Você também pode gostar

- ANHD 2016 Economic Opportunity PosterDocumento1 páginaANHD 2016 Economic Opportunity PosterNorman OderAinda não há avaliações

- HSBC Institutional Trust (Trustee of Starhill Global REIT) V Toshin Deve...Documento34 páginasHSBC Institutional Trust (Trustee of Starhill Global REIT) V Toshin Deve...Harpott GhantaAinda não há avaliações

- Okp 080114Documento4 páginasOkp 080114Harpott GhantaAinda não há avaliações

- FileStore - Pdfstore - LectureSpeech - NUSS Professorship Lecture - FromThirdWorldToFirstDocumento26 páginasFileStore - Pdfstore - LectureSpeech - NUSS Professorship Lecture - FromThirdWorldToFirstHarpott GhantaAinda não há avaliações

- Re Wan Soon Construction Judicial Managers Entitlement to Sale ProceedsDocumento6 páginasRe Wan Soon Construction Judicial Managers Entitlement to Sale ProceedsHarpott GhantaAinda não há avaliações

- Happy Nails Fa 1Documento14 páginasHappy Nails Fa 1Harpott GhantaAinda não há avaliações

- Voidable Transactions in The Context of InsolvencyDocumento7 páginasVoidable Transactions in The Context of InsolvencyHarpott GhantaAinda não há avaliações

- Companies (Application of Bankruptcy Act) RegulationsDocumento3 páginasCompanies (Application of Bankruptcy Act) RegulationsHarpott GhantaAinda não há avaliações

- G2 - List of Videos On AdvocacyDocumento1 páginaG2 - List of Videos On AdvocacyHarpott GhantaAinda não há avaliações

- Aspen Publishers - Drafting Contracts - How and Why Lawyers Do What They Do 2E - Tina LDocumento9 páginasAspen Publishers - Drafting Contracts - How and Why Lawyers Do What They Do 2E - Tina LHarpott Ghanta20% (5)

- Asset Based Lending in Singapore Jun 2011Documento14 páginasAsset Based Lending in Singapore Jun 2011Harpott GhantaAinda não há avaliações

- SAcL IP Law SummaryDocumento15 páginasSAcL IP Law SummaryHarpott GhantaAinda não há avaliações

- Bankruptcy RulesDocumento154 páginasBankruptcy RulesHarpott GhantaAinda não há avaliações

- Hds Standards and PracticesDocumento29 páginasHds Standards and PracticesHarpott GhantaAinda não há avaliações

- (TTC) Geis - Business Statistics IIDocumento23 páginas(TTC) Geis - Business Statistics IIminh_neuAinda não há avaliações

- G2 - List of Videos On AdvocacyDocumento1 páginaG2 - List of Videos On AdvocacyHarpott GhantaAinda não há avaliações

- Rules of CourtDocumento574 páginasRules of CourtHarpott GhantaAinda não há avaliações

- Handwritingsample4 6 09Documento1 páginaHandwritingsample4 6 09Harpott GhantaAinda não há avaliações

- Ny All LocationsDocumento1 páginaNy All LocationsHarpott GhantaAinda não há avaliações

- StateBarRequest - Feb 2015 & July 2015Documento1 páginaStateBarRequest - Feb 2015 & July 2015Harpott GhantaAinda não há avaliações

- Act of Congress Establishing The Treasury DepartmentDocumento1 páginaAct of Congress Establishing The Treasury DepartmentHarpott GhantaAinda não há avaliações

- The Ultimate Bar Exam Preparation Resource GuideDocumento18 páginasThe Ultimate Bar Exam Preparation Resource GuidejohnkyleAinda não há avaliações

- Requirements to Practice Law in California for Foreign Educated Students (39 charactersDocumento4 páginasRequirements to Practice Law in California for Foreign Educated Students (39 charactersCarlo Vincent BalicasAinda não há avaliações

- Ny All LocationsDocumento1 páginaNy All LocationsHarpott GhantaAinda não há avaliações

- Bar Exams ScheduleDocumento3 páginasBar Exams ScheduleHarpott GhantaAinda não há avaliações

- NYS Bar Exam Online Application InstructionsDocumento4 páginasNYS Bar Exam Online Application InstructionsHarpott GhantaAinda não há avaliações

- Central Bank CollateralDocumento14 páginasCentral Bank CollateralHarpott GhantaAinda não há avaliações

- WTO Regulation of Subsidies To State-Owned Enterprises (SOEs) SSRN-id939435Documento47 páginasWTO Regulation of Subsidies To State-Owned Enterprises (SOEs) SSRN-id939435Harpott GhantaAinda não há avaliações

- Andenas On European Company LawDocumento74 páginasAndenas On European Company LawHarpott GhantaAinda não há avaliações

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- Credit Rating Agencies (1 FinalDocumento88 páginasCredit Rating Agencies (1 FinalAvtaar SinghAinda não há avaliações

