Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Employee Details Payment & Working Days Details Location Details Nitu SinghDocumento1 páginaEmployee Details Payment & Working Days Details Location Details Nitu SinghRohit raagAinda não há avaliações

- Receivables (Part 2 - Long Term)Documento56 páginasReceivables (Part 2 - Long Term)Jimbo ManalastasAinda não há avaliações

- General Banking LawDocumento23 páginasGeneral Banking LawRANDAN SADIQAinda não há avaliações

- Daily Walk in Jan 2021Documento177 páginasDaily Walk in Jan 2021fahad hassanAinda não há avaliações

- HDFC Bank Credit Cards GSTIN: 33AAACH2702H2Z6 HSN Code - 9971Documento1 páginaHDFC Bank Credit Cards GSTIN: 33AAACH2702H2Z6 HSN Code - 9971srinivas padalaAinda não há avaliações

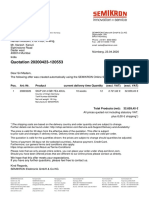

- Quotation 20200423-120553: Pos. Art.-Nr. Product Current Delivery Time Quantity Unit Price (Excl. VAT) Total (Excl. VAT)Documento1 páginaQuotation 20200423-120553: Pos. Art.-Nr. Product Current Delivery Time Quantity Unit Price (Excl. VAT) Total (Excl. VAT)kanrinareshAinda não há avaliações

- GST ChallanDocumento2 páginasGST ChallanArun KumarAinda não há avaliações

- Statement 125601000023857Documento10 páginasStatement 125601000023857rowdy2010Ainda não há avaliações

- BITS HD-2013 Print Challan Form .Documento1 páginaBITS HD-2013 Print Challan Form .Naveen Kumar SinhaAinda não há avaliações

- Account StatementDocumento4 páginasAccount Statementvickey chandraAinda não há avaliações

- Adv Fincnce MCQDocumento8 páginasAdv Fincnce MCQGLEN GOMESAinda não há avaliações

- Bandhan Bank MbaDocumento15 páginasBandhan Bank MbaAmanNandaAinda não há avaliações

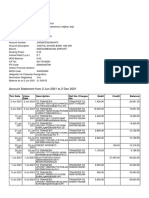

- Account Statement From 2 Jun 2021 To 2 Dec 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento6 páginasAccount Statement From 2 Jun 2021 To 2 Dec 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRavi PallaAinda não há avaliações

- Negotiable Instruments-Asanka KarunaratnaDocumento19 páginasNegotiable Instruments-Asanka KarunaratnaLahiru ChathurangaAinda não há avaliações

- Rib A Uk Chartered FormDocumento8 páginasRib A Uk Chartered FormralucaelenapricopAinda não há avaliações

- Accounts Cec 1year Test PaparDocumento2 páginasAccounts Cec 1year Test PaparMohammad MoinuddinAinda não há avaliações

- International Finance 5Documento36 páginasInternational Finance 5Hu Jia QuenAinda não há avaliações

- 92611902-KrugmanMacro SM Ch19 PDFDocumento6 páginas92611902-KrugmanMacro SM Ch19 PDFAlejandro Fernandez RodriguezAinda não há avaliações

- Credit Authorisation SchemeDocumento6 páginasCredit Authorisation SchemeOngwang KonyakAinda não há avaliações

- BFS PracticeDocumento61 páginasBFS PracticeBhagawath KishoreAinda não há avaliações

- Statement of Account For 4020cdiv599236: Bajaj Finance LimitedDocumento3 páginasStatement of Account For 4020cdiv599236: Bajaj Finance LimitedRudrali HitechAinda não há avaliações

- Third Space Learning Compound Interest GCSE Worksheet 1Documento12 páginasThird Space Learning Compound Interest GCSE Worksheet 1erin zietsmanAinda não há avaliações

- Next Generation Loyalty Management Systems: Trends, Challenges, and RecommendationsDocumento24 páginasNext Generation Loyalty Management Systems: Trends, Challenges, and Recommendationskolluru hariAinda não há avaliações

- LPB 94th JAIBBDocumento4 páginasLPB 94th JAIBBMahmudul HassanAinda não há avaliações

- Wachtell, Lipton, Rosen Katz: New - York, New York 10173Documento11 páginasWachtell, Lipton, Rosen Katz: New - York, New York 10173Matthew Russell LeeAinda não há avaliações

- Money ManagerDocumento32 páginasMoney ManagerMuhammad ZainiansyahAinda não há avaliações

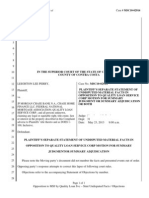

- Plaintiff's Statement of Undisputed Facts To QLSDocumento8 páginasPlaintiff's Statement of Undisputed Facts To QLSLee PerryAinda não há avaliações

- Fa Q Son RestructuringDocumento4 páginasFa Q Son RestructuringSoma ShekharAinda não há avaliações

- Paid PaidDocumento1 páginaPaid PaidJash SolankiAinda não há avaliações

- Card Cancellation DisclaimerDocumento1 páginaCard Cancellation Disclaimerambermikaela.siAinda não há avaliações