Você também pode gostar

- Afs PDFDocumento86 páginasAfs PDFms.AhmedAinda não há avaliações

- Spreadsheet Modelling For Solving Combinatorial Problems: The Vendor Selection ProblemDocumento13 páginasSpreadsheet Modelling For Solving Combinatorial Problems: The Vendor Selection ProblemNikhil GandhiAinda não há avaliações

- 01 Kros Ch01Documento28 páginas01 Kros Ch01Nikhil Gandhi0% (1)

- 437 Handout 7Documento60 páginas437 Handout 7Nikhil GandhiAinda não há avaliações

- 5 2 199-211Documento13 páginas5 2 199-211Nikhil GandhiAinda não há avaliações

- Spreadsheet Modelling For Solving Combinatorial Problems: The Vendor Selection ProblemDocumento13 páginasSpreadsheet Modelling For Solving Combinatorial Problems: The Vendor Selection ProblemNikhil GandhiAinda não há avaliações

- Other Assumptions: Each YearDocumento22 páginasOther Assumptions: Each YearNikhil GandhiAinda não há avaliações

- An Alternative Corporate Governance System: Aswath Damodaran! 47!Documento23 páginasAn Alternative Corporate Governance System: Aswath Damodaran! 47!Nikhil GandhiAinda não há avaliações

- Session 9Documento17 páginasSession 9Nikhil GandhiAinda não há avaliações

- Session 13Documento28 páginasSession 13Nikhil GandhiAinda não há avaliações

- Session 5Documento17 páginasSession 5Nikhil GandhiAinda não há avaliações

- Session 8Documento23 páginasSession 8Nikhil GandhiAinda não há avaliações

- Session 10Documento10 páginasSession 10Nikhil GandhiAinda não há avaliações

- Session 7Documento20 páginasSession 7Nikhil GandhiAinda não há avaliações

- Finance Notes From DamodharamDocumento2 páginasFinance Notes From DamodharamNikhil GandhiAinda não há avaliações

- Session 6Documento28 páginasSession 6Nikhil GandhiAinda não há avaliações

- So, What Next? When The Cat Is Idle, The Mice Will Play ...Documento28 páginasSo, What Next? When The Cat Is Idle, The Mice Will Play ...Nikhil GandhiAinda não há avaliações

- The Cost of Capital: OutlineDocumento10 páginasThe Cost of Capital: OutlineNikhil GandhiAinda não há avaliações

- Session 2Documento18 páginasSession 2Nikhil GandhiAinda não há avaliações

- Finance Notes From DamodharamDocumento2 páginasFinance Notes From DamodharamNikhil GandhiAinda não há avaliações

- Finance Solved CasesDocumento79 páginasFinance Solved Cases07413201980% (5)

- A Primer On Spreadsheet AnalyticsDocumento12 páginasA Primer On Spreadsheet Analyticsmasarriam1986Ainda não há avaliações

- Hurdlerate ChapterDocumento109 páginasHurdlerate ChapterNikhil GandhiAinda não há avaliações

- Other Assumptions: Each YearDocumento22 páginasOther Assumptions: Each YearNikhil GandhiAinda não há avaliações

- Session 14Documento39 páginasSession 14Nikhil GandhiAinda não há avaliações

- What Is Free Cash Flow and How Do I Calculate It?: A Summary Provided by Pamela Peterson Drake, James Madison UniversityDocumento8 páginasWhat Is Free Cash Flow and How Do I Calculate It?: A Summary Provided by Pamela Peterson Drake, James Madison UniversityNikhil GandhiAinda não há avaliações

- Session 17Documento17 páginasSession 17Nikhil GandhiAinda não há avaliações

- MultiplesDocumento13 páginasMultiplesNikhil GandhiAinda não há avaliações

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- Class 12 Economics Part 2 PDFDocumento112 páginasClass 12 Economics Part 2 PDFNaveenkumar NeelamAinda não há avaliações

- Philip Kotler Waldemar Pfoertsch Oct. 2006Documento20 páginasPhilip Kotler Waldemar Pfoertsch Oct. 2006Gazal Atul SharmaAinda não há avaliações

- Kotak Mahindra Bank Financial AnalysisDocumento25 páginasKotak Mahindra Bank Financial Analysisheena siddiquiAinda não há avaliações

