Você também pode gostar

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- Upload A Document 1. Click Upload 2. Select File 3. Wait. File Uploaded.Documento1 páginaUpload A Document 1. Click Upload 2. Select File 3. Wait. File Uploaded.Anantdeep Singh PuriAinda não há avaliações

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Exploring The Volatility of Stock Markets: Indian ExperienceDocumento19 páginasExploring The Volatility of Stock Markets: Indian ExperienceAnantdeep Singh PuriAinda não há avaliações

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Litreture ReviewDocumento17 páginasLitreture Review8866708515Ainda não há avaliações

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Stocks Shares Securities Stock Exchange: Notional ValuesDocumento1 páginaStocks Shares Securities Stock Exchange: Notional ValuesAnantdeep Singh PuriAinda não há avaliações

- Capital Budgeting ProblemsDocumento8 páginasCapital Budgeting ProblemsAnantdeep Singh Puri100% (1)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- Product: The Marketing Mix Is A Business Tool Used inDocumento2 páginasProduct: The Marketing Mix Is A Business Tool Used inAnantdeep Singh PuriAinda não há avaliações

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Banking: For Other Uses, See - "Banker" and "Bankers" Redirect Here. For Other Uses, SeeDocumento20 páginasBanking: For Other Uses, See - "Banker" and "Bankers" Redirect Here. For Other Uses, SeeAnantdeep Singh PuriAinda não há avaliações

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- Taxation of Individuals QuizzerDocumento38 páginasTaxation of Individuals QuizzerCookie Pookie BallerShopAinda não há avaliações

- Ride Details Bill Details: Jitendra ThakurDocumento3 páginasRide Details Bill Details: Jitendra ThakurNimmi Baisa TravelsAinda não há avaliações

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Bitumen - Emulsion Rates 01.01.2017Documento8 páginasBitumen - Emulsion Rates 01.01.2017karunamoorthi_p2209Ainda não há avaliações

- Tutorial 9 Questions Mfrs 112 Income Taxes (Part 1) - Lazar and HuangDocumento4 páginasTutorial 9 Questions Mfrs 112 Income Taxes (Part 1) - Lazar and HuangLee HansAinda não há avaliações

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Orderconfirmation 2211375989 From 01.09.2021: VWR International GMBH AustriaDocumento2 páginasOrderconfirmation 2211375989 From 01.09.2021: VWR International GMBH Austriaarman1704Ainda não há avaliações

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Dispute Transaction FormDocumento1 páginaDispute Transaction FormAli Naeem SheikhAinda não há avaliações

- College Toga Order Slip 100520 RevisedDocumento2 páginasCollege Toga Order Slip 100520 RevisedBLUE GOLDAinda não há avaliações

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- Compendium On Local Property Taxes & Other Taxes in The NCRDocumento35 páginasCompendium On Local Property Taxes & Other Taxes in The NCRBo DistAinda não há avaliações

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Transaction Receipt: ToheebatDocumento1 páginaTransaction Receipt: ToheebatSam AduraAinda não há avaliações

- Schedule of Fees & Charges November 2021 (English)Documento1 páginaSchedule of Fees & Charges November 2021 (English)Tabish JazbiAinda não há avaliações

- Gis 305782 01111327Documento2 páginasGis 305782 01111327goz.olmedo1998Ainda não há avaliações

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Invoice: Bo o King.c o M B.VDocumento1 páginaInvoice: Bo o King.c o M B.VJuan AugustinAinda não há avaliações

- Income Tax Calculator For IndiaDocumento4 páginasIncome Tax Calculator For Indiamahalakshmi muruganAinda não há avaliações

- Cta CaseDocumento10 páginasCta Caselucial_68Ainda não há avaliações

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- Bank of AmericaDocumento14 páginasBank of AmericagisellaolsenAinda não há avaliações

- Income Tax Return Forms ArdraDocumento25 páginasIncome Tax Return Forms ArdraGangothri AsokAinda não há avaliações

- Cash ReceiptDocumento40 páginasCash ReceiptAneesh ChandranAinda não há avaliações

- Checks Issued by The City of Boise Idaho - 4Documento52 páginasChecks Issued by The City of Boise Idaho - 4Mark ReinhardtAinda não há avaliações

- Taxation Solution 2018 MarchDocumento11 páginasTaxation Solution 2018 MarchNg GraceAinda não há avaliações

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- MG 3027 TAXATION - Week 10 Income From Self-Employment-Computation of IncomeDocumento34 páginasMG 3027 TAXATION - Week 10 Income From Self-Employment-Computation of IncomeSyed SafdarAinda não há avaliações

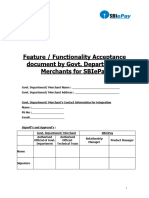

- Features & Functionality StatementDocumento8 páginasFeatures & Functionality Statementvijay narwadeAinda não há avaliações

- C2 Course Test 5Documento16 páginasC2 Course Test 5Tinashe MashoyoyaAinda não há avaliações

- TDS 23-24Documento2 páginasTDS 23-24Taharat Ahmed ChowdhuryAinda não há avaliações

- Bir EtformDocumento3 páginasBir EtformrjgingerpenAinda não há avaliações

- Cost-Sheet: Terms & ConditionDocumento2 páginasCost-Sheet: Terms & ConditionMohammedRahimAinda não há avaliações

- Tax Guide 2022/2023: Right People. Right Size. Right SolutionsDocumento60 páginasTax Guide 2022/2023: Right People. Right Size. Right Solutionstinashe mashoyoyaAinda não há avaliações

- Gmail - Guest Reservations - Reservation Confirmation #R4448147806Documento4 páginasGmail - Guest Reservations - Reservation Confirmation #R4448147806amarenterpries01Ainda não há avaliações

- Moza Jahangirabad Acc#1226203518874 Moza Jahangirabad Acc#1226203518874 Moza Jahangirabad Acc#1226203518874Documento1 páginaMoza Jahangirabad Acc#1226203518874 Moza Jahangirabad Acc#1226203518874 Moza Jahangirabad Acc#1226203518874Shahmeer - ul-HassanAinda não há avaliações

- Chapter 3 PayrollDocumento12 páginasChapter 3 Payrollawlachew100% (2)

- SBI BANK StatementDocumento15 páginasSBI BANK StatementChannel onetowAinda não há avaliações