Você também pode gostar

- Home Office, Branch and Agency AccountingDocumento17 páginasHome Office, Branch and Agency AccountingJoanne TolentinoAinda não há avaliações

- Lesson 4 Accounting For Home OfficeDocumento8 páginasLesson 4 Accounting For Home OfficeheyheyAinda não há avaliações

- CMPC 221 Punzalan PDFDocumento9 páginasCMPC 221 Punzalan PDFRialeeAinda não há avaliações

- MidtermQ2 - Home Office Branch Accounting Billing Above CostDocumento7 páginasMidtermQ2 - Home Office Branch Accounting Billing Above Costsarahbee33% (3)

- Home Office and Branch Accounting ProblemsDocumento6 páginasHome Office and Branch Accounting ProblemsMary Dale Joie Bocala100% (1)

- DocDocumento5 páginasDocYour Materials33% (3)

- P2 105 Agency Home Office and Branch Accounting Key AnswersDocumento6 páginasP2 105 Agency Home Office and Branch Accounting Key AnswersHikari100% (1)

- HOBA Problem SetDocumento3 páginasHOBA Problem SetFayehAmantilloBingcangAinda não há avaliações

- Home Office and Branch Acccounting 2020Documento3 páginasHome Office and Branch Acccounting 2020ReilpeterAinda não há avaliações

- Home Office, Branch and Agency AccountingDocumento15 páginasHome Office, Branch and Agency AccountingErwin Labayog MedinaAinda não há avaliações

- Aa2e Hal Testbank Ch04Documento26 páginasAa2e Hal Testbank Ch04jayAinda não há avaliações

- Home Office IntegDocumento9 páginasHome Office IntegReshielyn Vee Entrampas LopezAinda não há avaliações

- Accounting principles for branches and agenciesDocumento4 páginasAccounting principles for branches and agenciesJohn Bryan100% (1)

- Afar 2Documento24 páginasAfar 2KriztleKateMontealtoGelogo100% (1)

- Case 1 - Computations of GW or IFADocumento3 páginasCase 1 - Computations of GW or IFAJem Valmonte0% (1)

- Home Office and Branch AccountingDocumento5 páginasHome Office and Branch Accountingjelviee1575% (4)

- OfficeDocumento12 páginasOffice123r12f1100% (1)

- Billed price calculations for home office and branch shipmentsDocumento4 páginasBilled price calculations for home office and branch shipmentsJohnmichael Coroza0% (1)

- Final Examination in Business Combi 2021Documento7 páginasFinal Examination in Business Combi 2021Michael BongalontaAinda não há avaliações

- Installment Sales Multiple QuestionsDocumento36 páginasInstallment Sales Multiple QuestionsTrixie CapisosAinda não há avaliações

- ADV2 Chapter12 QADocumento4 páginasADV2 Chapter12 QAMa Alyssa DelmiguezAinda não há avaliações

- Advanced Accounting Home Office, Branch and Agency TransactionsDocumento7 páginasAdvanced Accounting Home Office, Branch and Agency TransactionsMajoy Bantoc100% (1)

- HOBA QuestionsDocumento7 páginasHOBA QuestionsKristine CorporalAinda não há avaliações

- 2 - Home Office and Branch, Joint VentureDocumento6 páginas2 - Home Office and Branch, Joint VentureJason Bautista0% (1)

- HOBA - Practice SetDocumento5 páginasHOBA - Practice SetCarl Dhaniel Garcia SalenAinda não há avaliações

- Hoba 2019 QuizDocumento10 páginasHoba 2019 QuizJo Montes0% (1)

- Home Office and BranchDocumento4 páginasHome Office and BranchRed YuAinda não há avaliações

- AA2Q1Documento1 páginaAA2Q1Sweet EmmeAinda não há avaliações

- Requirement: Prepare Journal Entries in The Books of The Home Office and in The Books of The Branch Office ForDocumento2 páginasRequirement: Prepare Journal Entries in The Books of The Home Office and in The Books of The Branch Office ForvonnevaleAinda não há avaliações

- Business Combinations ExplainedDocumento8 páginasBusiness Combinations ExplainedLabLab ChattoAinda não há avaliações

- Home Office and Branch Accounting: Trial Balances, Adjustments, and Financial StatementsDocumento4 páginasHome Office and Branch Accounting: Trial Balances, Adjustments, and Financial StatementsMaurice AgbayaniAinda não há avaliações

