Você também pode gostar

- Asset Liability ManagementDocumento2 páginasAsset Liability ManagementPritesh GhoshAinda não há avaliações

- Asset Liability Management in Banks (Alm) : Follow AllbankingsolutionsDocumento6 páginasAsset Liability Management in Banks (Alm) : Follow AllbankingsolutionsSanjeet MohantyAinda não há avaliações

- Manage Bank Balance Sheets & Risks with ALMDocumento4 páginasManage Bank Balance Sheets & Risks with ALMSri vidyaAinda não há avaliações

- Asset Liability ManagementDocumento35 páginasAsset Liability ManagementNiket Dattani100% (1)

- Comprehensive Risk Management SystemDocumento2 páginasComprehensive Risk Management SystemrakhalbanglaAinda não há avaliações

- 3 - FIG09104 Fin. Mark.& InsDocumento49 páginas3 - FIG09104 Fin. Mark.& InsMoud KhalfaniAinda não há avaliações

- Asset Liability ManagementDocumento9 páginasAsset Liability Managementnikitaneha0603Ainda não há avaliações

- MagggggiDocumento24 páginasMagggggiGaniya MeghanaAinda não há avaliações

- Indian Banking Sector Reforms: Asset Liability Management SystemDocumento3 páginasIndian Banking Sector Reforms: Asset Liability Management SystemRAJIV SINGHAinda não há avaliações

- Asset and Liability Management: Presented To Coronation Merchant Bank - Training SchoolDocumento40 páginasAsset and Liability Management: Presented To Coronation Merchant Bank - Training SchoolBlake SheltonAinda não há avaliações

- Asset Liability Management in BanksDocumento8 páginasAsset Liability Management in BankscelesteAinda não há avaliações

- (654180146) 282992783 Asset Liability Management in BanksDocumento50 páginas(654180146) 282992783 Asset Liability Management in BanksAnurag BajajAinda não há avaliações

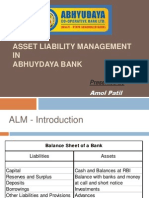

- Asset Liability Management IN Abhuydaya Bank: Amol PatilDocumento14 páginasAsset Liability Management IN Abhuydaya Bank: Amol Patilpari0000Ainda não há avaliações

- Ubi AlmDocumento20 páginasUbi AlmNagendraprasad PuppalaAinda não há avaliações

- Liabilities ManatgementiciciDocumento112 páginasLiabilities ManatgementiciciShaik NabiAinda não há avaliações

- Asset and Liability ManagementDocumento57 páginasAsset and Liability ManagementMayur Federer Kunder100% (2)

- Managing risks through ALMDocumento33 páginasManaging risks through ALMalpeshAinda não há avaliações

- Assets Andliability Management at Icici Bank-1Documento73 páginasAssets Andliability Management at Icici Bank-1akshuAinda não há avaliações

- Risk Management SystemDocumento4 páginasRisk Management SystemRanjith KumarAinda não há avaliações

- KRC Asset and Liability Management Presented to Coronation Merchant BankDocumento26 páginasKRC Asset and Liability Management Presented to Coronation Merchant BankBlake SheltonAinda não há avaliações

- Corporate Governance and Risk Management Framework at BTPN SyariahDocumento8 páginasCorporate Governance and Risk Management Framework at BTPN SyariahAhmad Ihsan RizkindaAinda não há avaliações

- Asset Liability Management of Icici Bank: Presented By: Paul Caroline Poornima Sonal AnvinDocumento47 páginasAsset Liability Management of Icici Bank: Presented By: Paul Caroline Poornima Sonal AnvinsonalsankhlaAinda não há avaliações

- Alm PDFDocumento68 páginasAlm PDFkarthikAinda não há avaliações

- Treasury ManagementDocumento14 páginasTreasury ManagementOmkar RohekarAinda não há avaliações

- Asset Liability Management in BanksDocumento5 páginasAsset Liability Management in BanksPooja GuptaAinda não há avaliações

- Unit 15 Asset Liability Management: ObjectivesDocumento24 páginasUnit 15 Asset Liability Management: ObjectivesSiva Venkata RamanaAinda não há avaliações

