Você também pode gostar

- G.R. No. 148163 - Banco Filipino Savings and Mortgage Bank v. YbañezDocumento6 páginasG.R. No. 148163 - Banco Filipino Savings and Mortgage Bank v. YbañezlckdsclAinda não há avaliações

- Bacolor vs. Banco Filipino Saving and Mortgage BankDocumento1 páginaBacolor vs. Banco Filipino Saving and Mortgage BankMarianne AndresAinda não há avaliações

- Bacolor Banking Bank in DistressDocumento3 páginasBacolor Banking Bank in DistressJai Rel RadlynAinda não há avaliações

- Barredo Vs GarciaDocumento2 páginasBarredo Vs GarciaDan Anthony BarrigaAinda não há avaliações

- University of The East v. JaderDocumento1 páginaUniversity of The East v. JaderShari Realce AndeAinda não há avaliações

- Jarco Marketing v. CAdocxDocumento2 páginasJarco Marketing v. CAdocxTerence Mark Arthur FerrerAinda não há avaliações

- Santos v. PizardoDocumento5 páginasSantos v. PizardoPVallAinda não há avaliações

- Floreindo v. MetrobankDocumento1 páginaFloreindo v. MetrobankSarah Jane UsopAinda não há avaliações

- People vs. Suedad (Case Digest)Documento2 páginasPeople vs. Suedad (Case Digest)FbarrsAinda não há avaliações

- Amadora vs. CADocumento1 páginaAmadora vs. CAVanya Klarika NuqueAinda não há avaliações

- Case Digest - Ruks Konsult Construction Vs Adworld Sign and Advertising CorpDocumento2 páginasCase Digest - Ruks Konsult Construction Vs Adworld Sign and Advertising CorpMaricris GalingganaAinda não há avaliações

- P.L. Uy Realty Corporation vs. Als Management & DevelopmentDocumento3 páginasP.L. Uy Realty Corporation vs. Als Management & Developmentmiles1280100% (2)

- Napocor Vs PhibroDocumento2 páginasNapocor Vs PhibroTogz MapeAinda não há avaliações

- #38. Allan Vs PNBDocumento37 páginas#38. Allan Vs PNBeizAinda não há avaliações

- 12 Gutierrez-v-GutierrezDocumento1 página12 Gutierrez-v-GutierrezluigimanzanaresAinda não há avaliações

- Vicarious LiabilityDocumento11 páginasVicarious LiabilityNeil Sandrei BayanganAinda não há avaliações

- Spouses Batal vs. Spouses San PedroDocumento12 páginasSpouses Batal vs. Spouses San PedroShela L LobasAinda não há avaliações

- Amador Vs CA, Et - Al., GR No. L-47745, April 15, 1988 DoctrineDocumento4 páginasAmador Vs CA, Et - Al., GR No. L-47745, April 15, 1988 DoctrineBleizel TeodosioAinda não há avaliações

- Rakes vs. AGPDocumento20 páginasRakes vs. AGPJesha GCAinda não há avaliações

- AdminLaw - Guevarra v. Commission On Elections, G.R. No. 12596Documento3 páginasAdminLaw - Guevarra v. Commission On Elections, G.R. No. 12596Lei BlancoAinda não há avaliações

- Tankeh vs. Development Bank of The PhilippinesDocumento2 páginasTankeh vs. Development Bank of The PhilippinesHyacinth Salig-BathanAinda não há avaliações

- Batarra V MarcosDocumento1 páginaBatarra V MarcosBGodAinda não há avaliações

- Allen MC Conn Vs Paul Haragan Et Al.Documento2 páginasAllen MC Conn Vs Paul Haragan Et Al.Jillian AsdalaAinda não há avaliações

- Rakes Vs AtlanticDocumento2 páginasRakes Vs AtlanticJames Evan I. ObnamiaAinda não há avaliações

- Wright V Manila Electric RR & Light CoDocumento2 páginasWright V Manila Electric RR & Light CoJaz SumalinogAinda não há avaliações

- Yobido Vs CADocumento2 páginasYobido Vs CAAiWeiAinda não há avaliações

- Mariveles Vs CA 415Documento15 páginasMariveles Vs CA 415Joel G. AyonAinda não há avaliações

- Andamo vs. Intermediate Appellate Court, 191 SCRA 195, November 06, 1990Documento1 páginaAndamo vs. Intermediate Appellate Court, 191 SCRA 195, November 06, 1990Rizchelle Sampang-ManaogAinda não há avaliações

- 119 - Manila Railroad Co v. La CompaniaDocumento2 páginas119 - Manila Railroad Co v. La CompaniajrvyeeAinda não há avaliações

