Você também pode gostar

- FIN501 - Financial Management Mid Term Assignment - Zin Thet Nyo LwinDocumento16 páginasFIN501 - Financial Management Mid Term Assignment - Zin Thet Nyo LwinZin Thet InwonderlandAinda não há avaliações

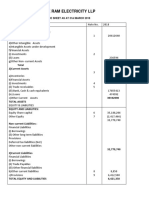

- Shree Ram Electricity LLP: 1) Non-Current AssetsDocumento5 páginasShree Ram Electricity LLP: 1) Non-Current AssetsSaba MullaAinda não há avaliações

- Exercises For Chapter 23 EFA2Documento13 páginasExercises For Chapter 23 EFA2tuananh leAinda não há avaliações

- Financial RatiosDocumento13 páginasFinancial RatiosAaron Coutinho0% (1)

- Measuring Financial Performance - HandoutDocumento11 páginasMeasuring Financial Performance - HandoutAjayi Adebayo Ebenezer-SuccessAinda não há avaliações

- Review Materials Financial ManagementDocumento9 páginasReview Materials Financial ManagementTOBIT JEHAZIEL SILVESTREAinda não há avaliações

- The Statement of Financial PositionDocumento18 páginasThe Statement of Financial PositionDanerish PabunanAinda não há avaliações

- Financial Planning and Forecasting Financial StatementsDocumento70 páginasFinancial Planning and Forecasting Financial StatementsAziz Hotelwala100% (1)

- Chapter 1 FNM108Documento13 páginasChapter 1 FNM108Aldrin John TungolAinda não há avaliações

- 14.04. CFS - Lecture Notes - StudentsDocumento39 páginas14.04. CFS - Lecture Notes - StudentsĐỗ Linh100% (1)

- 2018 - Session11 - 12 FSA - PGP - SentDocumento40 páginas2018 - Session11 - 12 FSA - PGP - SentArty DrillAinda não há avaliações

- Financial Statements Analysis: Bangko de Oro & Bank of The Philippine IslandsDocumento34 páginasFinancial Statements Analysis: Bangko de Oro & Bank of The Philippine IslandsNikol DayanAinda não há avaliações

- Discussion Question #5 Solution-Table 1.0 Shows The Order of Current Assets in Terms of Liquidity (Most To Least) Current AssetsDocumento7 páginasDiscussion Question #5 Solution-Table 1.0 Shows The Order of Current Assets in Terms of Liquidity (Most To Least) Current AssetsRijul DUbeyAinda não há avaliações

- Q1 Busfin PT 2021-2022Documento10 páginasQ1 Busfin PT 2021-2022Romano AbalosAinda não há avaliações

- CF Lecture 0 Working With FS v1Documento51 páginasCF Lecture 0 Working With FS v1Tâm NhưAinda não há avaliações

- Business Plan Work SheetDocumento17 páginasBusiness Plan Work SheetRey OñateAinda não há avaliações

- Capital University of Science and Technology: Honor StatementDocumento7 páginasCapital University of Science and Technology: Honor StatementPak KhAinda não há avaliações

- 01 ELMS Activity 1Documento2 páginas01 ELMS Activity 1Gonzaga FamAinda não há avaliações

- Financial Mod CH-2Documento7 páginasFinancial Mod CH-2Hawi DerebssaAinda não há avaliações

- Chapter 13 - Cfs - Lecture NotesDocumento36 páginasChapter 13 - Cfs - Lecture NotesTrung Võ ThànhAinda não há avaliações

- FIN2004 - 2704 Week 2 SlidesDocumento60 páginasFIN2004 - 2704 Week 2 SlidesJalen GohAinda não há avaliações

- Financial Statement Analysis Part 2Documento10 páginasFinancial Statement Analysis Part 2Kim Patrick VictoriaAinda não há avaliações

- Chapter IXDocumento3 páginasChapter IXCleo IlaoAinda não há avaliações

- Chapter IXDocumento3 páginasChapter IXCleo IlaoAinda não há avaliações

- Tarea Taller 1 FINA 503Documento4 páginasTarea Taller 1 FINA 503Hugo LombardiAinda não há avaliações

- Chap 2Documento16 páginasChap 2RABBIAinda não há avaliações

- Basic Q&A Balance SheetDocumento6 páginasBasic Q&A Balance SheetKunal Khaparkar patilAinda não há avaliações

- Introduction To Financial Statements - Views On News From EquitymasterDocumento4 páginasIntroduction To Financial Statements - Views On News From EquitymasterPrakash JoshiAinda não há avaliações

- Eng 111 S20 HW2Documento6 páginasEng 111 S20 HW2Edward LuAinda não há avaliações

- Cheap Sellers FSDocumento8 páginasCheap Sellers FSStan AccountAinda não há avaliações