- Asset Liability Management IciciDocumento71 páginasAsset Liability Management IciciHaniya Princexx Kousar0% (2)

- CBM IndexDocumento3 páginasCBM IndexcitunairAinda não há avaliações

- Malaysian Banking SystemDocumento2 páginasMalaysian Banking Systemorient4Ainda não há avaliações

- Comprehensive risk management framework for AMMBDocumento41 páginasComprehensive risk management framework for AMMBنورول ازلينا عثمانAinda não há avaliações

- This Report Is On Assets and Liability Management of Different BanksDocumento22 páginasThis Report Is On Assets and Liability Management of Different BanksPratik_Gupta_3369Ainda não há avaliações

- The Measurement and Management of Risks in BanksDocumento21 páginasThe Measurement and Management of Risks in BanksGaurav GehlotAinda não há avaliações

- Asset Liability ManagementDocumento3 páginasAsset Liability ManagementVictorAinda não há avaliações

- Bank VivaDocumento38 páginasBank VivaDebasis NayakAinda não há avaliações

- Asset Liability Management - TMDocumento11 páginasAsset Liability Management - TMPriyanka Srinivasulu ReddyAinda não há avaliações

- Credit Risk ManagementDocumento16 páginasCredit Risk Managementkrishnalohia9Ainda não há avaliações

- Shortnotes On ALM (Asset Liability Management) - Banking Basics For SBI and IBPS Common InterviewsDocumento3 páginasShortnotes On ALM (Asset Liability Management) - Banking Basics For SBI and IBPS Common InterviewsSanjeet MohantyAinda não há avaliações

- A Study On Asset Liability ManagementDocumento56 páginasA Study On Asset Liability ManagementMisraAinda não há avaliações

- Assets Liability ManagementDocumento28 páginasAssets Liability Managementpriyanka choudharyAinda não há avaliações

- Assets Liabilities ManagementDocumento11 páginasAssets Liabilities Managementlove MusicAinda não há avaliações

- Introduction to ALM in BankingDocumento69 páginasIntroduction to ALM in BankingSanthosh Soma75% (4)

- Jinal Asset Liablity ManaDocumento38 páginasJinal Asset Liablity Manajinalpanchal952Ainda não há avaliações

- Devoloping Risk ManagementDocumento13 páginasDevoloping Risk ManagementfaisalAinda não há avaliações

- Asset and Liability ManagementDocumento8 páginasAsset and Liability ManagementPriyanka YadavAinda não há avaliações

- ALM Policy SummaryDocumento9 páginasALM Policy Summarytreddy249Ainda não há avaliações

- Asset-Liability-Management - A Comparative Study of A Public andDocumento10 páginasAsset-Liability-Management - A Comparative Study of A Public andsukanyaAinda não há avaliações

- Asset Liability Management Under Risk FrameworkDocumento9 páginasAsset Liability Management Under Risk FrameworklinnnehAinda não há avaliações

- Asset Liability Management Canara BankDocumento102 páginasAsset Liability Management Canara BankAkash Jadhav0% (1)

- Asset Liability Management of Heritage Cooperative BankDocumento76 páginasAsset Liability Management of Heritage Cooperative Bankarjunmba1196240% (1)

- Garvit AXIS BankDocumento4 páginasGarvit AXIS BankGarvit SinghAinda não há avaliações

- AaaaDocumento12 páginasAaaaAhmad FadhilAinda não há avaliações

- Asset Liability Management: in BanksDocumento44 páginasAsset Liability Management: in Bankssachin21singhAinda não há avaliações

- Finance About City Union BankDocumento65 páginasFinance About City Union Bankarunkmr326Ainda não há avaliações

- Alm Guidelines by RBIDocumento10 páginasAlm Guidelines by RBIPranav ViraAinda não há avaliações

- Principles of Asset and Liability Management: Minimum Correct Answers For This Module: 4/8Documento11 páginasPrinciples of Asset and Liability Management: Minimum Correct Answers For This Module: 4/8Jovan SsenkandwaAinda não há avaliações

- Treasury Management SyllabusDocumento2 páginasTreasury Management SyllabusMiral MaisuriaAinda não há avaliações

