Você também pode gostar

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Universal Remote SUPERIOR AIRCO 1000 in 1 For AirCoDocumento2 páginasUniversal Remote SUPERIOR AIRCO 1000 in 1 For AirCoceteganAinda não há avaliações

- First Draft of The 2012 City of Brantford Budget DocumentsDocumento1.181 páginasFirst Draft of The 2012 City of Brantford Budget DocumentsHugo Rodrigues100% (1)

- CIBP Projects and Working Groups PDFDocumento37 páginasCIBP Projects and Working Groups PDFCIBPAinda não há avaliações

- Indian Association of Soil and Water ConservationistsDocumento521 páginasIndian Association of Soil and Water Conservationistsshyam143225Ainda não há avaliações

- FPEF ED 2017 Lo Res Pagination 002Documento136 páginasFPEF ED 2017 Lo Res Pagination 002klapperdopAinda não há avaliações

- Tick DataDocumento38 páginasTick DataIstvan GergelyAinda não há avaliações

- Spy Gap StudyDocumento30 páginasSpy Gap StudyMathias Dharmawirya100% (1)

- Wec11 01 Rms 20230112Documento27 páginasWec11 01 Rms 20230112Shafay SheikhAinda não há avaliações

- Consumption FunctionDocumento31 páginasConsumption Functionscottsummers39Ainda não há avaliações

- Business PlanDocumento20 páginasBusiness Planlucian89% (18)

- Free Market CapitalismDocumento18 páginasFree Market CapitalismbalathekickboxerAinda não há avaliações

- Investment Notes PDFDocumento30 páginasInvestment Notes PDFMuhammad NaeemAinda não há avaliações

- 1009-Article Text-1731-1-10-20171225 PDFDocumento6 páginas1009-Article Text-1731-1-10-20171225 PDFPursottam SarafAinda não há avaliações

- Fibonacci Trading (PDFDrive)Documento148 páginasFibonacci Trading (PDFDrive)ARK WOODYAinda não há avaliações

- Faisal, Napitupulu and Chariri (2019) Corporate Social and Environmental Responsibility Disclosure in Indonesian Companies Symbolic or SubstantiveDocumento20 páginasFaisal, Napitupulu and Chariri (2019) Corporate Social and Environmental Responsibility Disclosure in Indonesian Companies Symbolic or SubstantiveMuhamad Arif RohmanAinda não há avaliações

- Material 2. Writing A Synthesis Essay. Behrens, Rosen - pp.120-134Documento15 páginasMaterial 2. Writing A Synthesis Essay. Behrens, Rosen - pp.120-134George MujiriAinda não há avaliações

- ZZZZDocumento14 páginasZZZZMustofa Nur HayatAinda não há avaliações

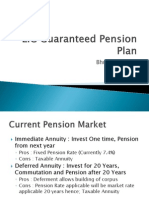

- LIC Guaranteed HNI Pension PlanDocumento9 páginasLIC Guaranteed HNI Pension PlanBhushan ShethAinda não há avaliações

- Free Talk SeniorDocumento102 páginasFree Talk SeniorCharmen Joy PonsicaAinda não há avaliações

- Bhavnath TempleDocumento7 páginasBhavnath TempleManpreet Singh'100% (1)

- Afiq Razlan Bin Abdul Razad: Trucking/Operation JR - ExecutiveDocumento2 páginasAfiq Razlan Bin Abdul Razad: Trucking/Operation JR - ExecutiveDaniel Fauzi AhmadAinda não há avaliações

- Asg1 - Nagakin Capsule TowerDocumento14 páginasAsg1 - Nagakin Capsule TowerSatyam GuptaAinda não há avaliações

- Account StatementDocumento4 páginasAccount StatementDure ShehwarAinda não há avaliações

- Southeast Asia Thriving in The Shadow of GiantsDocumento38 páginasSoutheast Asia Thriving in The Shadow of GiantsDDAinda não há avaliações

- RP 1Documento42 páginasRP 1Pahe LambAinda não há avaliações

- Case Study 4Documento8 páginasCase Study 4Lyka NaboaAinda não há avaliações

- Zapa ChemicalDocumento6 páginasZapa ChemicalZordanAinda não há avaliações

- Controlling The Global EconomyDocumento22 páginasControlling The Global EconomyCetkinAinda não há avaliações

- I. Annexure A. Questionnaire: Idbi BankDocumento4 páginasI. Annexure A. Questionnaire: Idbi BankRiSHI KeSH GawaIAinda não há avaliações

- The Philippine Administrative SystemDocumento10 páginasThe Philippine Administrative SystemDan YuAinda não há avaliações