Você também pode gostar

- Assignment 2 (Set 2)Documento7 páginasAssignment 2 (Set 2)sashaAinda não há avaliações

- Corporate social responsibility A Complete Guide - 2019 EditionNo EverandCorporate social responsibility A Complete Guide - 2019 EditionAinda não há avaliações

- Proposals For ResearchDocumento6 páginasProposals For ResearchJayman Tamang0% (1)

- Mini Marketing Plan OutlineDocumento8 páginasMini Marketing Plan Outlineapi-323496212Ainda não há avaliações

- Creating Customer ValueDocumento11 páginasCreating Customer Valuepaul jacksonAinda não há avaliações

- Attitude of EmployeesDocumento8 páginasAttitude of EmployeesVishal SoodanAinda não há avaliações

- Function of InsuranceDocumento3 páginasFunction of Insuranceviveksingh153Ainda não há avaliações

- Success in Business.Documento26 páginasSuccess in Business.Lamyae ez- zghari100% (1)

- Chapter 01 Long Term Investing and Financial DecisionsDocumento30 páginasChapter 01 Long Term Investing and Financial DecisionsNida FatimaAinda não há avaliações

- Assignment CSR #2Documento3 páginasAssignment CSR #2Gerald F. SalasAinda não há avaliações

- Environmental Scan PaperDocumento10 páginasEnvironmental Scan PaperDESMOND42Ainda não há avaliações

- Customer Loyalty and Brand Management - Natalia Rubio and Maria JesusDocumento125 páginasCustomer Loyalty and Brand Management - Natalia Rubio and Maria JesusANA JHOSSELYN PEREZ VELASQUEZAinda não há avaliações

- Mission Vision CdaDocumento3 páginasMission Vision CdaVirginia BuezaAinda não há avaliações

- Executive Briefing For The Santa Fe Grill Case StudyDocumento10 páginasExecutive Briefing For The Santa Fe Grill Case StudyShadab Qureshi0% (1)

- HRIS PreDocumento18 páginasHRIS PreMony Mst100% (1)

- Review Related LiteratureDocumento7 páginasReview Related LiteratureKate CorralesAinda não há avaliações

- Corporate Social Responsibility and Consumer Buying Behavior in Emerging MarketDocumento23 páginasCorporate Social Responsibility and Consumer Buying Behavior in Emerging MarketRoxana NicolaeAinda não há avaliações

- Mba Project - ProposalDocumento6 páginasMba Project - ProposalJijulal NairAinda não há avaliações

- Carrefour CSRDocumento3 páginasCarrefour CSRTapochekAinda não há avaliações

- Career Goal Analysis and Action Plan-1-1Documento9 páginasCareer Goal Analysis and Action Plan-1-1api-314537200Ainda não há avaliações

- Which Small Businesses Are Most Vulnerable To COVID 19 and WhenDocumento10 páginasWhich Small Businesses Are Most Vulnerable To COVID 19 and WhenBusiness Families Foundation100% (1)

- Factors Affecting Financial Sustainability of Microfinance InstitutionsDocumento10 páginasFactors Affecting Financial Sustainability of Microfinance InstitutionsAlexander DeckerAinda não há avaliações

- Research ProposalDocumento5 páginasResearch ProposalPrajay PatelAinda não há avaliações

- Marketing Assignment Case Study On Heinz WattieDocumento10 páginasMarketing Assignment Case Study On Heinz WattieShahinAinda não há avaliações

- Funding Mobilization in Non Govermental Organizations: A Case of World Food ProgrammeDocumento63 páginasFunding Mobilization in Non Govermental Organizations: A Case of World Food ProgrammeInternational Journal of Innovative Science and Research TechnologyAinda não há avaliações

- Paper Presentation ConferenceDocumento15 páginasPaper Presentation ConferenceSurbhi JainAinda não há avaliações

