Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Formula Sheet For Financial MathematicsDocumento4 páginasFormula Sheet For Financial MathematicsMilon SultanAinda não há avaliações

- Fund Selector EditionDocumento3 páginasFund Selector Editionapi-26324170Ainda não há avaliações

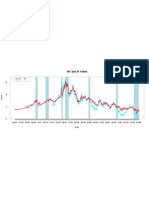

- 10Y and 2Y YieldsDocumento1 página10Y and 2Y Yieldsapi-26324170Ainda não há avaliações

- 10yr 2yrDocumento1 página10yr 2yrapi-26324170Ainda não há avaliações

- Gold and Your PortfolioDocumento7 páginasGold and Your Portfolioapi-26324170Ainda não há avaliações

- Equities and Tobin's QDocumento18 páginasEquities and Tobin's Qapi-26324170Ainda não há avaliações

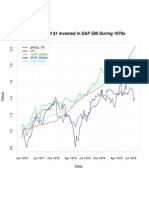

- Growth of $1 Invested in S&P 500 During 1970s: 10YR - BONDDocumento1 páginaGrowth of $1 Invested in S&P 500 During 1970s: 10YR - BONDapi-26324170Ainda não há avaliações

- Nomura EquityResearch The Business of AgeingDocumento136 páginasNomura EquityResearch The Business of Ageingstarbak777Ainda não há avaliações

- Where's The Smoking Gun? A Study of Underwriting Standards For US Subprime MortgagesDocumento38 páginasWhere's The Smoking Gun? A Study of Underwriting Standards For US Subprime Mortgagesapi-26324170Ainda não há avaliações

- Florida Limited Liability Company Operating AgreementDocumento6 páginasFlorida Limited Liability Company Operating AgreementBaseer HaqqieAinda não há avaliações

- Entrepreneurship Development Project - CinemasDocumento92 páginasEntrepreneurship Development Project - CinemaspranjalAinda não há avaliações

- Investment, Security and Portfolio ManagementDocumento396 páginasInvestment, Security and Portfolio ManagementSM FriendAinda não há avaliações

- Pag-IBIG Housing Loan CalculatorDocumento2 páginasPag-IBIG Housing Loan CalculatorkiraAinda não há avaliações

- Valuation of Bonds and SharesDocumento39 páginasValuation of Bonds and Shareskunalacharya5Ainda não há avaliações

- Black Friday: Directions: Read The Following Passage and Answer The Questions That Follow. Refer ToDocumento17 páginasBlack Friday: Directions: Read The Following Passage and Answer The Questions That Follow. Refer ToPutri SekarAinda não há avaliações

- Joint and Solidary Obligation1Documento29 páginasJoint and Solidary Obligation1merryAinda não há avaliações

- Reviewer Business Law Auto Saved)Documento17 páginasReviewer Business Law Auto Saved)Maria MariaAinda não há avaliações

- COMM 229 Notes Chapter 2:3Documento2 páginasCOMM 229 Notes Chapter 2:3Cody ClinkardAinda não há avaliações

- 2019 IFRS Financial Results: Resources Create Opportunities Resources Create OpportunitiesDocumento24 páginas2019 IFRS Financial Results: Resources Create Opportunities Resources Create OpportunitiesVlad KremerAinda não há avaliações

- Understanding The Federal Reserve Balance SheetDocumento4 páginasUnderstanding The Federal Reserve Balance Sheetjimmyboy111Ainda não há avaliações

- Economist A 200417Documento56 páginasEconomist A 200417Ligia Marina PechAinda não há avaliações

- Solution File: Intergenerational IngenuityDocumento4 páginasSolution File: Intergenerational IngenuitykyliefosterAinda não há avaliações

- TB Bank loans-đã chuyển sang wordDocumento8 páginasTB Bank loans-đã chuyển sang wordVi TrươngAinda não há avaliações

- CH 14Documento8 páginasCH 14Lemon VeinAinda não há avaliações

- GCR Nims Amicus BriefDocumento148 páginasGCR Nims Amicus BriefRussinator100% (1)

- Draft FS Tax Purpose 01.03.2018Documento25 páginasDraft FS Tax Purpose 01.03.2018Engineering EntertainmentAinda não há avaliações

- Confusion or Merger of Rights (Arts. 1275 - 1277)Documento2 páginasConfusion or Merger of Rights (Arts. 1275 - 1277)Nailiah MacakilingAinda não há avaliações

- Financial Statement Analysis With Ratio Analysis On: Glenmark Pharmaceutical LimitedDocumento41 páginasFinancial Statement Analysis With Ratio Analysis On: Glenmark Pharmaceutical LimitedGovindraj PrabhuAinda não há avaliações

- Debtor Reply Affirmation To Aust Gregory Zipes FiledDocumento87 páginasDebtor Reply Affirmation To Aust Gregory Zipes FiledRahul ManchandaAinda não há avaliações

- 087 BPI v. CA CompensationDocumento2 páginas087 BPI v. CA CompensationCarl AngeloAinda não há avaliações

- Mora Solvendi (Delay of The Debtor)Documento11 páginasMora Solvendi (Delay of The Debtor)John Paul100% (1)

- Home Afrika Limited V Ecobank Kenya Limited (Insol 230321 082056Documento17 páginasHome Afrika Limited V Ecobank Kenya Limited (Insol 230321 082056Malcolm 'Doctore' LeeAinda não há avaliações

- Acca Afm (P4)Documento36 páginasAcca Afm (P4)SamanMurtazaAinda não há avaliações

- Quiz #3.2-Time Value of Money-SolutionsDocumento2 páginasQuiz #3.2-Time Value of Money-SolutionsChrisAinda não há avaliações

- A Credit Rating Evaluates The Credit Worthiness of An Issuer of Specific Types of DebtDocumento17 páginasA Credit Rating Evaluates The Credit Worthiness of An Issuer of Specific Types of Debtlucaciu_ale6517Ainda não há avaliações

- Unit 1 - Indian Financial SystemDocumento31 páginasUnit 1 - Indian Financial SystemPrasad IngoleAinda não há avaliações

- Comparative Analysis of SailDocumento60 páginasComparative Analysis of SailKajal YadavAinda não há avaliações

- Sdo Batangas: Department of EducationDocumento15 páginasSdo Batangas: Department of EducationPrincess GabaynoAinda não há avaliações