- Responsibility Accounting and Transfer Pricing: Variable Costing & Segmented ReportingDocumento8 páginasResponsibility Accounting and Transfer Pricing: Variable Costing & Segmented ReportingJonailyn YR PeraltaAinda não há avaliações

- Advanced Accounting Part II Quiz 1 Home Office and Branch AccountingDocumento10 páginasAdvanced Accounting Part II Quiz 1 Home Office and Branch AccountingAzyrah Lyren Seguban UlpindoAinda não há avaliações

- CMPC Quiz 2Documento5 páginasCMPC Quiz 2Mae-shane Sagayo50% (2)

- C Par First Pre Board 2008 ADocumento17 páginasC Par First Pre Board 2008 AJaylord Pido100% (1)

- Home Office and Branch Accounting Covidproject4accountants Aug 2020 PDFDocumento9 páginasHome Office and Branch Accounting Covidproject4accountants Aug 2020 PDFKathrina RoxasAinda não há avaliações

- Problems Chapter 11 and 12Documento8 páginasProblems Chapter 11 and 12u got no jamsAinda não há avaliações

- HOBADocumento4 páginasHOBAHannah YnciertoAinda não há avaliações

- Activity 1 Home Office and Branch Accounting - General ProceduresDocumento4 páginasActivity 1 Home Office and Branch Accounting - General ProceduresDaenielle EspinozaAinda não há avaliações

- BAC 318 Final Examination With AnswersDocumento10 páginasBAC 318 Final Examination With Answersjanus lopez100% (1)

- P2 03v2Documento5 páginasP2 03v2Rhegee Irene RosarioAinda não há avaliações

- BRanch and Home OfficeDocumento1 páginaBRanch and Home OfficeSharonLargosaGabrielAinda não há avaliações

- HOBA ProblemsDocumento3 páginasHOBA ProblemsEmma Mariz Garcia67% (3)

- Home Office BranchDocumento5 páginasHome Office BranchRodAinda não há avaliações

- Toaz - Info Afar PRDocumento95 páginasToaz - Info Afar PRMiraflor Sanchez BiñasAinda não há avaliações

- Accounting for Home Office, Branch and Agency TransactionsDocumento30 páginasAccounting for Home Office, Branch and Agency TransactionsHarvey Dienne Quiambao100% (3)

- 4 Home Office Agency Handout SolutionDocumento15 páginas4 Home Office Agency Handout SolutionRyan CornistaAinda não há avaliações

- Cost To CostDocumento1 páginaCost To CostAnirban Roy ChowdhuryAinda não há avaliações

- Chapter 8: Home Office, Branch, and Agency AccountingDocumento32 páginasChapter 8: Home Office, Branch, and Agency Accountingjammy Agno50% (2)

- C. The Results of Operations, Cash Flow, and The Balance Sheet As If The Parent and Subsidiary Were A Single EntityDocumento13 páginasC. The Results of Operations, Cash Flow, and The Balance Sheet As If The Parent and Subsidiary Were A Single EntityAlijah MercadoAinda não há avaliações

- Trial Balance Home Office DR (CR) Branch Office DR (CR)Documento2 páginasTrial Balance Home Office DR (CR) Branch Office DR (CR)Adriana CarinanAinda não há avaliações

- Home Office Branch Accounting at CostDocumento12 páginasHome Office Branch Accounting at Costsarahbee100% (2)

- AFAR Assessment October 2020Documento8 páginasAFAR Assessment October 2020FelixAinda não há avaliações

- Define Fraud, and Explain The Two Types of Misstatements That Are Relevant To Auditors' Consideration of FraudDocumento3 páginasDefine Fraud, and Explain The Two Types of Misstatements That Are Relevant To Auditors' Consideration of FraudSomething ChicAinda não há avaliações

- Afar - Business Combinations - Mergers Ellery de Leon Far Eastern UniversityDocumento3 páginasAfar - Business Combinations - Mergers Ellery de Leon Far Eastern UniversityRyan Joseph Agluba Dimacali50% (2)

- NFJPIA Mockboard 2011 P2Documento13 páginasNFJPIA Mockboard 2011 P2Regie Sharry Alutang PanisAinda não há avaliações

- Advanced Financial Accounting Chapter 2 LECTURE - NOTESDocumento14 páginasAdvanced Financial Accounting Chapter 2 LECTURE - NOTESAshenafi ZelekeAinda não há avaliações