- Proffessional Development For Strategic Manager SohaillllllllllDocumento13 páginasProffessional Development For Strategic Manager SohaillllllllllFred ChukwuAinda não há avaliações

- Role of Self Help Groups in Financial InclusionDocumento6 páginasRole of Self Help Groups in Financial InclusionSona Kool100% (1)

- Analysis of Supply Chain Social Sustainability in Hotel IndustryDocumento5 páginasAnalysis of Supply Chain Social Sustainability in Hotel IndustryIJAR JOURNALAinda não há avaliações

- Tesla PPTDocumento8 páginasTesla PPTfatima afzalAinda não há avaliações

- Writing A Social Enterprise Business PlanDocumento27 páginasWriting A Social Enterprise Business PlanRoosvelt TalabertAinda não há avaliações

- How CSR Pays OffDocumento8 páginasHow CSR Pays OffAldrin Benitez Jumaquio100% (1)

- The Importance of School Events 2Documento5 páginasThe Importance of School Events 2zach king0% (1)

- Eng 105 ResearchDocumento35 páginasEng 105 ResearchSamy AbdullahAinda não há avaliações

- Practical Research Body TemplateDocumento107 páginasPractical Research Body TemplateCymer Aron VerzosaAinda não há avaliações

- Milo MaterialsDocumento17 páginasMilo MaterialsNwabuisi PamelaAinda não há avaliações

- MGT1023-Fundamentals of Human Resource Management Digital Assignment - 1Documento5 páginasMGT1023-Fundamentals of Human Resource Management Digital Assignment - 1Ram Prasad ReddyAinda não há avaliações

- Role of Public Relations For Effective Communications in NGOsDocumento3 páginasRole of Public Relations For Effective Communications in NGOsgotcanAinda não há avaliações

- Challenges of CSR & ExamplesDocumento4 páginasChallenges of CSR & ExamplesAkmal HassanAinda não há avaliações

- Business Environment Refers To Different Forces or Surroundings That Affect Business OperationsDocumento9 páginasBusiness Environment Refers To Different Forces or Surroundings That Affect Business Operationsmldc2011Ainda não há avaliações

- Customer Satisfaction On Service Quality in Private Commercial Banking Sector in BangladeshDocumento11 páginasCustomer Satisfaction On Service Quality in Private Commercial Banking Sector in BangladeshUmar KhanAinda não há avaliações

- From Corporate Social Responsibility To Creating Shared Value. A Case Study From Tetra PakDocumento55 páginasFrom Corporate Social Responsibility To Creating Shared Value. A Case Study From Tetra PakMuhammad Farhan100% (1)

- Impact Financial Literacy PDFDocumento10 páginasImpact Financial Literacy PDFberardeusAinda não há avaliações

- Admissions-Policy Bradford UniversityDocumento8 páginasAdmissions-Policy Bradford UniversityAppu Jain100% (1)

- Silicon Valley Trip Reflective EssayDocumento6 páginasSilicon Valley Trip Reflective Essaymatthew.brightAinda não há avaliações

- Client Service Quality of The Board of InvestmentsDocumento12 páginasClient Service Quality of The Board of InvestmentsIza EstinopoAinda não há avaliações

- NGO and Rular Development PresentationDocumento11 páginasNGO and Rular Development PresentationEfty M E IslamAinda não há avaliações

- Environmental Scan PaperDocumento5 páginasEnvironmental Scan PaperLatasha Hill RandleAinda não há avaliações

- Bis EthicDocumento32 páginasBis EthicThe SymphonyAinda não há avaliações

- Corporate Social Responsibility - Wikipedia PDFDocumento163 páginasCorporate Social Responsibility - Wikipedia PDFAntony RobinsonAinda não há avaliações

- Case StudyDocumento9 páginasCase StudyGoharAinda não há avaliações

- Pure It Case StudyDocumento6 páginasPure It Case StudyTaskin SadmanAinda não há avaliações