- Mastering Financial Risk Management : Strategies for SuccessNo EverandMastering Financial Risk Management : Strategies for SuccessAinda não há avaliações

- Rules of the game dumb charades - game rules clues time limitDocumento3 páginasRules of the game dumb charades - game rules clues time limitAnantha NagAinda não há avaliações

- Star Outlets List Sa3Documento4 páginasStar Outlets List Sa3Anantha NagAinda não há avaliações

- Social Media in The WorkplaceDocumento37 páginasSocial Media in The WorkplaceAnantha Nag100% (1)

- LettersDocumento1 páginaLettersAnantha NagAinda não há avaliações

- Negotations SkillsDocumento18 páginasNegotations SkillsAnantha NagAinda não há avaliações

- Hire PurcahseDocumento9 páginasHire PurcahseAnantha Nag100% (1)

- Strategic ManagementDocumento191 páginasStrategic ManagementAnantha NagAinda não há avaliações

- Check List For PlacementsDocumento1 páginaCheck List For PlacementsAnantha NagAinda não há avaliações

- Sample of A Short Formal ReportDocumento2 páginasSample of A Short Formal ReportAnantha Nag70% (10)

- Business Letter's & Report WritingDocumento77 páginasBusiness Letter's & Report WritingAnantha Nag67% (3)

- Presentation SkillsDocumento17 páginasPresentation SkillsAnantha NagAinda não há avaliações

- CVS, Personal Interviews, and Group DiscussionsDocumento20 páginasCVS, Personal Interviews, and Group DiscussionsAnantha NagAinda não há avaliações

- Idea HamaraDocumento13 páginasIdea HamaraAnantha NagAinda não há avaliações

- Business Planning in Different EnvironmentsDocumento56 páginasBusiness Planning in Different EnvironmentsAnantha Nag67% (3)

- Crafting & Executing Strategy Chapter 1 SummaryDocumento33 páginasCrafting & Executing Strategy Chapter 1 SummaryTruc Tran100% (4)

- 011-Icssh 2012-S00010Documento6 páginas011-Icssh 2012-S00010Asim KhanAinda não há avaliações

- TallyDocumento1 páginaTallyAnantha NagAinda não há avaliações

- Indian Financial System OverviewDocumento171 páginasIndian Financial System OverviewKarthikeyan ElangovanAinda não há avaliações

- What Do You Mean by ANCOVA?: Advantages of SPSSDocumento5 páginasWhat Do You Mean by ANCOVA?: Advantages of SPSSAnantha NagAinda não há avaliações

- Sample Letter of EnquiriesDocumento1 páginaSample Letter of EnquiriesAnantha NagAinda não há avaliações

- What Are Some Inspiring Indian Entrepreneurial Stories - QuoraDocumento29 páginasWhat Are Some Inspiring Indian Entrepreneurial Stories - QuoraAnantha NagAinda não há avaliações

- Business Etiquittes NewDocumento37 páginasBusiness Etiquittes NewAnantha NagAinda não há avaliações

- LettersDocumento1 páginaLettersAnantha NagAinda não há avaliações

- 25 Young Entrepreneur Success Stories - Entrepreneur The ArtsDocumento10 páginas25 Young Entrepreneur Success Stories - Entrepreneur The ArtsAnantha NagAinda não há avaliações

- RegulationDocumento10 páginasRegulationRees JohnsonAinda não há avaliações

- Bharathiar University MPhil/PhD Management SyllabusDocumento22 páginasBharathiar University MPhil/PhD Management SyllabusRisker RaviAinda não há avaliações

- Business Communication BookDocumento180 páginasBusiness Communication BookVinay KeshriAinda não há avaliações

- Conflict ModuleDocumento14 páginasConflict ModuleAnantha NagAinda não há avaliações

- ALM-Asset & Liability Management: The ALM Process Rests On Three Pillars: I. ALM Information SystemsDocumento1 páginaALM-Asset & Liability Management: The ALM Process Rests On Three Pillars: I. ALM Information SystemsAnantha NagAinda não há avaliações

- Mba-IV-International Marketing Management (12mbamm418) - Question PaperDocumento4 páginasMba-IV-International Marketing Management (12mbamm418) - Question PaperAnantha NagAinda não há avaliações