Você também pode gostar

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (120)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Charles LeBeau - Exit Strategies For Stock and FuturesDocumento42 páginasCharles LeBeau - Exit Strategies For Stock and Futuresbeli_oblak_1100% (1)

- Loans ReceivableDocumento22 páginasLoans ReceivableJendall SisonAinda não há avaliações

- Customer Lifetime Value ModelsDocumento50 páginasCustomer Lifetime Value Modelspraveen_bpgcAinda não há avaliações

- Free Trade ZoneDocumento3 páginasFree Trade ZonemanoramanAinda não há avaliações

- Warren E. Buffett, 2005: Case Studies in FinanceDocumento2 páginasWarren E. Buffett, 2005: Case Studies in FinanceNakonoaAinda não há avaliações

- Harvey - On Planning The Ideology of PlanningDocumento20 páginasHarvey - On Planning The Ideology of PlanningMacarena Paz Cares VerdugoAinda não há avaliações

- What Is in Coca-Cola?: A Briefing On Our IngredientsDocumento17 páginasWhat Is in Coca-Cola?: A Briefing On Our IngredientsMario Brown100% (1)

- Crisis Management in Belgium: The Case of Coca-ColaDocumento5 páginasCrisis Management in Belgium: The Case of Coca-ColaCham ChoumAinda não há avaliações

- BooksDocumento3 páginasBooksMario BrownAinda não há avaliações

- Customer ProfitabilityDocumento11 páginasCustomer ProfitabilityVaibhav Bindroo0% (1)

- Customer Profitability AnalysisDocumento36 páginasCustomer Profitability AnalysisMichalaki Xrisoula100% (1)

- Pankaj Review of Welding ProcessDocumento9 páginasPankaj Review of Welding ProcessMario BrownAinda não há avaliações

- Customer ProfitabilityDocumento11 páginasCustomer ProfitabilityVaibhav Bindroo0% (1)

- AMIT (2 Files Merged)Documento2 páginasAMIT (2 Files Merged)Mario BrownAinda não há avaliações

- HPLC Solutions #28: Back-to-Basics #1: Retention Factor: John DolanDocumento1 páginaHPLC Solutions #28: Back-to-Basics #1: Retention Factor: John DolanMario BrownAinda não há avaliações

- PM Mid TermDocumento5 páginasPM Mid TermMario BrownAinda não há avaliações

- High-Performance Liquid ChromatographyDocumento9 páginasHigh-Performance Liquid ChromatographyMario BrownAinda não há avaliações

- HPLC Solutions #28: Back-to-Basics #1: Retention Factor: John DolanDocumento1 páginaHPLC Solutions #28: Back-to-Basics #1: Retention Factor: John DolanMario BrownAinda não há avaliações

- GRI Report: A Companion To The 2011/2012 Sustainability ReportDocumento122 páginasGRI Report: A Companion To The 2011/2012 Sustainability ReportMihaela RoscaAinda não há avaliações

- Syllabus Vi SemregehDocumento8 páginasSyllabus Vi SemregehMario BrownAinda não há avaliações

- Definition - What Does Void Volume Mean?Documento8 páginasDefinition - What Does Void Volume Mean?Mario BrownAinda não há avaliações

- Caste SystemDocumento7 páginasCaste SystemMario BrownAinda não há avaliações

- Definition - What Does Void Volume Mean?Documento8 páginasDefinition - What Does Void Volume Mean?Mario BrownAinda não há avaliações

- Aditya Ghildiyal: Areer BjectiveDocumento3 páginasAditya Ghildiyal: Areer BjectiveMario BrownAinda não há avaliações

- Martin Ansin Laurent Durieux Matt Taylor Tyler Stout Ken Taylor N.E. Gabz Aaron Horkey Nick VujicicDocumento5 páginasMartin Ansin Laurent Durieux Matt Taylor Tyler Stout Ken Taylor N.E. Gabz Aaron Horkey Nick VujicicMario BrownAinda não há avaliações

- AthletesDocumento1 páginaAthletesMario BrownAinda não há avaliações

- Environment Report 2009Documento46 páginasEnvironment Report 2009prjtrschAinda não há avaliações

- Coca-Cola - The Alternative ReportDocumento16 páginasCoca-Cola - The Alternative ReportHassan Tahir SialAinda não há avaliações

- SIP On IDBI FederalDocumento18 páginasSIP On IDBI FederalMario BrownAinda não há avaliações

