Você também pode gostar

- #IndiaStockExchange #BSE Update On 24th June 2015Documento2 páginas#IndiaStockExchange #BSE Update On 24th June 2015Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- Foreign Direct Investment in Equity Market in IndiaDocumento4 páginasForeign Direct Investment in Equity Market in IndiaJhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Wheat Production From 2010 To 2014Documento4 páginasIndia's Wheat Production From 2010 To 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's UREA Trade On 2013-14 and 2014-15 Up To November 2014.Documento3 páginasIndia's UREA Trade On 2013-14 and 2014-15 Up To November 2014.Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Per Capita Food Grain For 2014Documento3 páginasIndia's Per Capita Food Grain For 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- MSMEs or Micro Small and Medium Enterprses Share in India Exports 2013-2014Documento4 páginasMSMEs or Micro Small and Medium Enterprses Share in India Exports 2013-2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India Coir Trade From April To October 2014Documento4 páginasIndia Coir Trade From April To October 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Rice Trade For 2014Documento5 páginasIndia's Rice Trade For 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

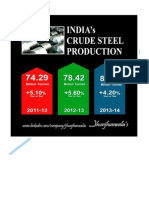

- India's Crude Steel Production Estimate For 2014 To 2017Documento3 páginasIndia's Crude Steel Production Estimate For 2014 To 2017Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Diamond Reserves With Diamond Trade Update For 2014Documento6 páginasIndia's Diamond Reserves With Diamond Trade Update For 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- Foreign Institutional Investors Investment in India During 2014-15 Until 27th November 2014Documento3 páginasForeign Institutional Investors Investment in India During 2014-15 Until 27th November 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Coal Reserves To Last 100 YearsDocumento3 páginasIndia's Coal Reserves To Last 100 YearsJhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Coal Production For Last 5 Years Upto October 2014Documento2 páginasIndia's Coal Production For Last 5 Years Upto October 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India Crude Steel Production From 2011-2014Documento4 páginasIndia Crude Steel Production From 2011-2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- Commercially Operating Nuclear Reactors in The World at The End of 2013Documento4 páginasCommercially Operating Nuclear Reactors in The World at The End of 2013Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Import and Export Update For September and December 2014Documento16 páginasIndia's Import and Export Update For September and December 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Methane Hydrates Reserves 25th November 2014Documento3 páginasIndia's Methane Hydrates Reserves 25th November 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Coal Bed Methane Production For Last 3 Years With Current Year 2014-15 (Upto 31 Oct 2014)Documento3 páginasIndia's Coal Bed Methane Production For Last 3 Years With Current Year 2014-15 (Upto 31 Oct 2014)Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Tourism Sector Performance For January and October 2014Documento15 páginasIndia's Tourism Sector Performance For January and October 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Kharif and Rabi Crops Area Coverage For October and January 2014Documento10 páginasIndia's Kharif and Rabi Crops Area Coverage For October and January 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- Foreign Investment Promotion Board Approves 12 Proposals of Foreign Direct Investment in India As On 19th December 2014Documento27 páginasForeign Investment Promotion Board Approves 12 Proposals of Foreign Direct Investment in India As On 19th December 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- Global Central Banks Highlights For Monetary Policy Rates From 23rd To 30th September 2014Documento11 páginasGlobal Central Banks Highlights For Monetary Policy Rates From 23rd To 30th September 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- Fuel Price Change For Petrol, Diesel, and JetFuel in IndiaDocumento11 páginasFuel Price Change For Petrol, Diesel, and JetFuel in IndiaJhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Mineral Production in Month of August 2014Documento3 páginasIndia's Mineral Production in Month of August 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- Global Central Banks Highlights For Monetary Policy Rates For October 2014Documento31 páginasGlobal Central Banks Highlights For Monetary Policy Rates For October 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- Indians Railways Revenue Earnings With Freight Traffic During April To October 2014Documento18 páginasIndians Railways Revenue Earnings With Freight Traffic During April To October 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India's Index of Eight Core Industries From June To November 2014Documento57 páginasIndia's Index of Eight Core Industries From June To November 2014Jhunjhunwalas Digital Finance & Business Info Library100% (1)

- India 'S Total Kharif Crop Sowing Area As On July and August 2014Documento6 páginasIndia 'S Total Kharif Crop Sowing Area As On July and August 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- India Tax Collection From April To November 2014Documento11 páginasIndia Tax Collection From April To November 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- Indian Currency Rupee Exchange Rate of 19 Foreign Currencies Relating To Import and Export Goods From July To September 2014Documento5 páginasIndian Currency Rupee Exchange Rate of 19 Foreign Currencies Relating To Import and Export Goods From July To September 2014Jhunjhunwalas Digital Finance & Business Info LibraryAinda não há avaliações