- 2A FS Analysis Exercises 2022Documento5 páginas2A FS Analysis Exercises 2022Alyssa Tolcidas0% (1)

- 6.2 Money Accounts Versus Profitability AccountsDocumento9 páginas6.2 Money Accounts Versus Profitability AccountsArchitecture ArtAinda não há avaliações

- Handout 7 - Business FinanceDocumento3 páginasHandout 7 - Business FinanceCeage SJAinda não há avaliações

- Total Current Assets 1,345,000: Legal Ownership Is A Necessary Criterion When Determining The Existence of An AssetDocumento7 páginasTotal Current Assets 1,345,000: Legal Ownership Is A Necessary Criterion When Determining The Existence of An Assetann abegail perezAinda não há avaliações

- Project Report HP MananDocumento18 páginasProject Report HP Manankandarp patelAinda não há avaliações

- Bank ValuationDocumento34 páginasBank ValuationwathanaAinda não há avaliações

- ACCA AFM S22 NotesDocumento66 páginasACCA AFM S22 NotesdakshinAinda não há avaliações

- DeVry University Walmart ProjectDocumento12 páginasDeVry University Walmart ProjectKristin ParkerAinda não há avaliações

- Case 21Documento14 páginasCase 21Gabriela LueiroAinda não há avaliações

- Chapter 6 (CF)Documento51 páginasChapter 6 (CF)Hossain BelalAinda não há avaliações

- Unit 2 (I)Documento44 páginasUnit 2 (I)martaAinda não há avaliações

- Cash Flow - InvestopediaDocumento4 páginasCash Flow - InvestopediaBob KaneAinda não há avaliações

- Financial Accounting & AnalysisDocumento16 páginasFinancial Accounting & AnalysisMohit ChaudharyAinda não há avaliações

- Financial Statements ExercicesDocumento7 páginasFinancial Statements Exercicesluliga.loulouAinda não há avaliações

- Addtional Cash Flow Problems and SolutionsDocumento7 páginasAddtional Cash Flow Problems and SolutionsHossein ParvardehAinda não há avaliações

- End Beginning of Year of Year: Liquidity of Short-Term Assets Related Debt-Paying AbilityDocumento4 páginasEnd Beginning of Year of Year: Liquidity of Short-Term Assets Related Debt-Paying Abilityawaischeema100% (1)

- Ratio Analysis: Categories of RatiosDocumento7 páginasRatio Analysis: Categories of RatiosAhmad vlogsAinda não há avaliações

- Understanding Cash Flow Analysis: Ag Decision MakerDocumento4 páginasUnderstanding Cash Flow Analysis: Ag Decision MakerSURAJIT DAS BAURIAinda não há avaliações

- Poll 3 - SolutionDocumento19 páginasPoll 3 - Solutionakshita bansalAinda não há avaliações

- LXL Gr12Accounting 08 Revision Interpretation-of-Financial-Statements 27mar2014 PDFDocumento5 páginasLXL Gr12Accounting 08 Revision Interpretation-of-Financial-Statements 27mar2014 PDFNezer Byl P. VergaraAinda não há avaliações

- Cash Flow - HandoutDocumento3 páginasCash Flow - HandoutMichelle ManuelAinda não há avaliações

- Toaz - Info Preparation of Financial Statements and Its Importance PRDocumento7 páginasToaz - Info Preparation of Financial Statements and Its Importance PRCriscel SantiagoAinda não há avaliações

- Financial Stament ReviewDocumento8 páginasFinancial Stament Reviewロザリーロザレス ロザリー・マキルAinda não há avaliações

- HO No. 1 - Financial Statements AnalysisDocumento3 páginasHO No. 1 - Financial Statements AnalysisJOHANNAAinda não há avaliações

- Exercises: Method. Under This Form Expenses Are Aggregated According To Their Nature and NotDocumento15 páginasExercises: Method. Under This Form Expenses Are Aggregated According To Their Nature and NotCherry Doong CuantiosoAinda não há avaliações

- RWJBarnabas 2018 FinancialsDocumento52 páginasRWJBarnabas 2018 FinancialsJonathan LaMantiaAinda não há avaliações

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryAinda não há avaliações

- Summary of Richard A. Lambert's Financial Literacy for ManagersNo EverandSummary of Richard A. Lambert's Financial Literacy for ManagersAinda não há avaliações

- Securities Brokerage Revenues World Summary: Market Values & Financials by CountryNo EverandSecurities Brokerage Revenues World Summary: Market Values & Financials by CountryAinda não há avaliações

- Internship (1) FinalDocumento12 páginasInternship (1) FinalManak Jain50% (2)

- Paper:Introduction To Economics and Finance: Functions of Economic SystemDocumento10 páginasPaper:Introduction To Economics and Finance: Functions of Economic SystemQadirAinda não há avaliações