- Estores Vs Spouses SupanganDocumento3 páginasEstores Vs Spouses SupanganAnne MiguelAinda não há avaliações

- 17 Chiongvian-V - OrbosDocumento2 páginas17 Chiongvian-V - OrbosLuna BaciAinda não há avaliações

- Marites - Cases Credit DigestedDocumento58 páginasMarites - Cases Credit DigestedMaritesCatayongAinda não há avaliações

- Stronghold Insurance Company vs. Republic - Asahi Glass Corp.Documento1 páginaStronghold Insurance Company vs. Republic - Asahi Glass Corp.Juan Carlos Brillantes100% (1)

- Republic V Luzon StevedoringDocumento1 páginaRepublic V Luzon StevedoringSuiAinda não há avaliações

- N-10-01 Jimenez v. BucoyDocumento1 páginaN-10-01 Jimenez v. Bucoy刘王钟Ainda não há avaliações

- Loadmasters Customs Services, Inc. v. Glodel Brokerage Corporation, G.R. No. 179446, 10 January 2011, (639 SCRA 69)Documento3 páginasLoadmasters Customs Services, Inc. v. Glodel Brokerage Corporation, G.R. No. 179446, 10 January 2011, (639 SCRA 69)Christian Talisay100% (1)

- Rural Bank of San Miguel vs. MB DigestDocumento1 páginaRural Bank of San Miguel vs. MB DigestMae NavarraAinda não há avaliações

- CIR V SM PRIMEDocumento2 páginasCIR V SM PRIMEPopeye100% (1)

- Victory Liner Vs Heirs of Malecdan Case DigestDocumento1 páginaVictory Liner Vs Heirs of Malecdan Case DigestSheena JuarezAinda não há avaliações

- Case Digest Asset Builders Vs StrongholdDocumento2 páginasCase Digest Asset Builders Vs StrongholdMirai Kuriyama0% (1)

- Banco de Oro vs. Bayuga, 93 SCRA 443Documento18 páginasBanco de Oro vs. Bayuga, 93 SCRA 443Jillian Batac100% (1)

- CANON7 9 AdditionalDocumento11 páginasCANON7 9 AdditionalJustine M.Ainda não há avaliações

- R Transport Corporation v. Luisito G. YuDocumento3 páginasR Transport Corporation v. Luisito G. YuJoshua MaulaAinda não há avaliações

- Fuellas Vs CadanoDocumento4 páginasFuellas Vs CadanoMutyaAlmodienteCocjinAinda não há avaliações

- Philippine Hawk V LeeDocumento2 páginasPhilippine Hawk V LeeJanine IsmaelAinda não há avaliações

- Metro Manila Transit Corp v. CADocumento3 páginasMetro Manila Transit Corp v. CAEva TrinidadAinda não há avaliações

- Tanpingco vs. IAC (1992)Documento5 páginasTanpingco vs. IAC (1992)Madelinia100% (1)

- Metrobank vs. CADocumento2 páginasMetrobank vs. CADongkaeAinda não há avaliações

- CPG - 1. Metrobank Et Al Vs TanDocumento6 páginasCPG - 1. Metrobank Et Al Vs TanImma OlayanAinda não há avaliações

- Manliclic V CalaunanDocumento2 páginasManliclic V CalaunanMillicent MatienzoAinda não há avaliações

- Metro Concast v. Allied Banking - Case DigestDocumento2 páginasMetro Concast v. Allied Banking - Case DigestLulu RodriguezAinda não há avaliações

- St. Francis High School vs. Court of AppealsDocumento3 páginasSt. Francis High School vs. Court of AppealsMandaluyong RtcAinda não há avaliações

- (People vs. Ligon, 152 SCRA 419 (1987) ) PDFDocumento13 páginas(People vs. Ligon, 152 SCRA 419 (1987) ) PDFJillian BatacAinda não há avaliações

- Petitioner vs. vs. Respondents: First DivisionDocumento12 páginasPetitioner vs. vs. Respondents: First DivisionGael MoralesAinda não há avaliações

- Carino v. CHR (Digest)Documento2 páginasCarino v. CHR (Digest)Homer SimpsonAinda não há avaliações

- Durban Apartments v. Pioneer InsuranceDocumento2 páginasDurban Apartments v. Pioneer InsuranceNivra Lyn EmpialesAinda não há avaliações

- DIGESTDocumento7 páginasDIGESTSometimes goodAinda não há avaliações

- Pelayo vs. Lauron 12 Phil. 453Documento1 páginaPelayo vs. Lauron 12 Phil. 453Lu CasAinda não há avaliações