- Marketing Management MaterialDocumento13 páginasMarketing Management Materialsandeepmachavolu100% (1)

- Varun B015Documento6 páginasVarun B015nischal krishnaAinda não há avaliações

- Comparative Study of Cefpodoxime and To Study The Market Potential For RANBAXY's Product PortfolioDocumento77 páginasComparative Study of Cefpodoxime and To Study The Market Potential For RANBAXY's Product PortfolioUttam Kr PatraAinda não há avaliações

- Marketing Coordinator ResumeDocumento2 páginasMarketing Coordinator ResumeAriandy UtamaAinda não há avaliações

- Sample_MCQ_Topics_1-5Documento12 páginasSample_MCQ_Topics_1-5horace000715Ainda não há avaliações

- Chap5 Creating Long-Term Loyalty RelationshipsDocumento32 páginasChap5 Creating Long-Term Loyalty RelationshipsRajja RashadAinda não há avaliações

- Summary - A Short Course On Swing TradingDocumento2 páginasSummary - A Short Course On Swing TradingsumonAinda não há avaliações

- 2020-ENG Đorić Žarko - Kreativna Ekonomija - Istraživanje Koncepta I Evropska PerspektivaDocumento31 páginas2020-ENG Đorić Žarko - Kreativna Ekonomija - Istraživanje Koncepta I Evropska PerspektivaSandra NikolicAinda não há avaliações

- Toys R Us Case AnalysisDocumento3 páginasToys R Us Case AnalysisHarsh Asthana86% (7)

- Financial Management:: Stock ValuationDocumento57 páginasFinancial Management:: Stock ValuationSarah SaluquenAinda não há avaliações

- Group 13 - Sec F - Does It Payoff Strategies of Two BanksDocumento5 páginasGroup 13 - Sec F - Does It Payoff Strategies of Two BanksAlok CAinda não há avaliações

- Ace Case Study SolutionsDocumento4 páginasAce Case Study SolutionsGunjan joshiAinda não há avaliações

- Igloo Business PlanDocumento26 páginasIgloo Business PlanpratimAinda não há avaliações

- Reliance SIP Insure Application FormDocumento24 páginasReliance SIP Insure Application FormDrashti Investments100% (6)

- Felix Goldstein - Forex, The Ultimate Beginner's Guide To Foreign Exchange Trading 1ra Ed PDFDocumento89 páginasFelix Goldstein - Forex, The Ultimate Beginner's Guide To Foreign Exchange Trading 1ra Ed PDFSheikh GonzaloAinda não há avaliações

- Clinique Marketing PlanDocumento26 páginasClinique Marketing PlanAbdullah Al-Rafi100% (3)

- MarketingDocumento27 páginasMarketingNeradabilli EswarAinda não há avaliações

- Joven CampuganDocumento8 páginasJoven CampuganJovenAinda não há avaliações

- Jan 2005 Income Statement for Variable and Absorption CostingDocumento4 páginasJan 2005 Income Statement for Variable and Absorption CostingWSLeeAinda não há avaliações

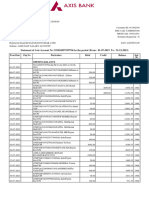

- Account STMT XX9794 31122023Documento16 páginasAccount STMT XX9794 31122023shubhamkasyap443Ainda não há avaliações

- MODULE 8 EntreprenureDocumento10 páginasMODULE 8 EntreprenureQuiel Jomar GarciaAinda não há avaliações

- Nipa Palm Fruit CandyDocumento39 páginasNipa Palm Fruit CandyPrime RietaAinda não há avaliações

- Chapter 2 - Strategic Marketing PlanningDocumento49 páginasChapter 2 - Strategic Marketing PlanningEtpages IgcseAinda não há avaliações

- Case ZerodhaDocumento7 páginasCase ZerodhaMihir JichkarAinda não há avaliações

- Salinan Terjemahan Paper PaymentDocumento16 páginasSalinan Terjemahan Paper PaymentInatamayu ArdikaAinda não há avaliações

- Philamlife vs. SOFDocumento1 páginaPhilamlife vs. SOFMichelleAinda não há avaliações

- Sales and Marketing Assistant Job Description - Google SearchDocumento1 páginaSales and Marketing Assistant Job Description - Google SearchZang Dela CruzAinda não há avaliações