100% (1)

- HEL Case Study on Supply Chain ManagementDocumento27 páginasHEL Case Study on Supply Chain ManagementMayank KothariAinda não há avaliações

- Financial Times UK 08jan2020 PDFDocumento26 páginasFinancial Times UK 08jan2020 PDFTaimur AbdullahAinda não há avaliações

- 6409-Article Text-22422-1-10-20120709 PDFDocumento10 páginas6409-Article Text-22422-1-10-20120709 PDFAmosh ShresthaAinda não há avaliações

- HEALTHCARE SERVICESDocumento2 páginasHEALTHCARE SERVICESraviAinda não há avaliações

- Metalem Ademe, Thesis Draft On Price Escalation Done On ABWC Improv 1Documento69 páginasMetalem Ademe, Thesis Draft On Price Escalation Done On ABWC Improv 1Hope GoAinda não há avaliações

- Operations Management 11th Edition Stevenson Solutions ManualDocumento32 páginasOperations Management 11th Edition Stevenson Solutions Manualeiranguyenrd8t100% (24)

- Mylan Write-Up Historicals and Sell RecommendationDocumento1 páginaMylan Write-Up Historicals and Sell RecommendationAdam SchlossAinda não há avaliações

- Rajat Gupta and Insider Trading: by Todd ShimamotoDocumento11 páginasRajat Gupta and Insider Trading: by Todd ShimamotoBharani BharaniAinda não há avaliações

- Cambridge IGCSE™: Accounting 0452/22 March 2021Documento19 páginasCambridge IGCSE™: Accounting 0452/22 March 2021Farrukhsg50% (2)

- Assignment GE MckinseyDocumento2 páginasAssignment GE MckinseyBhavana Watwani100% (1)

- Akuntansi p5Documento7 páginasAkuntansi p5Alche MistAinda não há avaliações

- Taylor Scientific ManagementDocumento6 páginasTaylor Scientific ManagementMondayAinda não há avaliações