Você também pode gostar

- IDC Historic Rehabilitation Tax Credit Report - March 16, 2011Documento16 páginasIDC Historic Rehabilitation Tax Credit Report - March 16, 2011robertharding22Ainda não há avaliações

- FY2019 Proposed BudgetDocumento134 páginasFY2019 Proposed BudgetFauquier NowAinda não há avaliações

- Mobile Police Department Crime Statistics 2023Documento18 páginasMobile Police Department Crime Statistics 2023WALAAinda não há avaliações

- ReportDocumento7 páginasReportRecordTrac - City of OaklandAinda não há avaliações

- FBI Crime Statistics 2011 SummaryDocumento2 páginasFBI Crime Statistics 2011 SummaryRoy SteeleAinda não há avaliações

- Coca Cola CompanyDocumento6 páginasCoca Cola CompanyAnwesha Dev ChaudharyAinda não há avaliações

- Xavier Institute of ManagementDocumento9 páginasXavier Institute of ManagementSidhant NayakAinda não há avaliações

- Obboy Architects Company PortfolioDocumento112 páginasObboy Architects Company PortfolioMahzub HasanAinda não há avaliações

- FY2025 NYS Executive Budget Briefing BookDocumento144 páginasFY2025 NYS Executive Budget Briefing BookNews 8 WROCAinda não há avaliações

- First PrelimsDocumento41 páginasFirst PrelimsKath OAinda não há avaliações

- File-Sample 2MBDocumento2 páginasFile-Sample 2MBjsjahidhAinda não há avaliações

- 2013 Mayor's Proposed BudgetDocumento407 páginas2013 Mayor's Proposed BudgetBridgeportCTAinda não há avaliações

- September 4 2012 Complete AgendaDocumento53 páginasSeptember 4 2012 Complete AgendaTown of Ocean CityAinda não há avaliações

- Website Audit Project ReportDocumento27 páginasWebsite Audit Project ReportKim Sydow CampbellAinda não há avaliações

- Portfolio and Investment Analysis - Students-1 2Documento74 páginasPortfolio and Investment Analysis - Students-1 2Abdullahi AbdikadirAinda não há avaliações

- Guidelines On Real Estate Investment Trusts: Issued By: Securities Commission Effective: 21 August 2008Documento162 páginasGuidelines On Real Estate Investment Trusts: Issued By: Securities Commission Effective: 21 August 2008Nik Najwa100% (1)

- ZombieSurvival 2Documento8 páginasZombieSurvival 2Diana GhalyAinda não há avaliações

- Pollution EssayDocumento4 páginasPollution EssayKhadijah AsrarAinda não há avaliações

- Stock Portfolio Analysis ProjectDocumento18 páginasStock Portfolio Analysis Projectapi-515224062Ainda não há avaliações

- Question: Official Crime Statistics Do Not Show The Pattern, Extent and Coverage of Crime in Zimbabwe. Critically Evaluate This StatementDocumento7 páginasQuestion: Official Crime Statistics Do Not Show The Pattern, Extent and Coverage of Crime in Zimbabwe. Critically Evaluate This StatementKudakwashe Shumba WeMhaziAinda não há avaliações

- Bài tập bổ trợ Anh 8 Global Bùi Văn Vinh. 1ST TERM TESTDocumento17 páginasBài tập bổ trợ Anh 8 Global Bùi Văn Vinh. 1ST TERM TESTTrần Thị Lệ Hồng100% (1)

- Cleveland Crime StatisticsDocumento25 páginasCleveland Crime StatisticsWKYC.comAinda não há avaliações

- 1668419557536 (2)Documento9 páginas1668419557536 (2)Jom JeanAinda não há avaliações

- Math Batch ReviewerpdfDocumento11 páginasMath Batch ReviewerpdfjayceAinda não há avaliações

- Lone Star College District $149.78 Million Limited Tax General Obligation Bonds Official Statement, 2008Documento142 páginasLone Star College District $149.78 Million Limited Tax General Obligation Bonds Official Statement, 2008Texas WatchdogAinda não há avaliações

- UBC Okanagan Calendar College of Graduate StudiesDocumento89 páginasUBC Okanagan Calendar College of Graduate Studiesrobertofca2266Ainda não há avaliações

- City of Carmel-By-The-Sea City Council Staff Report: TO: Submit T Ed By: Approved byDocumento4 páginasCity of Carmel-By-The-Sea City Council Staff Report: TO: Submit T Ed By: Approved byL. A. PatersonAinda não há avaliações

- RBC - ORCC - Estimates Down - 3Q20 Review Updating Our - 13 PagesDocumento13 páginasRBC - ORCC - Estimates Down - 3Q20 Review Updating Our - 13 PagesSagar PatelAinda não há avaliações