- Case Digests For Banking LawsDocumento22 páginasCase Digests For Banking LawsJanine CastroAinda não há avaliações

- Banco Filipino Vs YbanezDocumento3 páginasBanco Filipino Vs YbanezAllen Jeil GeronaAinda não há avaliações

- FIN226 Summer 2011 Lectures CH 6 SlidesDocumento20 páginasFIN226 Summer 2011 Lectures CH 6 SlidesBasit F.Ainda não há avaliações

- Sici PDFDocumento12 páginasSici PDFaathavan1991Ainda não há avaliações

- Business Math Reviewer ShortDocumento12 páginasBusiness Math Reviewer ShortJames Earl AbainzaAinda não há avaliações

- Swot AnalysisDocumento21 páginasSwot AnalysisEvan SenAinda não há avaliações

- Account Opening Form DLM KYCDocumento4 páginasAccount Opening Form DLM KYCAnthonyAinda não há avaliações

- Zakat Declaration Form CZ501Documento1 páginaZakat Declaration Form CZ501Zahid BashirAinda não há avaliações

- Guillermo Napoleon Lopez Petition For Emergency SuspensionDocumento53 páginasGuillermo Napoleon Lopez Petition For Emergency SuspensionThe Straw BuyerAinda não há avaliações

- SMC R&P FY 2022-Final FormatsDocumento3 páginasSMC R&P FY 2022-Final Formatsacge nrptAinda não há avaliações

- Case Study R. Thyagarajan PDFDocumento65 páginasCase Study R. Thyagarajan PDFAnkit JainAinda não há avaliações

- CH 7 SourcesDocumento6 páginasCH 7 Sourcesmanoj kashyapAinda não há avaliações

- Syla F552Documento7 páginasSyla F552Aiman Maimunatullail RahimiAinda não há avaliações

- Banking Law MCQDocumento33 páginasBanking Law MCQShivansh Bansal100% (7)

- British Gas Acquisition Verbal Script 06-01-2014Documento3 páginasBritish Gas Acquisition Verbal Script 06-01-2014asdasdsadAinda não há avaliações

- Annual Report 2010 2011 PDFDocumento31 páginasAnnual Report 2010 2011 PDFbekele abomsaAinda não há avaliações

- Comparative Analysis of Two Small Finance BanksDocumento19 páginasComparative Analysis of Two Small Finance BanksSneha SharmaAinda não há avaliações

- A Study On Barriers To E-Commerce Adoption in Vadodara District SMEsDocumento15 páginasA Study On Barriers To E-Commerce Adoption in Vadodara District SMEsKushagra purohitAinda não há avaliações

- Complete List of Indian Banks and Their Heads - CMDs - CEOs - Gr8AmbitionZ PDFDocumento8 páginasComplete List of Indian Banks and Their Heads - CMDs - CEOs - Gr8AmbitionZ PDFNageswara ReddyAinda não há avaliações

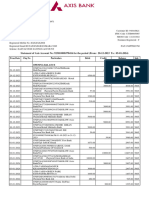

- Account STMTDocumento2 páginasAccount STMTnazim.civilengrAinda não há avaliações

- 1.1: Accounting Conventions and Standards ObjectivesDocumento6 páginas1.1: Accounting Conventions and Standards ObjectivesbijuAinda não há avaliações

- BPI Employees Union Vs Bank of The Philippine IslandDocumento6 páginasBPI Employees Union Vs Bank of The Philippine IslandAllen OlayvarAinda não há avaliações

- Diploma in Investment AnalysisDocumento4 páginasDiploma in Investment AnalysisyanauitmAinda não há avaliações

- CIS Client Information SheetDocumento4 páginasCIS Client Information SheetVíctor Palacios Romero75% (4)

- Union Bank vs. Sps Tiu DigestDocumento3 páginasUnion Bank vs. Sps Tiu DigestCaitlin KintanarAinda não há avaliações

- Centrum Wealth Ratnamani Metals - Initiating CoverageDocumento11 páginasCentrum Wealth Ratnamani Metals - Initiating Coveragenarayanan_rAinda não há avaliações

- General Electric Case StudyDocumento14 páginasGeneral Electric Case StudySherif ElfarAinda não há avaliações

- Banfield Financial Documents 2 - 15 - 2024Documento3 páginasBanfield Financial Documents 2 - 15 - 2024yourphdjAinda não há avaliações

- General Bank and Trust V Central BankDocumento3 páginasGeneral Bank and Trust V Central Bankdino de guzmanAinda não há avaliações

- All Bank CEO List PDFDocumento5 páginasAll Bank CEO List PDFKishanAinda não há avaliações