- Effectiveness of The Turkish Corporate Governace SystemDocumento18 páginasEffectiveness of The Turkish Corporate Governace SystemMario BrownAinda não há avaliações

- Coca Cola PDFDocumento30 páginasCoca Cola PDFAmit YadavAinda não há avaliações

- Coca Cola NutritionDocumento1 páginaCoca Cola NutritionMario BrownAinda não há avaliações

- Lic 2 PDFDocumento29 páginasLic 2 PDFDipti MaheriyaAinda não há avaliações

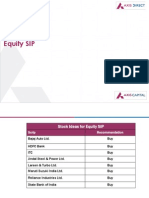

- Equity SIP Stock Ideas of MarutiDocumento11 páginasEquity SIP Stock Ideas of MarutiMario BrownAinda não há avaliações

- Supply Side PoliciesDocumento5 páginasSupply Side PoliciesVanessa KuaAinda não há avaliações

- Display PDFDocumento22 páginasDisplay PDFMurugan AnathanAinda não há avaliações

- Toronto Star Cannabis Report Aug 25 2018Documento8 páginasToronto Star Cannabis Report Aug 25 2018Anonymous i8Pf14Ainda não há avaliações

- PD 1034 - Offshore BankingDocumento5 páginasPD 1034 - Offshore BankingSZAinda não há avaliações

- Arbitrage Pricing TheoryDocumento16 páginasArbitrage Pricing Theorya_karimAinda não há avaliações

- Accounting Standard 11Documento10 páginasAccounting Standard 11api-3828505100% (1)

- Holding CoDocumento35 páginasHolding Coshilpi raniAinda não há avaliações

- Government of India/Bharat Sarkar Ministry of Railways/Rail Mantralaya (Railway Board)Documento9 páginasGovernment of India/Bharat Sarkar Ministry of Railways/Rail Mantralaya (Railway Board)jitendra singhAinda não há avaliações

- Microfinance Report in MaharashtraDocumento96 páginasMicrofinance Report in MaharashtraJugal Taneja100% (1)

- Economic Policies of Ayyub Khan (1958-1968)Documento19 páginasEconomic Policies of Ayyub Khan (1958-1968)Balaj ShaheenAinda não há avaliações

- Fundamentals of Corporate Finance 7th Edition Brealey Test BankDocumento54 páginasFundamentals of Corporate Finance 7th Edition Brealey Test BankEmilyJohnsonfnpgb100% (13)

- Debt InstrumentsDocumento204 páginasDebt InstrumentsSitaKumariAinda não há avaliações

- The Anatomy of A Transaction 020311Documento1 páginaThe Anatomy of A Transaction 020311ealpeshpatelAinda não há avaliações

- Invoice: Orange Bio Science Products Private Limited Bill ToDocumento1 páginaInvoice: Orange Bio Science Products Private Limited Bill ToTanmoy Sarkar GhoshAinda não há avaliações

- Create Scan Old Candlestick P&F Realtime & Alerts WatchlistsDocumento5 páginasCreate Scan Old Candlestick P&F Realtime & Alerts WatchlistsSushobhan DasAinda não há avaliações

- Why Marc Faber Is Such A BearDocumento6 páginasWhy Marc Faber Is Such A BearrobintanwhAinda não há avaliações

- Duplichecker Plagiarism ReportDocumento2 páginasDuplichecker Plagiarism ReportErika DeboraAinda não há avaliações

- MollyDocumento18 páginasMollyYS FongAinda não há avaliações

- Financial Accounting Thesis TopicsDocumento5 páginasFinancial Accounting Thesis TopicsNaomi Hansen100% (2)

- Affidavit (Property Settlement)Documento3 páginasAffidavit (Property Settlement)Jan Kenrick SagumAinda não há avaliações

- Mega Lifesciences Mega TB: Growing in ASEANDocumento12 páginasMega Lifesciences Mega TB: Growing in ASEANAshokAinda não há avaliações

- Primaco Internship ReportDocumento55 páginasPrimaco Internship ReportarmamnmwtAinda não há avaliações

- S4HANA 1909 Preliminary Highlights OverviewDocumento60 páginasS4HANA 1909 Preliminary Highlights OverviewAjersh Paturu100% (6)

- Calendar of The Ancient Records of Dublin Volume XI 1761 - 1768Documento608 páginasCalendar of The Ancient Records of Dublin Volume XI 1761 - 1768Geordie WinkleAinda não há avaliações

- 2 Nit04Documento139 páginas2 Nit04executive engineerAinda não há avaliações