- Research Proposal - (Monisha-20D1977)Documento13 páginasResearch Proposal - (Monisha-20D1977)Moni 47Ainda não há avaliações

- Internal AuditDocumento11 páginasInternal AuditSara MujawarAinda não há avaliações

- 18 Company Portfolio Construction ReportDocumento35 páginas18 Company Portfolio Construction ReportAnik DeyAinda não há avaliações

- All IL Corporate Filings by The Save-A-Life Foundation (SALF) Including 9/17/09 Dissolution (1993-2009)Documento48 páginasAll IL Corporate Filings by The Save-A-Life Foundation (SALF) Including 9/17/09 Dissolution (1993-2009)Peter M. HeimlichAinda não há avaliações

- San Antonio Police Department Crime Statistics For 2021Documento14 páginasSan Antonio Police Department Crime Statistics For 2021KENS 5Ainda não há avaliações

- Barclays - What Makes A Great Industrial CompanyDocumento37 páginasBarclays - What Makes A Great Industrial CompanyRandy LaheyAinda não há avaliações

- MBAZ514Documento204 páginasMBAZ514zivainyaudeAinda não há avaliações

- Baltimore City Fiscal Year 2024 Preliminary BudgetDocumento190 páginasBaltimore City Fiscal Year 2024 Preliminary BudgetChris BerinatoAinda não há avaliações

- Course Content Form: Practical Accounting ProceduresDocumento2 páginasCourse Content Form: Practical Accounting ProceduresOscar I. ValenzuelaAinda não há avaliações

- ICIC Smaple Doc222Documento494 páginasICIC Smaple Doc222samkskingsAinda não há avaliações

- TPG Specialty Lending ResearchDocumento25 páginasTPG Specialty Lending ResearchaaquibnasirAinda não há avaliações

- Santa Clara County Department of Child Support Services 880 Ridder Park DR SAN JOSE CA 95131-2486Documento4 páginasSanta Clara County Department of Child Support Services 880 Ridder Park DR SAN JOSE CA 95131-2486Good2cuAinda não há avaliações

- Updated Operational Circular For Issue and Listing of Commercial Paper - April 13 2022Documento120 páginasUpdated Operational Circular For Issue and Listing of Commercial Paper - April 13 2022Vani PattnaikAinda não há avaliações

- Pir Ifrs 3 Report Feedback StatementDocumento38 páginasPir Ifrs 3 Report Feedback StatementPIA MICHAELLA ILAGAAinda não há avaliações

- Cincinnati 2022 Crime StatisticsDocumento37 páginasCincinnati 2022 Crime StatisticsWVXU NewsAinda não há avaliações

- MUHAS Internal Audit Charter 2013Documento16 páginasMUHAS Internal Audit Charter 2013Audifax JohnAinda não há avaliações

- Quick Start Report - 2011-12 - Final 11.5.10Documento50 páginasQuick Start Report - 2011-12 - Final 11.5.10New York SenateAinda não há avaliações

- Economics Group: Interest Rate WeeklyDocumento3 páginasEconomics Group: Interest Rate Weeklyd_stepien43098Ainda não há avaliações

- Van Hoisington Letter, Q3 2011Documento5 páginasVan Hoisington Letter, Q3 2011Elliott WaveAinda não há avaliações

- Analysis of CBO's August 2011 Baseline and Update of CRFB Realistic Baseline August 24, 2011Documento6 páginasAnalysis of CBO's August 2011 Baseline and Update of CRFB Realistic Baseline August 24, 2011Committee For a Responsible Federal BudgetAinda não há avaliações

- Enacted Budget Report 2020-21Documento22 páginasEnacted Budget Report 2020-21Luke ParsnowAinda não há avaliações

- Review of The Financial Plan of The City of New York: Report 10-2016Documento36 páginasReview of The Financial Plan of The City of New York: Report 10-2016Nick ReismanAinda não há avaliações

- November Econ OutlookDocumento13 páginasNovember Econ OutlookccanioAinda não há avaliações

- Mid Session Review FY2011Documento9 páginasMid Session Review FY2011Committee For a Responsible Federal BudgetAinda não há avaliações

- CRFB Analysis of Jan 2011 BaselineDocumento7 páginasCRFB Analysis of Jan 2011 BaselineCommittee For a Responsible Federal BudgetAinda não há avaliações

- Autumn Statement 2011Documento9 páginasAutumn Statement 2011IPPRAinda não há avaliações

- Stoking Sentiments - Grp6 Sec BDocumento39 páginasStoking Sentiments - Grp6 Sec BrajivAinda não há avaliações

- 2011 Quick StartDocumento24 páginas2011 Quick StartNick ReismanAinda não há avaliações