- FABM2 12 Quarter1 Week7Documento10 páginasFABM2 12 Quarter1 Week7Princess DuquezaAinda não há avaliações

- Project On SebiDocumento15 páginasProject On SebiVrushti Parmar86% (14)

- Getting Through: Cold Calling Techniques To Get Your Foot In The DoorNo EverandGetting Through: Cold Calling Techniques To Get Your Foot In The DoorNota: 4.5 de 5 estrelas4.5/5 (63)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingNo EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingNota: 4.5 de 5 estrelas4.5/5 (97)

- Introduction to Negotiable Instruments: As per Indian LawsNo EverandIntroduction to Negotiable Instruments: As per Indian LawsNota: 5 de 5 estrelas5/5 (1)

- The Startup Visa: U.S. Immigration Visa Guide for Startups and FoundersNo EverandThe Startup Visa: U.S. Immigration Visa Guide for Startups and FoundersAinda não há avaliações

- Buffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorNo EverandBuffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorNota: 4.5 de 5 estrelas4.5/5 (132)

- Public Finance: Legal Aspects: Collective monographNo EverandPublic Finance: Legal Aspects: Collective monographAinda não há avaliações

- How to Win a Merchant Dispute or Fraudulent Chargeback CaseNo EverandHow to Win a Merchant Dispute or Fraudulent Chargeback CaseAinda não há avaliações

- Ben & Jerry's Double-Dip Capitalism: Lead With Your Values and Make Money TooNo EverandBen & Jerry's Double-Dip Capitalism: Lead With Your Values and Make Money TooNota: 5 de 5 estrelas5/5 (2)

- The SHRM Essential Guide to Employment Law, Second Edition: A Handbook for HR Professionals, Managers, Businesses, and OrganizationsNo EverandThe SHRM Essential Guide to Employment Law, Second Edition: A Handbook for HR Professionals, Managers, Businesses, and OrganizationsAinda não há avaliações

- Indian Polity with Indian Constitution & Parliamentary AffairsNo EverandIndian Polity with Indian Constitution & Parliamentary AffairsAinda não há avaliações

- Contract Law in America: A Social and Economic Case StudyNo EverandContract Law in America: A Social and Economic Case StudyAinda não há avaliações

- The Streetwise Guide to Going Broke without Losing your ShirtNo EverandThe Streetwise Guide to Going Broke without Losing your ShirtAinda não há avaliações

- LLC: LLC Quick start guide - A beginner's guide to Limited liability companies, and starting a businessNo EverandLLC: LLC Quick start guide - A beginner's guide to Limited liability companies, and starting a businessNota: 5 de 5 estrelas5/5 (1)

- AI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersNo EverandAI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersAinda não há avaliações

- A Simple Guide for Drafting of Conveyances in India : Forms of Conveyances and Instruments executed in the Indian sub-continent along with Notes and TipsNo EverandA Simple Guide for Drafting of Conveyances in India : Forms of Conveyances and Instruments executed in the Indian sub-continent along with Notes and TipsAinda não há avaliações

- The Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesWhite Collar CriminalsNo EverandThe Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesWhite Collar CriminalsNota: 5 de 5 estrelas5/5 (24)

- The Financial Planning Puzzle: Fitting Your Pieces Together to Create Financial FreedomNo EverandThe Financial Planning Puzzle: Fitting Your Pieces Together to Create Financial FreedomNota: 4.5 de 5 estrelas4.5/5 (2)

- Wall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementNo EverandWall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementNota: 4.5 de 5 estrelas4.5/5 (20)

- Venture Deals: Be Smarter Than Your Lawyer and Venture CapitalistNo EverandVenture Deals: Be Smarter Than Your Lawyer and Venture CapitalistNota: 4 de 5 estrelas4/5 (34)

- The Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesNo EverandThe Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesNota: 5 de 5 estrelas5/5 (1)

- Secrecy World: Inside the Panama Papers Investigation of Illicit Money Networks and the Global EliteNo EverandSecrecy World: Inside the Panama Papers Investigation of Illicit Money Networks and the Global EliteNota: 4.5 de 5 estrelas4.5/5 (6)

- International Business Law: Cases and MaterialsNo EverandInternational Business Law: Cases and MaterialsNota: 5 de 5 estrelas5/5 (1)

- The Complete Book of Wills, Estates & Trusts (4th Edition): Advice That Can Save You Thousands of Dollars in Legal Fees and TaxesNo EverandThe Complete Book of Wills, Estates & Trusts (4th Edition): Advice That Can Save You Thousands of Dollars in Legal Fees and TaxesNota: 4 de 5 estrelas4/5 (1)