- p2Documento8 páginasp2elizaAinda não há avaliações

- 3004 Home Office and BranchesDocumento6 páginas3004 Home Office and BranchesTatianaAinda não há avaliações

- Excel Professional Services Financial Statement InsightsDocumento7 páginasExcel Professional Services Financial Statement InsightsAzriele Rayne Fajardo BenozaAinda não há avaliações

- Monopolistic Competition and MonopolyDocumento4 páginasMonopolistic Competition and MonopolysarahbeeAinda não há avaliações

- Standard Costing and Variance AnalysisDocumento5 páginasStandard Costing and Variance AnalysissarahbeeAinda não há avaliações

- Acctg201 Assignment 1Documento7 páginasAcctg201 Assignment 1sarahbeeAinda não há avaliações

- Acctg201 Exercises2Documento18 páginasAcctg201 Exercises2sarahbeeAinda não há avaliações

- Standard Cost and Variance Analysis SeatworkDocumento2 páginasStandard Cost and Variance Analysis SeatworksarahbeeAinda não há avaliações

- Cost Concepts and ClassificationsDocumento19 páginasCost Concepts and ClassificationssarahbeeAinda não há avaliações

- Product CostingDocumento10 páginasProduct CostingsarahbeeAinda não há avaliações

- Standard Costing and Variance Analysis Problems Exam SolutionDocumento5 páginasStandard Costing and Variance Analysis Problems Exam SolutionsarahbeeAinda não há avaliações

- ACCTG 201 Illustrative ProblemsDocumento4 páginasACCTG 201 Illustrative ProblemsJewel Anne RentumaAinda não há avaliações

- Standard CostingDocumento7 páginasStandard CostingsarahbeeAinda não há avaliações

- Accounting 201 Cost Accounting Exam ReviewDocumento11 páginasAccounting 201 Cost Accounting Exam Reviewsarahbee75% (4)

- Job Order Costing Difficult RoundDocumento8 páginasJob Order Costing Difficult RoundsarahbeeAinda não há avaliações

- Job Order Costing SeatworkDocumento7 páginasJob Order Costing SeatworksarahbeeAinda não há avaliações

- Job Order Costing QuizbowlDocumento27 páginasJob Order Costing QuizbowlsarahbeeAinda não há avaliações

- Exercise 5 Short Computations Backflush CostingDocumento2 páginasExercise 5 Short Computations Backflush CostingsarahbeeAinda não há avaliações

- Exercise 6-1 (Classification of Cost Drivers)Documento18 páginasExercise 6-1 (Classification of Cost Drivers)Barrylou ManayanAinda não há avaliações

- Process Costing Exercises Series 1Documento23 páginasProcess Costing Exercises Series 1sarahbeeAinda não há avaliações

- Cost AccountingDocumento6 páginasCost Accountingulquira grimamajowAinda não há avaliações

- Process Costing Exercises Series 1Documento23 páginasProcess Costing Exercises Series 1sarahbeeAinda não há avaliações

- Sales (De Leon)Documento737 páginasSales (De Leon)Bj Carido100% (7)

- ZARA CaseStudy Group5 FinalDocumento16 páginasZARA CaseStudy Group5 Finalsarahbee100% (1)

- Job Order Costing SeatworkDocumento7 páginasJob Order Costing SeatworksarahbeeAinda não há avaliações

- Journal of Business EthicsDocumento13 páginasJournal of Business EthicssarahbeeAinda não há avaliações

- Corporation Commencement ExceptionsDocumento10 páginasCorporation Commencement ExceptionssarahbeeAinda não há avaliações

- Sustainability Reporting in The PhilippinesDocumento45 páginasSustainability Reporting in The PhilippinessarahbeeAinda não há avaliações

- Gitman Chapter4Documento49 páginasGitman Chapter4sarahbeeAinda não há avaliações

- Complex Adaptive SystemsDocumento9 páginasComplex Adaptive Systemssprobooste100% (1)

- Sustainability 09 02112 PDFDocumento12 páginasSustainability 09 02112 PDFTawsif HasanAinda não há avaliações

- Resonance Performance ModelDocumento20 páginasResonance Performance ModelsarahbeeAinda não há avaliações

- 20201111report Financial Report December 2020 TheresidencesatbrentDocumento18 páginas20201111report Financial Report December 2020 TheresidencesatbrentChaAinda não há avaliações

- ULOa Let's Analyze Week 8 9Documento2 páginasULOa Let's Analyze Week 8 9emem resuentoAinda não há avaliações