- Budget Response FY 2012 FINALDocumento17 páginasBudget Response FY 2012 FINALCeleste KatzAinda não há avaliações

- April 2009 Economic UpdateDocumento4 páginasApril 2009 Economic UpdateMinnesota Public RadioAinda não há avaliações

- April 2013 State Revenues Exceed Forecast in February and MarchDocumento4 páginasApril 2013 State Revenues Exceed Forecast in February and Marchtom_scheckAinda não há avaliações

- Analysis of The Presidents 2012 BudgetDocumento9 páginasAnalysis of The Presidents 2012 BudgetCommittee For a Responsible Federal BudgetAinda não há avaliações

- Hedge Fund White Paper Teachout FinalDocumento18 páginasHedge Fund White Paper Teachout Finalhangman0000Ainda não há avaliações

- RAISE UP NY Slide DeckDocumento26 páginasRAISE UP NY Slide Deckhangman0000Ainda não há avaliações

- #NYInequalityDocumento34 páginas#NYInequalityhangman0000Ainda não há avaliações

- NY Inequality Slide Deck VRSN ADocumento34 páginasNY Inequality Slide Deck VRSN Ahangman0000Ainda não há avaliações

- Ecosystem Services of The Congo Basin ForestsDocumento33 páginasEcosystem Services of The Congo Basin ForestsGlobal Canopy Programme100% (3)

- Synopsis Self-Sustainable CommunityDocumento3 páginasSynopsis Self-Sustainable Communityankitankit yadavAinda não há avaliações

- Bbob Current AffairsDocumento28 páginasBbob Current AffairsGangwar AnkitAinda não há avaliações

- Asx S&P 200Documento15 páginasAsx S&P 200abcfactcheckAinda não há avaliações

- Financial and Physical Performance Report FORMATDocumento9 páginasFinancial and Physical Performance Report FORMATJeremiah TrinidadAinda não há avaliações

- Filt RosDocumento6 páginasFilt RosSalva SalazarAinda não há avaliações

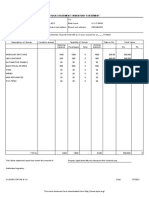

- Stock Statement Format For Bank LoanDocumento1 páginaStock Statement Format For Bank Loanpsycho Neha40% (5)

- L 1Documento5 páginasL 1Elizabeth Espinosa ManilagAinda não há avaliações

- Downtown Design ExhibitorsDocumento21 páginasDowntown Design ExhibitorsIan DañgananAinda não há avaliações

- Business Economics PPT Chap 1Documento18 páginasBusiness Economics PPT Chap 1david sughapriyaAinda não há avaliações

- YUL YYZ: TICKET - ConfirmedDocumento3 páginasYUL YYZ: TICKET - ConfirmedRamuAinda não há avaliações

- PPSAS 28 - Financial Instruments - Presentation 3-18-2013Documento3 páginasPPSAS 28 - Financial Instruments - Presentation 3-18-2013Christian Ian LimAinda não há avaliações

- List of TSD Facilities July 31 2019Documento15 páginasList of TSD Facilities July 31 2019Emrick SantiagoAinda não há avaliações

- Pipistrel Alpha Trainer e Learning 2020Documento185 páginasPipistrel Alpha Trainer e Learning 2020Kostas RossidisAinda não há avaliações

- India Completing Inv UniverseDocumento16 páginasIndia Completing Inv UniverseKushal ManupatiAinda não há avaliações

- Greenberg-Megaworld Demand LetterDocumento2 páginasGreenberg-Megaworld Demand LetterLilian RoqueAinda não há avaliações

- Pune MetroDocumento11 páginasPune MetroGanesh NichalAinda não há avaliações

- LP BrochureDocumento2 páginasLP BrochureSyed Abdul RafeyAinda não há avaliações

- B2B Marketing - MRFDocumento13 páginasB2B Marketing - MRFMohit JainAinda não há avaliações

- Section 125 Digested CasesDocumento6 páginasSection 125 Digested CasesRobAinda não há avaliações

- Its The Economy, Student! by Gloria Macapagal ArroyoDocumento9 páginasIts The Economy, Student! by Gloria Macapagal ArroyodabomeisterAinda não há avaliações

- Truffle MarketDocumento14 páginasTruffle MarketAnonymous zL3aOc9Ainda não há avaliações

- Understanding ManagementDocumento35 páginasUnderstanding ManagementXian-liAinda não há avaliações

- Assessment of The Kosovo Innovation SystemDocumento113 páginasAssessment of The Kosovo Innovation SystemOECD Global RelationsAinda não há avaliações

- Herbert HooverDocumento4 páginasHerbert HooverZuñiga Salazar Hamlet EnocAinda não há avaliações