- 2012 Business Plan DraftDocumento27 páginas2012 Business Plan DraftGrimlitchAinda não há avaliações

- Assignment IB LeadershipDocumento18 páginasAssignment IB Leadershipsasha100% (1)

- Influence of Social Media Marketing On Consumer Buying Decision Making ProcessDocumento5 páginasInfluence of Social Media Marketing On Consumer Buying Decision Making ProcessAyessa Faye Dayag FernandoAinda não há avaliações

- The Growth of Small and Medium Enterprises in Malaysia: A Study On Private Limited Companies in Perak MalaysiaDocumento6 páginasThe Growth of Small and Medium Enterprises in Malaysia: A Study On Private Limited Companies in Perak MalaysiaRieska foni YuniarAinda não há avaliações

- Research ProposalDocumento16 páginasResearch ProposalWamani Linus KirungiAinda não há avaliações

- P.D.S MotivationDocumento12 páginasP.D.S MotivationAgrippa MungaziAinda não há avaliações

- Development Processes and The Development IndustryDocumento30 páginasDevelopment Processes and The Development IndustryDHAMODHARANAinda não há avaliações

- Atomic Structuure and BondingDocumento6 páginasAtomic Structuure and BondingHarshika Prasanganie Abeydeera100% (1)

- A Critical Analysis of The Issues Women Face in Male Dominated Sports in PennsylvaniaDocumento24 páginasA Critical Analysis of The Issues Women Face in Male Dominated Sports in PennsylvaniaHarshika Prasanganie AbeydeeraAinda não há avaliações

- Unit 2 Health&SafetyDocumento8 páginasUnit 2 Health&SafetyHarshika Prasanganie AbeydeeraAinda não há avaliações

- 3M HIP Series 3930 - CALCOAST Report - 2020 With Weathering Test DataDocumento21 páginas3M HIP Series 3930 - CALCOAST Report - 2020 With Weathering Test DataHarshika Prasanganie AbeydeeraAinda não há avaliações

- Chemical Calculations 2Documento6 páginasChemical Calculations 2Harshika Prasanganie Abeydeera100% (1)

- Spelling List-Grade 4Documento1 páginaSpelling List-Grade 4Harshika Prasanganie AbeydeeraAinda não há avaliações

- Clause 8 Commencement Delays and Suspension: Cross-ReferencesDocumento17 páginasClause 8 Commencement Delays and Suspension: Cross-ReferencesHatem HejaziAinda não há avaliações

- EOP: Existing Edge of Pavement Legend:: Carriage WAY Carriage WAYDocumento1 páginaEOP: Existing Edge of Pavement Legend:: Carriage WAY Carriage WAYHarshika Prasanganie AbeydeeraAinda não há avaliações

- Energy OL 3Documento8 páginasEnergy OL 3Harshika Prasanganie AbeydeeraAinda não há avaliações

- EOP: Existing Edge of Pavement Legend:: Carriage WAY Carriage WAYDocumento1 páginaEOP: Existing Edge of Pavement Legend:: Carriage WAY Carriage WAYHarshika Prasanganie AbeydeeraAinda não há avaliações

- EOP: Existing Edge of Pavement Legend:: Carriage WAY Carriage WAYDocumento1 páginaEOP: Existing Edge of Pavement Legend:: Carriage WAY Carriage WAYHarshika Prasanganie AbeydeeraAinda não há avaliações

- BSR 2019Documento109 páginasBSR 2019aflal100% (3)

- Activity BookDocumento80 páginasActivity BookBinoy DeereshaAinda não há avaliações

- Covid-19 and FIDIC Contracts - What Protections and Entitlements?Documento5 páginasCovid-19 and FIDIC Contracts - What Protections and Entitlements?Harshika Prasanganie AbeydeeraAinda não há avaliações

- Ancient Mesopotamian CivilizationsDocumento1 páginaAncient Mesopotamian CivilizationsHarshika Prasanganie AbeydeeraAinda não há avaliações

