Você também pode gostar

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- Shariah Requirements in The Contracting PartiesDocumento26 páginasShariah Requirements in The Contracting PartiesfashdeenAinda não há avaliações

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Shariah Issues in TakafulDocumento16 páginasShariah Issues in Takafulfashdeen100% (2)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Financial Due-Diligence in IslamDocumento14 páginasFinancial Due-Diligence in IslamfashdeenAinda não há avaliações

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Islamic EconomicsDocumento14 páginasIslamic EconomicsfashdeenAinda não há avaliações

- Feasibility Report On Fish Farm ProductionDocumento14 páginasFeasibility Report On Fish Farm Productionfashdeen86% (49)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- BPI Vs PosadasDocumento2 páginasBPI Vs PosadasCarlota Nicolas VillaromanAinda não há avaliações

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Checklistand Sample Forms FinalDocumento46 páginasChecklistand Sample Forms FinalDK DalusongAinda não há avaliações

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

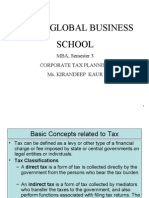

- Amity Global Business School: MBA, Semester 3 Corporate Tax Planning Ms. Kirandeep KaurDocumento14 páginasAmity Global Business School: MBA, Semester 3 Corporate Tax Planning Ms. Kirandeep KaurAditya SinghAinda não há avaliações

- Tax Deduction at Source OR: Tds/TcsDocumento29 páginasTax Deduction at Source OR: Tds/TcsArka PramanikAinda não há avaliações

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Strategic Planning For Emerging Growth CompaniesDocumento73 páginasStrategic Planning For Emerging Growth CompaniesrmdecaAinda não há avaliações

- Chapter 16: Hybrid and Derivative SecuritiesDocumento70 páginasChapter 16: Hybrid and Derivative SecuritiesJoreseAinda não há avaliações

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Future Trends in LNG Project Finance - M FilippichDocumento36 páginasFuture Trends in LNG Project Finance - M Filippichmichael_filippich2Ainda não há avaliações

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Oriental Engineering Works PVTDocumento20 páginasOriental Engineering Works PVTDarshan DhimanAinda não há avaliações

- Unit ThreeDocumento5 páginasUnit ThreeTIZITAW MASRESHA100% (1)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- State Bank of India: HdfcbankDocumento3 páginasState Bank of India: HdfcbankAmit deyAinda não há avaliações

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Tde EosDocumento9 páginasTde EosAnonymous blVjJY6Ainda não há avaliações

- Internship Project ON Fundamental and Technical Analysis On Equity DerivativesDocumento85 páginasInternship Project ON Fundamental and Technical Analysis On Equity Derivativestarun nemalipuriAinda não há avaliações

- What Is Transnational Corporation?: Royal Dutch Shell The Hague Netherlands London United KingdomDocumento2 páginasWhat Is Transnational Corporation?: Royal Dutch Shell The Hague Netherlands London United KingdomChaN.deDiosAinda não há avaliações

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- EC Bulletin Annual Incentive Plan Design SurveyDocumento6 páginasEC Bulletin Annual Incentive Plan Design SurveyVikas RamavarmaAinda não há avaliações

- Granules India On The Growth PathDocumento5 páginasGranules India On The Growth PathAravinda BoddupalliAinda não há avaliações

- Esso Ar2014 enDocumento116 páginasEsso Ar2014 endjokouwmAinda não há avaliações

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- Capital BudgetingDocumento4 páginasCapital Budgetingrachmmm0% (3)

- Putnam White Paper: The Outlook For U.S. and European BanksDocumento12 páginasPutnam White Paper: The Outlook For U.S. and European BanksPutnam InvestmentsAinda não há avaliações

- Understanding The Bad Bank - McKinsey QuarterlyDocumento11 páginasUnderstanding The Bad Bank - McKinsey QuarterlyitsalmaitiAinda não há avaliações

- Manulife ESP PDFDocumento31 páginasManulife ESP PDFTim YapAinda não há avaliações

- 10789103Documento7 páginas10789103Sachit MalikAinda não há avaliações

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Asset Liability Management QuestionnaireDocumento9 páginasAsset Liability Management QuestionnairePriya MhatreAinda não há avaliações

- Bucksbaum SuitDocumento28 páginasBucksbaum SuitChicago Tribune100% (1)

- Risk and Return Trade OffDocumento14 páginasRisk and Return Trade OffDebabrata SutarAinda não há avaliações

- Collapse of The Thai BahtDocumento5 páginasCollapse of The Thai BahtShakil AlamAinda não há avaliações

- Audit RiskDocumento5 páginasAudit RiskFermie Shell100% (1)

- #2 Flip & Gap First Position Funding, Instructions, C&P, Referral 06-03-19Documento8 páginas#2 Flip & Gap First Position Funding, Instructions, C&P, Referral 06-03-19Darnell Woodard100% (1)

- Final ProjectDocumento39 páginasFinal ProjectJerry SharmaAinda não há avaliações

- Balance SheetDocumento2 páginasBalance SheetPro ResourcesAinda não há avaliações

- J JDocumento4 páginasJ JShani KhanAinda não há avaliações