Você também pode gostar

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Government Accounting ManualDocumento62 páginasGovernment Accounting ManualDez Za100% (1)

- XDepartmental Examination - Pricing DecisionsDocumento2 páginasXDepartmental Examination - Pricing DecisionsxorelliAinda não há avaliações

- Test Bank For Managerial AccountingDocumento54 páginasTest Bank For Managerial Accountingsadiq626100% (2)

- Cost AccountingDocumento23 páginasCost AccountingxorelliAinda não há avaliações

- Introduction To MASDocumento10 páginasIntroduction To MASxorelli100% (8)

- Accounts Receivable and Receivable FinancingDocumento4 páginasAccounts Receivable and Receivable FinancingLui50% (2)

- FARAP-4501 (Cash and Cash Equivalents)Documento10 páginasFARAP-4501 (Cash and Cash Equivalents)Marya NvlzAinda não há avaliações

- Intercompany Profit Transactions - Inventories: Answers To Questions 1Documento22 páginasIntercompany Profit Transactions - Inventories: Answers To Questions 1NisrinaPArisantyAinda não há avaliações

- Accounting TheoryDocumento61 páginasAccounting TheoryxorelliAinda não há avaliações

- UC 101 Exam MidDocumento1 páginaUC 101 Exam MidxorelliAinda não há avaliações

- UC 101 Exam PrelDocumento2 páginasUC 101 Exam PrelxorelliAinda não há avaliações

- 563d24a8-2ae4-487f-9818-f2acb8108caeDocumento6 páginas563d24a8-2ae4-487f-9818-f2acb8108caeSwamy Dhas DhasAinda não há avaliações

- Suspense Accounts and The Correction of ErrorsDocumento3 páginasSuspense Accounts and The Correction of ErrorsVishal Paupiah0% (1)

- Cost Audit ReportDocumento20 páginasCost Audit ReportVishesh DwivediAinda não há avaliações

- Management Accounting OverviewDocumento27 páginasManagement Accounting Overviewfreya cuevasAinda não há avaliações

- AST LTCC ComputationDocumento9 páginasAST LTCC ComputationeiraAinda não há avaliações

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Documento3 páginasStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderAinda não há avaliações

- Jadwal Interview Analisa Jabatan BP V 2Documento3 páginasJadwal Interview Analisa Jabatan BP V 2Reza ZachrandAinda não há avaliações

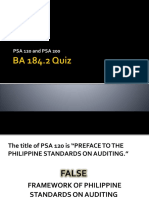

- PSA 120 and PSA 200Documento26 páginasPSA 120 and PSA 200Anna CastroAinda não há avaliações

- Monthly Sales: PriceDocumento5 páginasMonthly Sales: PriceChicken NoodlesAinda não há avaliações

- April and Arias Partnership Financial StatementDocumento8 páginasApril and Arias Partnership Financial StatementJames Jharred UmlasAinda não há avaliações

- FINAL LPU ACCOUNTS Avinash BeheraDocumento11 páginasFINAL LPU ACCOUNTS Avinash BeheraAvinash BeheraAinda não há avaliações

- Financial Statement AnalysisDocumento6 páginasFinancial Statement AnalysisJasper Briones IIAinda não há avaliações

- Factors Influencing The Level of Compliance With International Financial Reporting Standards by Small and Medium Scale Enterprises in Ondo State, NigeriaDocumento10 páginasFactors Influencing The Level of Compliance With International Financial Reporting Standards by Small and Medium Scale Enterprises in Ondo State, NigeriaPremier PublishersAinda não há avaliações

- Accounting Principles and ConceptsDocumento31 páginasAccounting Principles and ConceptskunyangAinda não há avaliações

- Management Controls PDF FreeDocumento78 páginasManagement Controls PDF FreeJohn Rich GamasAinda não há avaliações

- 02 - Angkasa Pura II - AR 2019Documento630 páginas02 - Angkasa Pura II - AR 2019Julian HutabaratAinda não há avaliações

- Ummary of Study Objectives: 312 Internal Control and CashDocumento5 páginasUmmary of Study Objectives: 312 Internal Control and CashchandoraAinda não há avaliações

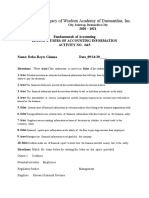

- Legacy of Wisdom Academy of Dasmariñas, IncDocumento2 páginasLegacy of Wisdom Academy of Dasmariñas, InczavriaAinda não há avaliações

- Finance Chapter No 2Documento20 páginasFinance Chapter No 2UzairAinda não há avaliações

- ACCT6003 Assessment 2 T1 2020 Brief PDFDocumento7 páginasACCT6003 Assessment 2 T1 2020 Brief PDFbhavikaAinda não há avaliações

- AAA Company Financial PositionDocumento4 páginasAAA Company Financial PositionEthan Michael CorralesAinda não há avaliações

- Just Dial's Q2 FY20 resultsDocumento10 páginasJust Dial's Q2 FY20 resultsGovardhan RaviAinda não há avaliações

- Finals Quiz Assignment Private Equity Valuation Method With AnswersDocumento3 páginasFinals Quiz Assignment Private Equity Valuation Method With AnswersRille Estrada CabanesAinda não há avaliações

- The Contribution of Systems TheoryDocumento14 páginasThe Contribution of Systems TheoryDaniela LomarttiAinda não há avaliações

- Career Objective: Curriculum VitaeDocumento3 páginasCareer Objective: Curriculum VitaeThanh X TranAinda não há avaliações