Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Davis Dynasty: Focus Take-AwaysDocumento5 páginasThe Davis Dynasty: Focus Take-Awaysgreyistari100% (1)

- FGate Vinamilk VNM ModelDocumento94 páginasFGate Vinamilk VNM Modelnvanhuu98Ainda não há avaliações

- GRC PWC IntegritydrivenperformanceDocumento52 páginasGRC PWC IntegritydrivenperformanceDeepak YakkundiAinda não há avaliações

- Final DocumentationDocumento39 páginasFinal DocumentationSelva KumarAinda não há avaliações

- Project Profile For Establishment of 48 Automatic Loom: 1.0 Scope of The Project in The Area of OperationDocumento2 páginasProject Profile For Establishment of 48 Automatic Loom: 1.0 Scope of The Project in The Area of OperationSelva KumarAinda não há avaliações

- A Study On Cunsumers Preference and Attitude Towards Purchase of Gold (With Special Reference To Pollachi Talluk)Documento5 páginasA Study On Cunsumers Preference and Attitude Towards Purchase of Gold (With Special Reference To Pollachi Talluk)Selva KumarAinda não há avaliações

- Chapter 2Documento36 páginasChapter 2Selva KumarAinda não há avaliações

- Create and Display The List of Ledger Accounts in The Books of Star LTD On 31 MarchDocumento1 páginaCreate and Display The List of Ledger Accounts in The Books of Star LTD On 31 MarchSelva KumarAinda não há avaliações

- UTR: P17010306821520: Beneficiary DetailsDocumento1 páginaUTR: P17010306821520: Beneficiary DetailsSelva KumarAinda não há avaliações

- DFT Study On Dihydrogen Bond Interactions by Substitution in XH Si .NCH and NCH .HM (X H, F, CL, BR M Li, Na, Beh, MGH) ComplexesDocumento24 páginasDFT Study On Dihydrogen Bond Interactions by Substitution in XH Si .NCH and NCH .HM (X H, F, CL, BR M Li, Na, Beh, MGH) ComplexesSelva KumarAinda não há avaliações

- A Study On Customer Satisfaction Towards Tvs MotorDocumento3 páginasA Study On Customer Satisfaction Towards Tvs MotorSelva KumarAinda não há avaliações

- Program For Form ValidationDocumento8 páginasProgram For Form ValidationSelva KumarAinda não há avaliações

- Program For User Defined Exception / Exp - HTMLDocumento2 páginasProgram For User Defined Exception / Exp - HTMLSelva KumarAinda não há avaliações

- Determination of GoalsDocumento1 páginaDetermination of GoalsSelva KumarAinda não há avaliações

- Program For Illustrate The Concept of Cookies / Cookies - PHPDocumento3 páginasProgram For Illustrate The Concept of Cookies / Cookies - PHPSelva KumarAinda não há avaliações

- Jfty) Mwpa (K) Chpik RL) LJ) JPD) FPH) MDG) G (DH)Documento2 páginasJfty) Mwpa (K) Chpik RL) LJ) JPD) FPH) MDG) G (DH)Selva KumarAinda não há avaliações

- Telephone Banking: FeaturesDocumento3 páginasTelephone Banking: FeaturesSelva KumarAinda não há avaliações

- Coir ProjectDocumento18 páginasCoir ProjectSelva KumarAinda não há avaliações

- Companies Act 2017Documento30 páginasCompanies Act 2017Muhammad AzeemAinda não há avaliações

- CHAPTER - 5 - Exercise & ProblemsDocumento6 páginasCHAPTER - 5 - Exercise & ProblemsFahad Mushtaq20% (5)

- Ap 9401-1 SheDocumento4 páginasAp 9401-1 SheLuzviminda SaspaAinda não há avaliações

- Carpio, J.: Directors, and Thus in The Present Case Only To Common Shares, and Not To The TotalDocumento3 páginasCarpio, J.: Directors, and Thus in The Present Case Only To Common Shares, and Not To The Totalkimoymoy7Ainda não há avaliações

- Midterm II SampleDocumento4 páginasMidterm II SamplejamesAinda não há avaliações

- Technical Perspectives: Louise Yamada Technical Research Advisors, LLCDocumento8 páginasTechnical Perspectives: Louise Yamada Technical Research Advisors, LLCanalyst_anil14Ainda não há avaliações

- PS1Documento5 páginasPS1faiqsattarAinda não há avaliações

- Islamic Perspective of Maximizaing Shareholders' WealthDocumento56 páginasIslamic Perspective of Maximizaing Shareholders' WealthI'ffah NasirAinda não há avaliações

- Nestle: Final Task in Fundamentals of Accountancy, Business and ManagementDocumento43 páginasNestle: Final Task in Fundamentals of Accountancy, Business and ManagementApply Ako Work EhAinda não há avaliações

- FNDACT2 Corporations PDFDocumento11 páginasFNDACT2 Corporations PDFEl YangAinda não há avaliações

- Acct 4610Documento3 páginasAcct 4610Juliette YasuhiroAinda não há avaliações

- World Largest Gold and Copper Mine Reko Diq BalochistanDocumento6 páginasWorld Largest Gold and Copper Mine Reko Diq BalochistanJavaid Ali ShahAinda não há avaliações

- Strategic Management Full NotesDocumento133 páginasStrategic Management Full Notessahir_sameer1984100% (1)

- ALR 20180427172542 2017-Annual-Report PDFDocumento130 páginasALR 20180427172542 2017-Annual-Report PDFAnonimu256Ainda não há avaliações

- Mahusay Bsa 315 Module 3 Major OutputDocumento7 páginasMahusay Bsa 315 Module 3 Major OutputJeth MahusayAinda não há avaliações

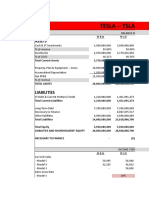

- Tesla ForecastDocumento6 páginasTesla ForecastDanikaLiAinda não há avaliações

- Chart of Entity ComparisonDocumento4 páginasChart of Entity ComparisonDee BeldAinda não há avaliações

- BA Boeing Stock SummaryDocumento1 páginaBA Boeing Stock SummaryOld School ValueAinda não há avaliações

- Leverage and Capital StructureDocumento8 páginasLeverage and Capital StructureC H ♥ N T ZAinda não há avaliações

- Panlilio Vs Citi BankDocumento2 páginasPanlilio Vs Citi BankRed HoodAinda não há avaliações

- Government-Owned And/Or Controlled Corporations: (GOCC)Documento30 páginasGovernment-Owned And/Or Controlled Corporations: (GOCC)Angelica HonaAinda não há avaliações

- FTSE All-World High Dividend Yield IndexDocumento16 páginasFTSE All-World High Dividend Yield IndexLeonardo ToledoAinda não há avaliações

- Canslim TradingDocumento1 páginaCanslim TradingSudeesh Kumar Pabbathi100% (1)

- Test 8 Corporate GovernanceDocumento3 páginasTest 8 Corporate GovernanceMir Fida NadeemAinda não há avaliações

- Pocket Money Course Material-MarathiDocumento81 páginasPocket Money Course Material-MarathiAbhieshek P GodhaAinda não há avaliações

- KKR Investor UpdateDocumento8 páginasKKR Investor Updatepucci23Ainda não há avaliações

- The State of Social Enterprise in Indoensia British Council Web FinalDocumento101 páginasThe State of Social Enterprise in Indoensia British Council Web FinalAlinda PermatasariAinda não há avaliações