- Adjusting Process PDFDocumento47 páginasAdjusting Process PDFJohn Oliver D. OcampoAinda não há avaliações

- Finance Process Flow in JDEDocumento35 páginasFinance Process Flow in JDERamesh KumarAinda não há avaliações

- Partnership profit distribution and capital account changesDocumento4 páginasPartnership profit distribution and capital account changesMaria Carmela MoraudaAinda não há avaliações

- Banana Bell Patty Income StatementDocumento2 páginasBanana Bell Patty Income StatementLyanAinda não há avaliações

- Las 4Documento8 páginasLas 4Venus Abarico Banque-AbenionAinda não há avaliações

- Financial Reporting Act 2015 BNDocumento31 páginasFinancial Reporting Act 2015 BNOsman GoniAinda não há avaliações

- Chapter 2 JournalizingDocumento21 páginasChapter 2 Journalizingkakao100% (1)

- IFRS Diploma Answers 2015Documento7 páginasIFRS Diploma Answers 2015Soňa SlovákováAinda não há avaliações

- FinancialPlan - 2013 Version - Prof DR IsmailDocumento129 páginasFinancialPlan - 2013 Version - Prof DR IsmailSyukur Byte0% (1)

- Chap-2 Quản trị tài chínhDocumento12 páginasChap-2 Quản trị tài chínhQuế Anh TrươngAinda não há avaliações

- Annual-Report-13-14 AOP PDFDocumento38 páginasAnnual-Report-13-14 AOP PDFkhurram_66Ainda não há avaliações

- CPM Construction Company AccountingDocumento6 páginasCPM Construction Company AccountingPrita HerdiantiAinda não há avaliações

- Oktay Urcan: Financial Accounting: Advanced TopicsDocumento39 páginasOktay Urcan: Financial Accounting: Advanced TopicsRishap JindalAinda não há avaliações

- Cash Flow StatementDocumento19 páginasCash Flow StatementROHIT SHAAinda não há avaliações

- Ey Leases A Summary of Ifrs 16Documento28 páginasEy Leases A Summary of Ifrs 16Wedi TassewAinda não há avaliações

- Sarath & Associates: To The Board of Directors of GSS Infotech LimitedDocumento9 páginasSarath & Associates: To The Board of Directors of GSS Infotech LimitedAkshay AKAinda não há avaliações

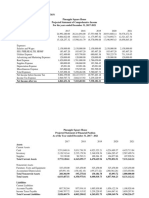

- Five-Year Financial Projection Pineapple Square House Projected Statement of Comprehensive Income For The Years Ended December 31, 2017-2021Documento4 páginasFive-Year Financial Projection Pineapple Square House Projected Statement of Comprehensive Income For The Years Ended December 31, 2017-2021Rey PordalizaAinda não há avaliações

- Wa0000 PDFDocumento12 páginasWa0000 PDFsipheleleAinda não há avaliações

- Laporan Keuangan PT BFI Finance IndonesiaDocumento103 páginasLaporan Keuangan PT BFI Finance IndonesiaAdi HamdaniAinda não há avaliações

- Fsa Solved ProblemsDocumento27 páginasFsa Solved ProblemsKumarVelivela100% (1)

- Financial Accountinng 3Documento10 páginasFinancial Accountinng 3Nami2mititAinda não há avaliações

- Liquidity and Solvency Ratios: Google vs Yahoo 2015Documento57 páginasLiquidity and Solvency Ratios: Google vs Yahoo 2015cvilalobos198527100% (1)

- Cfas Cash Flow Theories and ProblemsDocumento30 páginasCfas Cash Flow Theories and ProblemsIris MnemosyneAinda não há avaliações

- Akuntansi DagangDocumento13 páginasAkuntansi DagangAsmarani SiregarAinda não há avaliações

- Test Bank For Intermediate Accounting 13th Edition Donald e KiesoDocumento36 páginasTest Bank For Intermediate Accounting 13th Edition Donald e Kiesoheatingbultow.ji9fo100% (42)

- Business Finance - Horizontal AnalysisDocumento2 páginasBusiness Finance - Horizontal AnalysisAnon0% (1)

- Lecture Notes 2 Formation of A PartnershipDocumento14 páginasLecture Notes 2 Formation of A PartnershipMegapoplocker MegapoplockerAinda não há avaliações

- Key Words: Multiple Choice QuestionsDocumento7 páginasKey Words: Multiple Choice QuestionsMOHAMMED AMIN SHAIKHAinda não há avaliações