- TCSDocumento4 páginasTCSjayasree_reddyAinda não há avaliações

- Africa World AirlinesDocumento1 páginaAfrica World AirlinesKwame YeboahAinda não há avaliações

- 6 Zimbabwean DollarDocumento32 páginas6 Zimbabwean DollarArjun Nayak100% (1)

- Oceangoing Ships 2007 PDFDocumento102 páginasOceangoing Ships 2007 PDFaleventAinda não há avaliações

- Business Taxation Made EasyDocumento2 páginasBusiness Taxation Made EasyNatsumi T. ViceralAinda não há avaliações

- When Helping Hurts: How to Alleviate Poverty Without Hurting the Poor . . . and YourselfNo EverandWhen Helping Hurts: How to Alleviate Poverty Without Hurting the Poor . . . and YourselfNota: 5 de 5 estrelas5/5 (36)

- High-Risers: Cabrini-Green and the Fate of American Public HousingNo EverandHigh-Risers: Cabrini-Green and the Fate of American Public HousingAinda não há avaliações

- Workin' Our Way Home: The Incredible True Story of a Homeless Ex-Con and a Grieving Millionaire Thrown Together to Save Each OtherNo EverandWorkin' Our Way Home: The Incredible True Story of a Homeless Ex-Con and a Grieving Millionaire Thrown Together to Save Each OtherAinda não há avaliações

- The Meth Lunches: Food and Longing in an American CityNo EverandThe Meth Lunches: Food and Longing in an American CityNota: 5 de 5 estrelas5/5 (5)

- Heartland: A Memoir of Working Hard and Being Broke in the Richest Country on EarthNo EverandHeartland: A Memoir of Working Hard and Being Broke in the Richest Country on EarthNota: 4 de 5 estrelas4/5 (188)

- The Great Displacement: Climate Change and the Next American MigrationNo EverandThe Great Displacement: Climate Change and the Next American MigrationNota: 4.5 de 5 estrelas4.5/5 (32)

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassNo EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassAinda não há avaliações

- Budget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.No EverandBudget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.Nota: 5 de 5 estrelas5/5 (89)

- You Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantNo EverandYou Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantNota: 4 de 5 estrelas4/5 (104)

- Poor Economics: A Radical Rethinking of the Way to Fight Global PovertyNo EverandPoor Economics: A Radical Rethinking of the Way to Fight Global PovertyNota: 4.5 de 5 estrelas4.5/5 (263)

- Hillbilly Elegy: A Memoir of a Family and Culture in CrisisNo EverandHillbilly Elegy: A Memoir of a Family and Culture in CrisisNota: 4 de 5 estrelas4/5 (4284)

- Same Kind of Different As Me Movie Edition: A Modern-Day Slave, an International Art Dealer, and the Unlikely Woman Who Bound Them TogetherNo EverandSame Kind of Different As Me Movie Edition: A Modern-Day Slave, an International Art Dealer, and the Unlikely Woman Who Bound Them TogetherNota: 4 de 5 estrelas4/5 (686)

- IF YOU SEE THEM: Young, Unhoused, and Alone in America.No EverandIF YOU SEE THEM: Young, Unhoused, and Alone in America.Ainda não há avaliações

- Money Made Easy: How to Budget, Pay Off Debt, and Save MoneyNo EverandMoney Made Easy: How to Budget, Pay Off Debt, and Save MoneyNota: 5 de 5 estrelas5/5 (1)

- Nickel and Dimed: On (Not) Getting By in AmericaNo EverandNickel and Dimed: On (Not) Getting By in AmericaNota: 4 de 5 estrelas4/5 (186)

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsNo EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsAinda não há avaliações

- The Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsNo EverandThe Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsAinda não há avaliações

- CDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsNo EverandCDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsNota: 4 de 5 estrelas4/5 (4)

- Who Really Owns Ireland: How we became tenants in our own land - and what we can do about itNo EverandWho Really Owns Ireland: How we became tenants in our own land - and what we can do about itAinda não há avaliações

- Heartland: A Memoir of Working Hard and Being Broke in the Richest Country on EarthNo EverandHeartland: A Memoir of Working Hard and Being Broke in the Richest Country on EarthNota: 4 de 5 estrelas4/5 (269)

- The Best Team Wins: The New Science of High PerformanceNo EverandThe Best Team Wins: The New Science of High PerformanceNota: 4.5 de 5 estrelas4.5/5 (31)

- Life at the Bottom: The Worldview That Makes the UnderclassNo EverandLife at the Bottom: The Worldview That Makes the UnderclassNota: 5 de 5 estrelas5/5 (30)

- Nickel and Dimed: On (Not) Getting By in AmericaNo EverandNickel and Dimed: On (Not) Getting By in AmericaNota: 3.5 de 5 estrelas3.5/5 (197)