Você também pode gostar

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5795)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1091)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Exercise-5 - Genta Yusuf Madhani - 1201174352 PDFDocumento17 páginasExercise-5 - Genta Yusuf Madhani - 1201174352 PDFGentaYusufMadhaniAinda não há avaliações

- Case Solutions For Case Studies in Finance Managing For Corporate Value Creation 6th Edition by BrunerDocumento12 páginasCase Solutions For Case Studies in Finance Managing For Corporate Value Creation 6th Edition by BrunerGregory Wilson50% (2)

- Audit 2 - Concept Map For InvestmentsDocumento4 páginasAudit 2 - Concept Map For InvestmentsPrecious Recede100% (1)

- Manual of Engineering Economy PDFDocumento114 páginasManual of Engineering Economy PDFSanjay Kumar SahAinda não há avaliações

- The Audit of LiabilitiesDocumento3 páginasThe Audit of LiabilitiesIftekhar Ifte100% (3)

- Petitioner Respondents: MAYBANK PHILIPPINES, INC. (Formerly PNB-Republic Bank), Spouses Oscar and Nenita TarrosaDocumento6 páginasPetitioner Respondents: MAYBANK PHILIPPINES, INC. (Formerly PNB-Republic Bank), Spouses Oscar and Nenita TarrosaKim Jan Navata BatecanAinda não há avaliações

- A Project Report On Customer Perception and Attitude Towards ICICI Prudential Life InsuranceDocumento85 páginasA Project Report On Customer Perception and Attitude Towards ICICI Prudential Life InsuranceBabasab Patil (Karrisatte)100% (1)

- Time Table For Term VDocumento2 páginasTime Table For Term VGregory WilsonAinda não há avaliações

- 23 Things That They Don't Tell YouDocumento8 páginas23 Things That They Don't Tell YouGregory WilsonAinda não há avaliações

- Group 3 Section B HRMDocumento5 páginasGroup 3 Section B HRMGregory WilsonAinda não há avaliações

- MonopolyDocumento21 páginasMonopolyDhaval ShahAinda não há avaliações

- Innovating For Shared ValueDocumento16 páginasInnovating For Shared ValueGregory WilsonAinda não há avaliações

- NikhilDocumento2 páginasNikhilGregory WilsonAinda não há avaliações

- Kelsey Manufacturing CompanyDocumento7 páginasKelsey Manufacturing CompanyGregory WilsonAinda não há avaliações

- T4 PGPM 2013-15Documento2 páginasT4 PGPM 2013-15Gregory WilsonAinda não há avaliações

- CH 11Documento51 páginasCH 11Gregory WilsonAinda não há avaliações

- Basant Rakesh: Educational QualificationsDocumento13 páginasBasant Rakesh: Educational QualificationsVishalNagarkotiAinda não há avaliações

- Foreign Currency Term LoanDocumento11 páginasForeign Currency Term LoanGunner WengerAinda não há avaliações

- Transaction Review RKPL, Draft ReportDocumento13 páginasTransaction Review RKPL, Draft ReportJoni alauddinAinda não há avaliações

- AAVE (EthLend) WhitepaperDocumento56 páginasAAVE (EthLend) WhitepaperSwitchainAinda não há avaliações

- Q1FY23 - Result Update: Future Growth IntactDocumento10 páginasQ1FY23 - Result Update: Future Growth IntactResearch ReportsAinda não há avaliações

- Final PPT Adr-GdrDocumento71 páginasFinal PPT Adr-Gdr24_anuAinda não há avaliações

- ATS FormatDocumento2 páginasATS FormatZeny BernalAinda não há avaliações

- Relaxo Footwears Initiating Coverage 11062020Documento7 páginasRelaxo Footwears Initiating Coverage 11062020Vaishali AgrawalAinda não há avaliações

- Merrill Lynch Case Study - PrajDocumento19 páginasMerrill Lynch Case Study - PrajAmit Shrivastava100% (3)

- 14th Finance Commission - Report Summary PDFDocumento1 página14th Finance Commission - Report Summary PDFSourav MeenaAinda não há avaliações

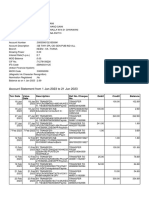

- Account Statement From 1 Jan 2023 To 21 Jun 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento6 páginasAccount Statement From 1 Jan 2023 To 21 Jun 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceKumar SunilAinda não há avaliações

- CAMPERDOWN HIGH SCHOOL - Accounting Grade 9 TestDocumento6 páginasCAMPERDOWN HIGH SCHOOL - Accounting Grade 9 TestLatoya SmithAinda não há avaliações

- H01. Conceptual Framework and Financial StatementsDocumento14 páginasH01. Conceptual Framework and Financial StatementsMaryrose SumulongAinda não há avaliações

- Taxi Proposal Form K5334Documento6 páginasTaxi Proposal Form K5334DorcasAinda não há avaliações

- Bumiputra Malaysia Finance Scandal: This Study Resource Was Shared ViaDocumento6 páginasBumiputra Malaysia Finance Scandal: This Study Resource Was Shared ViaRahimah NuryatiAinda não há avaliações

- K Kiran Kumar: Any Questions? Behavioral Finance, Netscape IPO, ReviewDocumento33 páginasK Kiran Kumar: Any Questions? Behavioral Finance, Netscape IPO, ReviewJohn DoeAinda não há avaliações

- Q. 4 There Are Three Different Phases in The History of Banking in India.Documento4 páginasQ. 4 There Are Three Different Phases in The History of Banking in India.MAHENDRA SHIVAJI DHENAKAinda não há avaliações

- Agribusiness SyllabiDocumento6 páginasAgribusiness SyllabiMerlyn HefervezAinda não há avaliações

- Luxembourg Fiduciary StructuresDocumento12 páginasLuxembourg Fiduciary StructuresDayana VelizAinda não há avaliações

- Ri Kon 6689Documento2 páginasRi Kon 6689Chetan VaishnavAinda não há avaliações

- Advanced Financial Accounting IDocumento21 páginasAdvanced Financial Accounting IAbdiAinda não há avaliações

- Partnership Deed EngDocumento3 páginasPartnership Deed EngShajana ShahulAinda não há avaliações

- Study of Organisational Structure Syndicate BankDocumento48 páginasStudy of Organisational Structure Syndicate BankJissy Shravan50% (2)