- Improving Sustainability of The Construction Industry - An UK PerspectiveDocumento24 páginasImproving Sustainability of The Construction Industry - An UK PerspectiveHarshika Prasanganie AbeydeeraAinda não há avaliações

- 48 - MTR SIL903 Viaduct Presentation - 20130828Documento69 páginas48 - MTR SIL903 Viaduct Presentation - 20130828Jacky LeongAinda não há avaliações

- Adjustment of Contract Prices: Using Cida Formula MethodDocumento10 páginasAdjustment of Contract Prices: Using Cida Formula MethodHarshika Prasanganie AbeydeeraAinda não há avaliações

- Resolution of Construction DisputesDocumento15 páginasResolution of Construction DisputesHarshika Prasanganie AbeydeeraAinda não há avaliações

- Cost Effective Strategies For ArbitrationDocumento6 páginasCost Effective Strategies For ArbitrationHarshika Prasanganie AbeydeeraAinda não há avaliações

- Contractor Not Required To Notify Claim For EOT Until Delay Has Started PDFDocumento7 páginasContractor Not Required To Notify Claim For EOT Until Delay Has Started PDFHarshika Prasanganie AbeydeeraAinda não há avaliações

- Contractor Not Required To Notify Claim For EOT Until Delay Has Started PDFDocumento7 páginasContractor Not Required To Notify Claim For EOT Until Delay Has Started PDFHarshika Prasanganie AbeydeeraAinda não há avaliações

- ELE CatalogDocumento164 páginasELE CatalogHarshika Prasanganie AbeydeeraAinda não há avaliações

- Other 3 - Duties and LiabilitesDocumento54 páginasOther 3 - Duties and Liabilitesok_computer111Ainda não há avaliações

- PMcom 2019 03 PersonalDevelopmentPlan SlidesDocumento39 páginasPMcom 2019 03 PersonalDevelopmentPlan SlidesHarshika Prasanganie AbeydeeraAinda não há avaliações

- GRIG4 Part1 Reporting Principles and Standard DisclosuresDocumento97 páginasGRIG4 Part1 Reporting Principles and Standard DisclosuresalisaamAinda não há avaliações

- Extensions of Time Iconsult FinalDocumento31 páginasExtensions of Time Iconsult FinalGwapito Tres100% (3)

- Bridge, Retaining Wall, Culverts Construction ManualDocumento300 páginasBridge, Retaining Wall, Culverts Construction ManualHarshika Prasanganie AbeydeeraAinda não há avaliações

- 5110 18172 1 PBDocumento17 páginas5110 18172 1 PBamilapriyangaAinda não há avaliações

- Delays in ProjectDocumento44 páginasDelays in ProjectMohamed El ArabiAinda não há avaliações

- Job Interview Skills Question ListDocumento23 páginasJob Interview Skills Question ListFazal MahmoodAinda não há avaliações

- Doctrine of Piercing The Corporate Veil - Case DigestDocumento2 páginasDoctrine of Piercing The Corporate Veil - Case DigestlookalikenilongAinda não há avaliações

- How To Start A Consulting BusinessDocumento28 páginasHow To Start A Consulting BusinessSatyabrat DasAinda não há avaliações

- Call Data Record of Prashun Jain Sonu Jain Custosm House Agent Prashant Gupta Icdtkd Global Log Ic Noida Rajdhani Crafts JaipurDocumento13 páginasCall Data Record of Prashun Jain Sonu Jain Custosm House Agent Prashant Gupta Icdtkd Global Log Ic Noida Rajdhani Crafts JaipurjainAinda não há avaliações

- CATHOLIC SOCIAL-WPS OfficeDocumento3 páginasCATHOLIC SOCIAL-WPS OfficeDan Dan DanAinda não há avaliações

- Group 5 SSP NutriAsia Inc. 2Documento8 páginasGroup 5 SSP NutriAsia Inc. 2AlaineAinda não há avaliações

