Você também pode gostar

- Ald CHR 683eDocumento1 páginaAld CHR 683ePRADEE2UAinda não há avaliações

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Investment by True NorthDocumento1 páginaInvestment by True NorthPRADEE2UAinda não há avaliações

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- Cce RR: - Subject: First Language - KANNADADocumento8 páginasCce RR: - Subject: First Language - KANNADAPRADEE2UAinda não há avaliações

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Azf - Azf.Ap9.B.: Subject MathematicsDocumento19 páginasAzf - Azf.Ap9.B.: Subject MathematicsPRADEE2UAinda não há avaliações

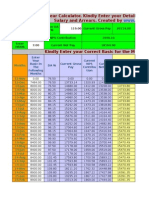

- Salary and Arrear Calculator. Kindly Enter Your Details in White Boxes For Calculation of Your Salary and Arrears. Created byDocumento4 páginasSalary and Arrear Calculator. Kindly Enter Your Details in White Boxes For Calculation of Your Salary and Arrears. Created byPRADEE2UAinda não há avaliações

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Bombay Stock ExchangeDocumento5 páginasBombay Stock ExchangeAnonymous NSNpGa3T93Ainda não há avaliações

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- SMEDA Spices Processing, Packing & Marketing111Documento6 páginasSMEDA Spices Processing, Packing & Marketing111Jahangir AliAinda não há avaliações

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Ranjani-211420631111 RemovedDocumento91 páginasRanjani-211420631111 RemovedSangeethaAinda não há avaliações

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- Forecasting Brigham Case SolutionDocumento7 páginasForecasting Brigham Case SolutionShahid Mehmood100% (1)

- Invesrment in Debt InstrumentsDocumento2 páginasInvesrment in Debt InstrumentsElla MontefalcoAinda não há avaliações

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- FINS3625 Case Study Report Davy Edit 1Documento15 páginasFINS3625 Case Study Report Davy Edit 1DavyZhouAinda não há avaliações

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Statement September 2021Documento1 páginaStatement September 2021Julio DelarozaAinda não há avaliações

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Ap A2.1 - FinalDocumento7 páginasAp A2.1 - FinalLuna LeeAinda não há avaliações

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- Quiz 2 Financial Accounting SolutionsDocumento5 páginasQuiz 2 Financial Accounting SolutionsScribdTranslationsAinda não há avaliações

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- CFAS 2020 Chapter 15 and MC ProblemsDocumento7 páginasCFAS 2020 Chapter 15 and MC Problems4220019Ainda não há avaliações

- Compound Financial InstrumentsDocumento3 páginasCompound Financial InstrumentsJm atlavs100% (1)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Cips L2M5Documento8 páginasCips L2M5dalia.diab.86Ainda não há avaliações

- FMT2 1Documento21 páginasFMT2 1Abhinav AgarwalAinda não há avaliações

- Campbell + Snyder'sTranscriptsDocumento12 páginasCampbell + Snyder'sTranscriptsYashJainAinda não há avaliações

- Stock Trading ChallengeDocumento9 páginasStock Trading ChallengeMiguel MartinezAinda não há avaliações

- Financial Modelling: ACST2001Documento17 páginasFinancial Modelling: ACST2001Nam Nam NamAinda não há avaliações

- AEXXDocumento11 páginasAEXXMohammad Sa-ad IndarAinda não há avaliações

- 3 CFSDocumento65 páginas3 CFSRocky Bassig100% (1)

- Cost of Goods Sold: Sales CommissionDocumento7 páginasCost of Goods Sold: Sales Commissionaparna153Ainda não há avaliações

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Accounting RatiosDocumento42 páginasAccounting RatiosApollo Institute of Hospital AdministrationAinda não há avaliações

- Applied Corporate Finance Assignment No. 1: C O B A M O B A (M) S F 2021-2022Documento4 páginasApplied Corporate Finance Assignment No. 1: C O B A M O B A (M) S F 2021-2022Hamda alzarooniAinda não há avaliações

- CH 4 - Intermediate Accounting Test BankDocumento51 páginasCH 4 - Intermediate Accounting Test BankCorliss Ko100% (11)

- Round: 0 Dec. 31, 2016: Selected Financial StatisticsDocumento11 páginasRound: 0 Dec. 31, 2016: Selected Financial Statisticsredditor1276Ainda não há avaliações

- The Dark Side of Valuation (Slides)Documento98 páginasThe Dark Side of Valuation (Slides)Johnathan Fitz KennedyAinda não há avaliações

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- 2024 Becker CPA Financial (FAR) Mock Exam AnswersDocumento28 páginas2024 Becker CPA Financial (FAR) Mock Exam AnswerscraigsappletreeAinda não há avaliações

- 50726b-624b876dcb855a000f5ca0a0-1649117080-Week 1-3 - ULOe - Practice ProblemDocumento3 páginas50726b-624b876dcb855a000f5ca0a0-1649117080-Week 1-3 - ULOe - Practice ProblemEagle OrtegaAinda não há avaliações

- Commerce MCQs Practice Test 1Documento8 páginasCommerce MCQs Practice Test 1Nirakar GoudaAinda não há avaliações

- Simsr2 Mba B III FM Quep 1Documento4 páginasSimsr2 Mba B III FM Quep 1Priyanka ReddyAinda não há avaliações

- Company Law Revision Notes June 2022 PDFDocumento221 páginasCompany Law Revision Notes June 2022 PDFRanveer GurjarAinda não há avaliações

- Lumber Duty DepositsDocumento10 páginasLumber Duty DepositsForexliveAinda não há avaliações

- Unilever Pakistan Limited Annual Report 2016 Tcm1267 501352 enDocumento71 páginasUnilever Pakistan Limited Annual Report 2016 Tcm1267 501352 enHammad AslamAinda não há avaliações