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- 7-12. (Byron, Inc.)Documento2 páginas7-12. (Byron, Inc.)Gray JavierAinda não há avaliações

- MTH 1290228Documento8 páginasMTH 1290228Pickle RickAinda não há avaliações

- Asset-Liability Management in BanksDocumento42 páginasAsset-Liability Management in Banksnike_4008a100% (1)

- FIN 350 Homework SolutionsDocumento6 páginasFIN 350 Homework SolutionsGomishChawlaAinda não há avaliações

- Himanshu Sharma - Detection of Financial Statement Fraud Using Decision Tree Classifiers - 2013Documento23 páginasHimanshu Sharma - Detection of Financial Statement Fraud Using Decision Tree Classifiers - 2013Ramakrishna GAinda não há avaliações

- Finance Projects TopicsDocumento29 páginasFinance Projects TopicsYumna KamranAinda não há avaliações

- Salient Features of RA 9700Documento16 páginasSalient Features of RA 9700histosol100% (1)

- Overseas Direct Investment ChecklistDocumento5 páginasOverseas Direct Investment ChecklistAnil Palan0% (1)

- Hongkong DisneyDocumento22 páginasHongkong DisneyLiam LêAinda não há avaliações

- Taxation and Investment Code SummaryDocumento10 páginasTaxation and Investment Code SummaryJustin Robert RoqueAinda não há avaliações

- India Infoline Risk and Return AnalysisDocumento58 páginasIndia Infoline Risk and Return AnalysisDileep JohnnyAinda não há avaliações

- BU111 Final December 4 /5 2018: Megan Corbett, Sam Sells, Lauren Carroll, Alex ClaytonDocumento97 páginasBU111 Final December 4 /5 2018: Megan Corbett, Sam Sells, Lauren Carroll, Alex ClaytonJugaadAinda não há avaliações

- Uzma BHD - KN ReportDocumento11 páginasUzma BHD - KN ReportAzmi MahamadAinda não há avaliações

- BRITANNIADocumento3 páginasBRITANNIAsalmaAinda não há avaliações

- Tax Saving StepsDocumento10 páginasTax Saving StepsDheeraj SethAinda não há avaliações

- Strategy Formulation and Implementation For An Expansion Strategy BlaBlaCar Middle East Aboud KhederchahDocumento9 páginasStrategy Formulation and Implementation For An Expansion Strategy BlaBlaCar Middle East Aboud KhederchahaboudgkAinda não há avaliações

- Ratio Analysis Case Study SolutionDocumento7 páginasRatio Analysis Case Study SolutionRanjuAinda não há avaliações

- Principles of Finance 6th Edition Besley Solutions ManualDocumento36 páginasPrinciples of Finance 6th Edition Besley Solutions Manualalexandrapearli5zj100% (27)

- Quiao V QuiaoDocumento3 páginasQuiao V QuiaoSimon James SemillaAinda não há avaliações

- Kim Eng Research (14042011)Documento9 páginasKim Eng Research (14042011)SG PropTalkAinda não há avaliações

- Tiffany and CoDocumento49 páginasTiffany and CoRajesh Lakhanotra83% (6)

- Ciq Financials Methodology PDFDocumento25 páginasCiq Financials Methodology PDFbhaskar2400Ainda não há avaliações

- 3 Crispin Odey PresentationDocumento23 páginas3 Crispin Odey PresentationWindsor1801Ainda não há avaliações

- Ben Graham Calculations Template - FinboxDocumento8 páginasBen Graham Calculations Template - FinboxDario RAinda não há avaliações

- Cambridge Target Score Final TestDocumento52 páginasCambridge Target Score Final TestFotini AnaniadouAinda não há avaliações

- Senior' ProjectDocumento265 páginasSenior' ProjectAayushi ChandwaniAinda não há avaliações

- Lecture 14 - Mutual Fund Theorem and Covariance Pricing TheoremsDocumento16 páginasLecture 14 - Mutual Fund Theorem and Covariance Pricing TheoremsLuis Aragonés FerriAinda não há avaliações

- An Overview of Sonali Bank LimitedDocumento5 páginasAn Overview of Sonali Bank LimitedCapricious ShovonAinda não há avaliações

- Quiz.2.TimevalueofMoney - Answer 1Documento6 páginasQuiz.2.TimevalueofMoney - Answer 1anhAinda não há avaliações

- Review Questions Volume 1 - Chapter 28Documento2 páginasReview Questions Volume 1 - Chapter 28YelenochkaAinda não há avaliações