- SMART BETA ETF PRESENTATIONDocumento12 páginasSMART BETA ETF PRESENTATIONRahul ChaudharyAinda não há avaliações

- IFMP Mutual Fund Distributors Certification (Study and Reference Guide) PDFDocumento165 páginasIFMP Mutual Fund Distributors Certification (Study and Reference Guide) PDFPunjabi Larka100% (1)

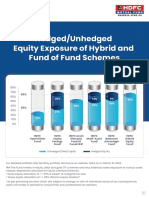

- Leaflet - Hedged and Unhedged Exposure of Hybrid FundsDocumento2 páginasLeaflet - Hedged and Unhedged Exposure of Hybrid FundsDeepakAinda não há avaliações

- Edelweiss Weekly Newsletter October 15 2021Documento2 páginasEdelweiss Weekly Newsletter October 15 2021AdityaAinda não há avaliações

- Literatur ReviewDocumento41 páginasLiteratur ReviewDevendraSarafAinda não há avaliações

- "Risk On - Risk Off" - How A Paradigm Is BornDocumento19 páginas"Risk On - Risk Off" - How A Paradigm Is BorntniravAinda não há avaliações

- Lighthouse Precious Metals Report - 2014 - AugustDocumento40 páginasLighthouse Precious Metals Report - 2014 - AugustAlexander GloyAinda não há avaliações

- Corporate Financing Decisions and Efficient Capital MarketsDocumento53 páginasCorporate Financing Decisions and Efficient Capital MarketsalexanderAinda não há avaliações

- Nondisclosure Agreement for Potential InvestorsDocumento3 páginasNondisclosure Agreement for Potential InvestorsAnthony K. HenryAinda não há avaliações

- Credit Rating Impact On Stock Prices - A Study For IndiaDocumento11 páginasCredit Rating Impact On Stock Prices - A Study For Indiaved2903_iitkAinda não há avaliações

- Market Technician No 73Documento12 páginasMarket Technician No 73ZhichaoWang100% (1)

- An Institutional Theory of Momentum and Revealsal Rev. Financ. Stud.-2013-Vayanos-1087-145Documento59 páginasAn Institutional Theory of Momentum and Revealsal Rev. Financ. Stud.-2013-Vayanos-1087-145IGift WattanatornAinda não há avaliações

- Share Khan LimitedDocumento96 páginasShare Khan LimitedMayur PrajapatiAinda não há avaliações

- HW Assignment Week 8 Student ID 1567033Documento2 páginasHW Assignment Week 8 Student ID 1567033Lưu Gia BảoAinda não há avaliações

- Professional Stock Market Training Course by Shakti Shiromani ShuklaDocumento12 páginasProfessional Stock Market Training Course by Shakti Shiromani ShuklaShakti ShuklaAinda não há avaliações

- Chap011 Exam3Documento78 páginasChap011 Exam3Huyen Vo100% (2)

- Answer: B: Cf-Multiple Choice Questions (1) - Thuhien-UehDocumento5 páginasAnswer: B: Cf-Multiple Choice Questions (1) - Thuhien-UehMinh Phạm100% (1)

- Mutual Fund Analysis ComparisonDocumento76 páginasMutual Fund Analysis ComparisonsantoshbansodeAinda não há avaliações

- Business Analysis ReportDocumento13 páginasBusiness Analysis Reporthassan_401651634Ainda não há avaliações

- Index Funds GuideDocumento17 páginasIndex Funds GuidesambhavjoshiAinda não há avaliações

- Godwin EstateDocumento32 páginasGodwin EstateEnamudu Hope TopeAinda não há avaliações

- MBA VocabularyDocumento41 páginasMBA VocabularyadjerourouAinda não há avaliações

- IIFL Multicap PMS TermsheetDocumento4 páginasIIFL Multicap PMS TermsheetRanjithAinda não há avaliações

- Explain The Sources of Funding For A Start-UpDocumento6 páginasExplain The Sources of Funding For A Start-UpChandra KeerthiAinda não há avaliações

- SPCapitalIQEquityResearch ConchoResourcesInc Feb 28 2016Documento11 páginasSPCapitalIQEquityResearch ConchoResourcesInc Feb 28 2016VeryclearwaterAinda não há avaliações

- Partners Group - FoF BenefitsDocumento8 páginasPartners Group - FoF BenefitsJose M Terrés-NícoliAinda não há avaliações

- What Is A Mutual Fund?Documento35 páginasWhat Is A Mutual Fund?Azaan KhanAinda não há avaliações

- Scenario of Indian Stock MarketDocumento12 páginasScenario of Indian Stock Marketnayak_ramesh330Ainda não há avaliações

- MCB-AH Corp Presentation Sept 12 PDFDocumento30 páginasMCB-AH Corp Presentation Sept 12 PDFlordraiAinda não há avaliações