- Ideology and Methodology Duncan FoleyDocumento11 páginasIdeology and Methodology Duncan Foley신재석Ainda não há avaliações

- Paternity Leave LawDocumento2 páginasPaternity Leave LawVikki AmorioAinda não há avaliações

- Business Annals. Willard Long Thorp 8Documento16 páginasBusiness Annals. Willard Long Thorp 8kirchyAinda não há avaliações

- HR AuditDocumento27 páginasHR Auditsanyakap100% (1)

- Position Paper - Is Unemployment A Serious Problem of A CountryDocumento20 páginasPosition Paper - Is Unemployment A Serious Problem of A Countrydoreethy manaloAinda não há avaliações

- Massive Munchies 2Documento81 páginasMassive Munchies 2lvincent7Ainda não há avaliações

- RecruitmentandselectionDocumento22 páginasRecruitmentandselectionHarfizzie FatehAinda não há avaliações

- Educational Medical, Health and Family Welfare Department, Guntur-Staff NurseQualification Medical Health Family Welfare Dept Guntur Staff Nurse PostsDocumento4 páginasEducational Medical, Health and Family Welfare Department, Guntur-Staff NurseQualification Medical Health Family Welfare Dept Guntur Staff Nurse PostsTheTubeGuruAinda não há avaliações

- Maternity Benefit Act 1961Documento13 páginasMaternity Benefit Act 1961Sumit KumarAinda não há avaliações

- Kid English PDFDocumento30 páginasKid English PDFPhilBoardResultsAinda não há avaliações

- Mary Parker Follett and Chester BarnardDocumento4 páginasMary Parker Follett and Chester BarnardLyceum Lawlibrary100% (1)

- Operational Risk ManagementDocumento13 páginasOperational Risk ManagementVikram RautelaAinda não há avaliações

- Muhammad Akram Khan - Introduction To Islamic Economics PDFDocumento167 páginasMuhammad Akram Khan - Introduction To Islamic Economics PDFIsyfi Syifaa100% (6)

- Contoh Training Matrix Untuk K3Documento1 páginaContoh Training Matrix Untuk K3adec100% (1)

- MNIT Resume StructureDocumento3 páginasMNIT Resume StructurePrabhaMeenaAinda não há avaliações

- LA TONDEÑA WORKERS UNION Vs Sec of LAborDocumento2 páginasLA TONDEÑA WORKERS UNION Vs Sec of LAborJessy FrancisAinda não há avaliações

- Summer Training Project Report On: "Employee Motivation" AT Hyundai MotorsDocumento87 páginasSummer Training Project Report On: "Employee Motivation" AT Hyundai Motorssilent readersAinda não há avaliações

- Charles Martin in Uganda What To Do When A Manager Goes Native Case Study - International BusinessDocumento7 páginasCharles Martin in Uganda What To Do When A Manager Goes Native Case Study - International BusinessNicholas Shanto100% (2)

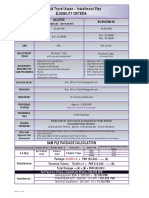

- Labbaik Travel Asaan - Installment Plan Eligibility CriteriaDocumento1 páginaLabbaik Travel Asaan - Installment Plan Eligibility CriteriamuhammadTzAinda não há avaliações

- Employment Physical ExamsDocumento2 páginasEmployment Physical ExamsraymundsugayAinda não há avaliações

- Social Perception and Managing DiversityDocumento28 páginasSocial Perception and Managing DiversityYusuf ArifinAinda não há avaliações

- What Is Web HostingDocumento6 páginasWhat Is Web Hostingrchl.nwtnAinda não há avaliações

- US Passport ApplicationDocumento6 páginasUS Passport ApplicationThe Slang Market100% (9)

- BMPM5103 AssignmentDocumento11 páginasBMPM5103 AssignmentbebetangAinda não há avaliações