- Flange CheckDocumento6 páginasFlange CheckMohd. Fadhil JamirinAinda não há avaliações

- DSS 2 (7th&8th) May2018Documento2 páginasDSS 2 (7th&8th) May2018Piara SinghAinda não há avaliações

- Define Variable and ConstantDocumento17 páginasDefine Variable and ConstantSenthil MuruganAinda não há avaliações

- Damage To Bottom Ash Handling SysDocumento6 páginasDamage To Bottom Ash Handling SyssanjeevchhabraAinda não há avaliações

- Tourism and GastronomyDocumento245 páginasTourism and GastronomySakurel ZenzeiAinda não há avaliações

- Diagnostic Test Everybody Up 5, 2020Documento2 páginasDiagnostic Test Everybody Up 5, 2020George Paz0% (1)

- Electronic Waste Management in Sri Lanka Performance and Environmental Aiudit Report 1 EDocumento41 páginasElectronic Waste Management in Sri Lanka Performance and Environmental Aiudit Report 1 ESupun KahawaththaAinda não há avaliações

- Lab Activity 5Documento5 páginasLab Activity 5Jasmin CeciliaAinda não há avaliações

- The Evolution of Knowledge Management Systems Needs To Be ManagedDocumento14 páginasThe Evolution of Knowledge Management Systems Needs To Be ManagedhenaediAinda não há avaliações

- Higher Vapor Pressure Lower Vapor PressureDocumento10 páginasHigher Vapor Pressure Lower Vapor PressureCatalina PerryAinda não há avaliações

- Deictics and Stylistic Function in J.P. Clark-Bekederemo's PoetryDocumento11 páginasDeictics and Stylistic Function in J.P. Clark-Bekederemo's Poetryym_hAinda não há avaliações

- Exam Ref 70 483 Programming in C by Wouter de Kort PDFDocumento2 páginasExam Ref 70 483 Programming in C by Wouter de Kort PDFPhilAinda não há avaliações

- Jurnal KORELASI ANTARA STATUS GIZI IBU MENYUSUI DENGAN KECUKUPAN ASIDocumento9 páginasJurnal KORELASI ANTARA STATUS GIZI IBU MENYUSUI DENGAN KECUKUPAN ASIMarsaidAinda não há avaliações

- Catalog de Aparatura Si Instrumentar Veterinar Eikemeyer-GermaniaDocumento336 páginasCatalog de Aparatura Si Instrumentar Veterinar Eikemeyer-GermaniaDr. Dragos CobzariuAinda não há avaliações

- Annotated Bibliography 2Documento3 páginasAnnotated Bibliography 2api-458997989Ainda não há avaliações

- Student Committee Sma Al Abidin Bilingual Boarding School: I. BackgroundDocumento5 páginasStudent Committee Sma Al Abidin Bilingual Boarding School: I. BackgroundAzizah Bilqis ArroyanAinda não há avaliações

- NHD Process PaperDocumento2 páginasNHD Process Paperapi-122116050Ainda não há avaliações

- EQUIP9-Operations-Use Case ChallengeDocumento6 páginasEQUIP9-Operations-Use Case ChallengeTushar ChaudhariAinda não há avaliações

- 3-CHAPTER-1 - Edited v1Documento32 páginas3-CHAPTER-1 - Edited v1Michael Jaye RiblezaAinda não há avaliações

- Đề Anh DHBB K10 (15-16) CBNDocumento17 páginasĐề Anh DHBB K10 (15-16) CBNThân Hoàng Minh0% (1)

- 42ld340h Commercial Mode Setup Guide PDFDocumento59 páginas42ld340h Commercial Mode Setup Guide PDFGanesh BabuAinda não há avaliações

- Brochure - Actiwhite PWLS 9860.02012013Documento12 páginasBrochure - Actiwhite PWLS 9860.02012013J C Torres FormalabAinda não há avaliações

- Aryan Civilization and Invasion TheoryDocumento60 páginasAryan Civilization and Invasion TheorySaleh Mohammad Tarif 1912343630Ainda não há avaliações

- Isaiah Chapter 6Documento32 páginasIsaiah Chapter 6pastorbbAinda não há avaliações

- Market Structure and TrendDocumento10 páginasMarket Structure and TrendbillAinda não há avaliações

- Chapter 3.seed CertificationDocumento9 páginasChapter 3.seed Certificationalemneh bayehAinda não há avaliações

- July 2014Documento56 páginasJuly 2014Gas, Oil & Mining Contractor MagazineAinda não há avaliações

- The Story of An Hour QuestionpoolDocumento5 páginasThe Story of An Hour QuestionpoolAKM pro player 2019Ainda não há avaliações